You’re probably looking at life insurance because something in life just got more real. Maybe a baby arrived. Maybe you bought a home. Maybe you got married, changed jobs, or started a business and realized other people now depend on your income.

Then you hit the usual friction. Medical exam scheduling. Phone tag. Needles. Waiting. More waiting.

That’s exactly why no exam life insurance quotes have become so popular. The process feels much closer to applying for a modern financial product online than going through an old-school insurance ritual. And that matters because 50% of people said they’d be more likely to buy life insurance if it didn’t require a medical exam, according to The Zebra’s life insurance statistics roundup.

A lot of people don’t avoid life insurance because they don’t care. They avoid it because the process feels inconvenient, confusing, or intrusive. No-exam options are built to remove that barrier.

Table of Contents

- Skip the Needle Get Covered Sooner

- Understanding No Exam Life Insurance

- How No Exam Quotes Are Calculated Instantly

- What Drives Your No Exam Quote Price

- Get Your Accurate Online Quote Step by Step

- Who Benefits Most from No Exam Policies

- Take the Next Step Toward Peace of Mind

- Common Questions About No Exam Life Insurance

Skip the Needle Get Covered Sooner

A common scene goes like this. You finally decide to get coverage after months of meaning to do it. You open a few tabs, compare policies, and then see the phrase “medical exam required.” Suddenly the to-do list gets longer. You need to pick a time, be available at home or in an office, answer more questions, and wait for someone else’s schedule to line up with yours.

For a new parent running on little sleep or a professional bouncing between meetings, that’s enough to stall the whole decision.

No-exam life insurance changes the rhythm. Instead of planning around a nurse visit, you answer health questions online and let the insurer review digital records. The result is often a faster path to a real quote and, for many applicants, a faster path to coverage.

Practical rule: If the exam is the part that keeps you from applying, a no-exam quote may be the difference between “I should do this” and “done.”

That doesn’t mean every no-exam policy works the same way, or that every applicant gets the same kind of offer. Some policies are built for speed and large coverage amounts. Others are designed for smaller amounts with simpler approval rules. Knowing the difference helps you avoid comparing products that only look similar on the surface.

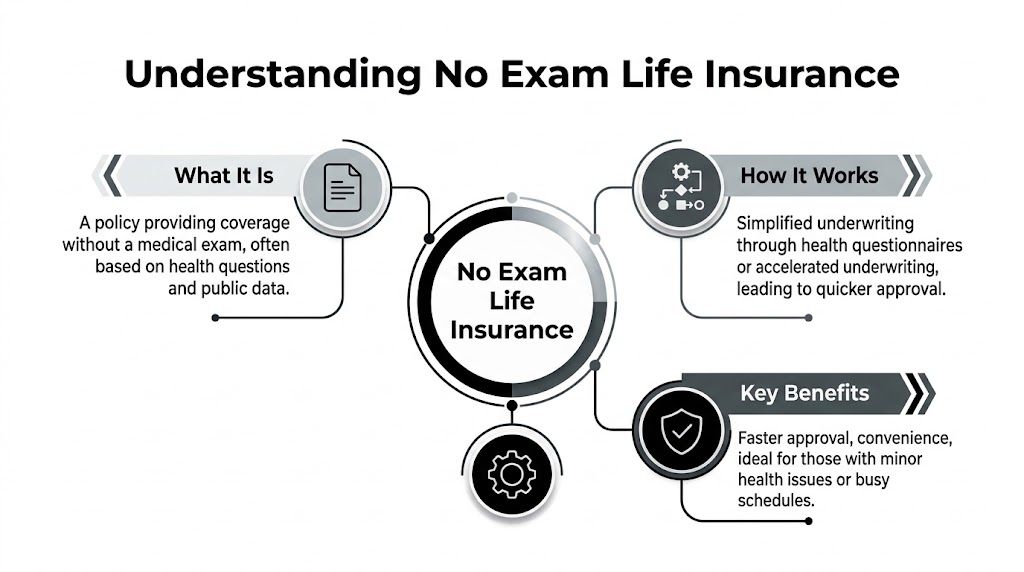

Understanding No Exam Life Insurance

No exam life insurance means you can apply for coverage without taking a physical medical exam. No blood draw. No urine sample. No nurse visit. Instead, the insurer relies on application answers and outside data to decide whether to offer coverage and at what price.

The easiest analogy is online mortgage pre-approval. You still provide information, and the lender still checks records. You’re not skipping evaluation. You’re skipping the slowest and most inconvenient part of the old process.

This category has grown far beyond a niche product. As Policygenius explains in its no-medical-exam life insurance guide, no-exam life insurance has evolved from niche simplified issue products to mainstream offerings, with providers like Pacific Life offering up to $3 million in coverage without an exam.

Three versions of no exam coverage

The phrase “no exam” can describe a few different paths. That’s where many shoppers get confused.

- Accelerated underwriting is the version often desired when seeking meaningful coverage quickly. It uses digital data and health questions to make a decision, often without a physical exam.

- Simplified issue usually asks more direct health questions and may offer lower coverage amounts than accelerated underwriting. If you want a closer look at that format, this overview of simplified issue life insurance is a helpful reference.

- Guaranteed issue is the broadest access option, but it generally comes with stricter limitations and is usually not what younger, healthy shoppers mean when they want affordable term coverage online.

Why this matters when you compare quotes

If one quote offers high term coverage and another offers a much smaller policy with more restrictions, those aren’t really apples-to-apples options. They may both be labeled “no exam,” but they serve different needs.

Some no-exam policies are designed for convenience. Others are designed for last-resort access. You want to know which one you’re looking at before you judge the price.

For many young families and working professionals, accelerated underwriting is the sweet spot. It keeps the convenience of skipping the exam while still making larger term policies available.

How No Exam Quotes Are Calculated Instantly

A parent applies for coverage after the kids go to bed, answers a few health questions, and sees a quote in minutes. That speed can feel suspicious. It helps to know what is happening behind the screen.

The insurer is still underwriting the application. It is just replacing part of the old process with a faster digital review instead of scheduling a nurse visit.

No exam does not mean no underwriting

In accelerated underwriting, software reviews the information you enter and compares it with outside records the insurer is allowed to check. According to Nationwide’s explanation of how no-exam life insurance works, insurers may use questionnaire responses, electronic medical records, prescription histories via the Medical Information Bureau, and driving records to assess risk, with approvals available for up to $3 million.

The goal is simple. The carrier wants to decide whether your risk fits its rules for the amount of coverage you requested.

Here are the records that often shape that decision:

- Application answers about your health, tobacco use, job, and personal history

- Electronic medical records when they are available

- Prescription history, which can point to current or past conditions

- MIB data, which helps insurers compare information across applications

- Driving records, because serious violations can signal higher risk

A traditional exam works like a manual review of a paper file. Accelerated underwriting works more like a secure digital screening that checks several trusted sources at once.

That is the part many shoppers never see. The quote may look instant, but the insurer is often checking for consistency in the background. If your application says one thing and a prescription record suggests another, the system may pause the process, adjust the offer, or ask for more review.

A small example makes the black box easier to understand. Say Applicant A takes medication for high blood pressure, but the condition has been stable for years and matches the medical record. Applicant B reports excellent health, but a recent driving record shows multiple serious speeding violations. An insurer's model may treat those two signals very differently. Well-managed treatment can look predictable. Recent risky driving can suggest a pattern the carrier prices more cautiously.

That is why accuracy matters so much. The fastest application is usually the most honest one.

It also explains why two companies can show different results for the same person. Each insurer builds its own model, chooses which signals matter more, and sets its own cutoff points for instant approval. One carrier may be comfortable with a certain prescription history if everything else looks clean. Another may send that same application to manual review.

So the process is not random, and it is not guesswork. It is a rules-based decision system that uses verified data to sort applicants into risk groups quickly. If you want to see how this option is commonly structured, this guide to no exam term life insurance gives a useful product overview.

What Drives Your No Exam Quote Price

Once the insurer has your information, it turns that risk picture into a premium. The price isn’t based on one answer. It comes from a bundle of factors working together.

For no-exam policies, convenience can come with a pricing tradeoff. As Ethos notes in its guide to no-exam term life insurance, healthy 35-year-olds may pay 15% to 30% more than they would for exam-based policies, though riders such as accelerated death benefits can add value.

The inputs behind the premium

Some factors are obvious. Age matters because insurance gets more expensive as risk rises with time. Tobacco use matters because it changes how the insurer sees long-term health risk. Coverage amount and term length matter because a larger or longer policy creates a bigger commitment for the carrier.

Other factors surprise people. Your family medical history can influence how an insurer views future risk. A dangerous hobby or a messy driving record can matter even if you feel healthy today. The insurer is pricing not just your current health, but the probability of paying a claim during the term.

If you want a focused look at this product category, this page on no exam term life insurance gives a useful product overview.

Key Factors That Influence Your No-Exam Quote

| Factor | Why It Matters | Example Impact |

|---|---|---|

| Age | Older applicants usually present more risk to the insurer | Two healthy people can see different prices mainly because one is older |

| Tobacco use | Smoking and nicotine use can raise perceived health risk | A non-smoker often gets a better quote than a smoker with otherwise similar answers |

| Current health | Conditions, medications, and symptoms affect eligibility and price | A person managing a condition may still qualify, but pricing may differ |

| Family history | Some insurers consider close family history of major illness | Strong family history can lead to more review |

| Driving record | Serious violations can suggest higher overall risk | Clean driving can help keep the file straightforward |

| Coverage amount | Higher death benefits create larger insurer exposure | A larger policy may trigger tighter underwriting |

| Term length | Longer terms keep the insurer on risk for more years | A longer policy often costs more than a shorter one |

| Riders | Optional features can increase value and sometimes cost | Adding living benefit features can change the final premium |

A useful mindset: Your quote is not a judgment. It’s a pricing decision based on the file the insurer can verify.

Get Your Accurate Online Quote Step by Step

A good online application feels simple, but a little prep makes it much smoother.

Before you start typing

Gather a few basics first. You’ll want your contact information, approximate income, the amount of coverage you think you need, any medications you take, and a clear picture of your medical history. You don’t need to overcomplicate it. You just want your answers to be consistent and complete.

A common mistake is rushing through health questions because they seem routine. Don’t do that. Even minor details can affect whether your quote stays the same after review.

A simple way to move through the application

Choose a quote platform that lets you compare clearly. A digital marketplace can help you see how offers differ without repeating the whole process each time. If you want to start that process, you can review instant online life insurance quotes.

Start with a realistic coverage goal. Think about who depends on your income, major debts, and how long your family would need support. You can adjust later, but starting with a sensible number gives the quote context.

Answer every health question directly. If you’ve taken medication, had a diagnosis, or seen a specialist, say so. Clear disclosure is what keeps an online quote from turning into a delayed application.

Review the term length carefully. Some people focus only on the monthly premium and forget that the policy has to last through the years that matter most. Match the term to the period when others depend on your income.

Compare final offers, not just the first number. Look at coverage amount, policy type, riders, and whether the insurer needs more review before approval.

This quick video gives a helpful sense of the online experience:

If a question feels unclear, pause and verify your answer. A five-minute delay now is better than a bigger delay after underwriting flags a mismatch.

Who Benefits Most from No Exam Policies

Some insurance products make the most sense only in narrow situations. No-exam coverage isn’t one of them. It fits several life stages especially well because the speed solves a real problem.

Young families who need protection fast

A couple brings home a newborn and suddenly starts seeing their finances differently. Childcare, mortgage payments, daily living costs, and future plans all depend on steady income. They don’t want a long underwriting process. They want protection in place while life is already moving fast.

For that household, no exam life insurance quotes can be appealing because the process cuts friction. They can apply online, answer the health questions, and move toward coverage without coordinating a separate medical visit.

Newlyweds and business professionals

A newly married couple often combines debts, savings goals, and long-term plans at the same time. Convenience matters because both schedules are usually full, and the insurance decision often gets pushed behind everything else. According to SelectQuote’s discussion of no-exam term life insurance, recent AI-driven underwriting trends have made higher-coverage no-exam policies attractive for newly married couples and business professionals, though premiums for $1M+ policies can remain 18% to 35% higher than fully underwritten options.

That tradeoff is easy to understand in real life. A healthy person might save money by taking the exam, but may still choose no-exam coverage because speed and convenience matter more right now.

Business owners and professionals often face a different pressure. They may need coverage tied to a loan process, succession planning, or family financial protection while traveling frequently or managing packed calendars. In that situation, a digital application can be less disruptive than arranging an exam.

- Young parents often value speed because the need feels immediate.

- Newlyweds often value simplicity because they’re organizing multiple financial decisions at once.

- Business professionals often value flexibility because their schedules make traditional steps harder to complete.

Take the Next Step Toward Peace of Mind

Life insurance doesn’t need to feel like a medical project. For many applicants, it can be a digital decision made from a laptop in one sitting.

The key idea is simple. No exam doesn’t mean the insurer skips due diligence. It means the company uses modern underwriting tools instead of sending you through the old exam process. Once you understand that, no exam life insurance quotes feel much less mysterious and much easier to trust.

If you’ve been putting this off because you didn’t want the hassle, that’s a solvable problem. Getting a quote can be quick, straightforward, and far less invasive than many people assume.

A few honest answers today can put real financial protection in place much sooner than you expected.

Common Questions About No Exam Life Insurance

What if I have a pre-existing condition

You may still qualify. No-exam coverage is not limited to people with perfect health. The insurer will review your application answers and available records, then decide whether to offer coverage, request more information, or steer you toward a different type of policy.

Is no-exam life insurance always more expensive

Not always in a way that matters equally to every shopper. Some healthy applicants may find exam-based coverage cheaper, while others decide the faster process is worth the difference. The right comparison is not just price. It’s price, convenience, timing, and the likelihood that the policy fits your actual life.

Can I get whole life without an exam

Sometimes, yes. But the structure and pricing can differ a lot from term life. If your main goal is affordable income protection during working years, term coverage is often the starting point people compare first.

What happens right after I submit my application

Usually, the insurer reviews your disclosures and checks the external data sources available for underwriting. Then one of several things happens. You may receive an offer quickly, get follow-up questions, or be told that a traditional exam would be required for that specific application.

Can I trust an instant quote

You can treat it as meaningful, but not magical. The quote is only as good as the information provided and what the insurer can verify. Accurate answers give you the best chance of seeing a quote that holds up through review.

If you’re ready to turn this from a task on your list into something finished, Coveredly makes it easy to explore digital life insurance options built for real schedules. You can compare no-exam term life coverage online, move quickly, and see whether you qualify for up to $3 million in coverage without the old exam hassle.