You're probably here because life got more real recently.

Maybe you brought home a new baby. Maybe you signed mortgage papers and realized that one income, one illness, or one accident could change everything for the people who count on you. That's usually when term life insurance stops feeling like an abstract financial product and starts feeling like a practical tool.

For many households, term coverage is the first place to look because it can provide a large death benefit during the years when responsibilities are highest. For a healthy 40-year-old buying $500,000 of 20-year term life insurance, the average cost is about $26 per month, while a comparable whole life policy could cost around $3,200 per year for men and $2,849 per year for women, according to NerdWallet's life insurance comparison guide. That price gap is why term life often becomes the default option for young families, homeowners, and anyone who wants meaningful protection without paying for permanent cash-value features.

A good term life insurance comparison isn't just about finding the lowest quote. It's about matching the policy to your timeline, your health profile, your debts, and your future options. When you compare that way, the decision gets simpler.

Table of Contents

- Introduction Choosing Protection That Fits Your Life

- Decoding the Details What to Compare in a Policy

- The Underwriting Divide Traditional Exam vs Digital No-Exam

- Your Step-by-Step Guide to Comparing Quotes

- Comparing Policies for Your Specific Life Stage

- A Practical Comparison Checklist Before You Apply

- Common Term Life Insurance Comparison Questions

Introduction Choosing Protection That Fits Your Life

People often assume life insurance is hard because there are too many products, too many carriers, and too many unfamiliar terms. In practice, the first decision is usually narrower than it seems. You're trying to protect a specific period of life when other people depend on your income or when a major debt would strain the household if you weren't there.

That's where term life stands out. It's built for a defined window, often when kids are still at home, a mortgage is still large, or a business loan is still active. Instead of paying for lifelong features you may not need, you buy coverage for the years that matter most financially.

Here's the useful shift in mindset. Don't start with, “Which company has the cheapest quote?” Start with, “What exactly am I protecting, for how long, and what kind of application process fits my life right now?” That one change makes term life insurance comparison much more practical.

| Comparison factor | What you should ask | Why it matters |

|---|---|---|

| Term length | How long do I need protection? | It should line up with debts, child-raising years, or income replacement needs |

| Coverage amount | What would my family or business actually need? | A low premium isn't helpful if the payout is too small |

| Premium structure | Are premiums level for the full term? | Predictable payments make budgeting easier |

| Underwriting | Do I want a medical exam or a faster digital path? | Approval speed and convenience can matter as much as price |

| Convertibility | Can I switch to permanent coverage later? | Flexibility matters if your health or goals change |

| Riders | Which add-ons are useful, and which are noise? | Some riders add real value, others just complicate the policy |

| Carrier strength | Is the insurer financially stable? | A policy is only as reliable as the company backing it |

Practical rule: The best policy usually isn't the one with the absolute lowest sticker price. It's the one that fits your life stage with the least mismatch.

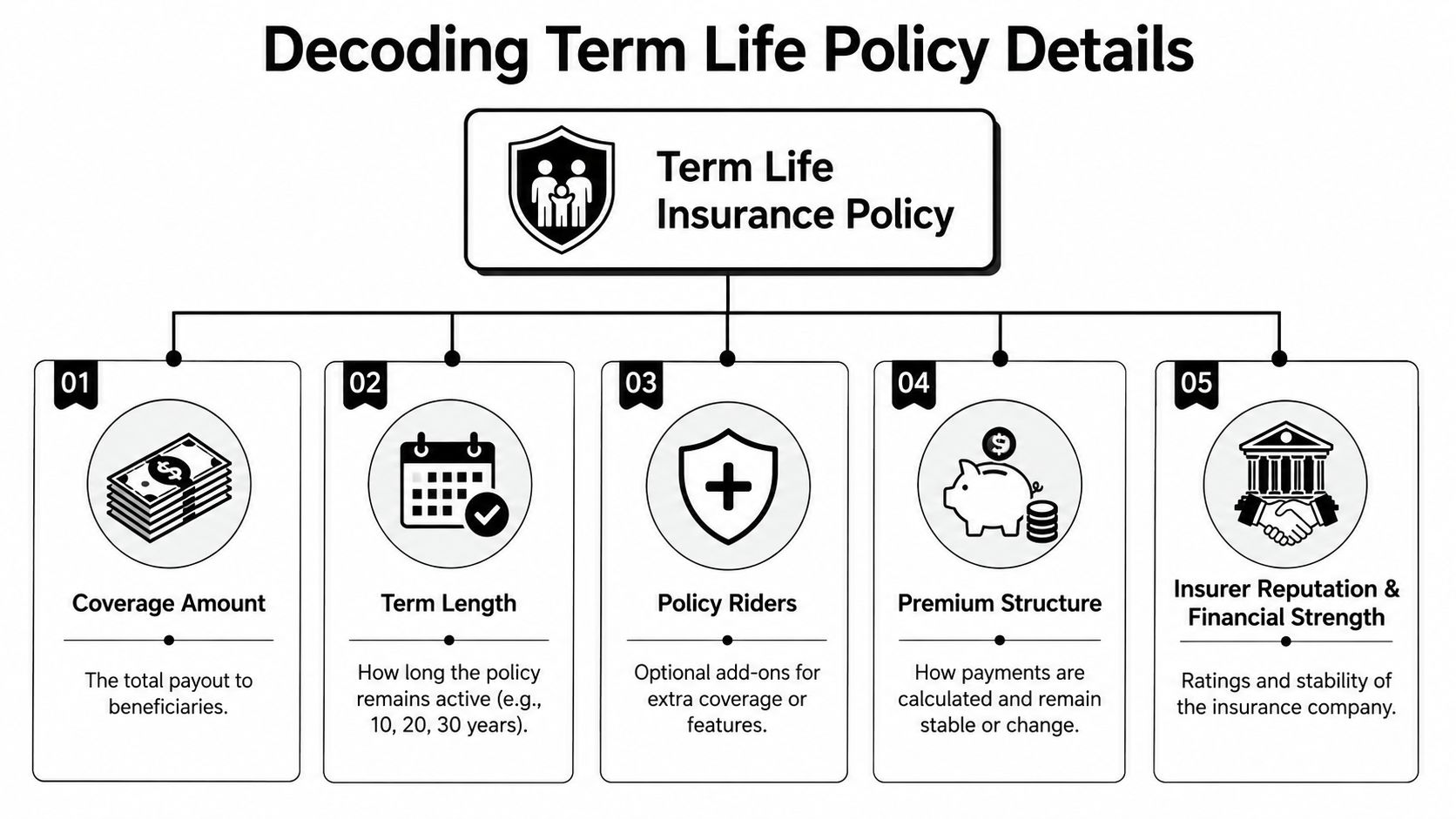

Decoding the Details What to Compare in a Policy

A term policy looks simple on the surface. You pay premiums, the insurer provides a death benefit, and coverage lasts for a set period. But the details inside that structure determine whether a policy is a good fit or a frustrating compromise.

Start with the term itself

The most basic comparison point is term length. If you only need protection until your kids are financially independent or until your mortgage balance is manageable, you want a term that covers that window. Buy too short a term and you may need replacement coverage later when you're older. Buy too long a term and you may pay more than necessary for years you don't really need.

Published market comparisons show that longer terms cost more because the insurer locks in your rate for a longer period. For a healthy 40-year-old buying a $500,000 policy, average annual costs are about $203 for a 10-year term, $331 for a 20-year term, and $579 for a 30-year term, according to Aflac's term policy comparison guide. That's a clean example of the trade-off. More years of guaranteed coverage generally means a higher premium.

Coverage amount matters just as much. Some buyers anchor too hard on income replacement and forget other obligations. Others focus only on debt and miss the need for ongoing family support. A stronger comparison looks at the whole picture:

- Income needs: How long would your household need support?

- Debt payoff: Mortgage, personal loans, or business debt.

- Future expenses: Childcare, education, or a surviving spouse's transition costs.

- Existing assets: Savings and employer benefits can reduce the gap.

Look past price alone

Two policies with similar prices can still be very different.

Convertibility is a good example. It means keeping a future door open. If your needs change later, a convertible term policy may let you move into permanent coverage without starting from scratch. That can matter if your health changes and buying a new policy becomes harder.

Riders deserve a closer look too. They're optional features, not automatic upgrades. Some can be useful. A waiver of premium rider may help if you become disabled and can't work. Other riders might sound appealing but add cost without solving a real problem in your life.

Then there's the insurer itself. A low quote from a carrier you haven't researched isn't automatically a bargain. You want a company with a solid reputation, clear policy language, and dependable service when beneficiaries need to file a claim.

Compare the policy design, not just the quote screen. A cheaper policy with weak flexibility can become the more expensive choice later.

A strong term life insurance comparison usually comes down to five questions:

- Does the term line up with my actual obligations?

- Is the death benefit sized for real needs, not guesses?

- Are premiums level and predictable for the full period I care about?

- Do the riders solve a real problem for me?

- Would I be glad this policy includes conversion if my health changes?

Those questions cut through a lot of marketing fast.

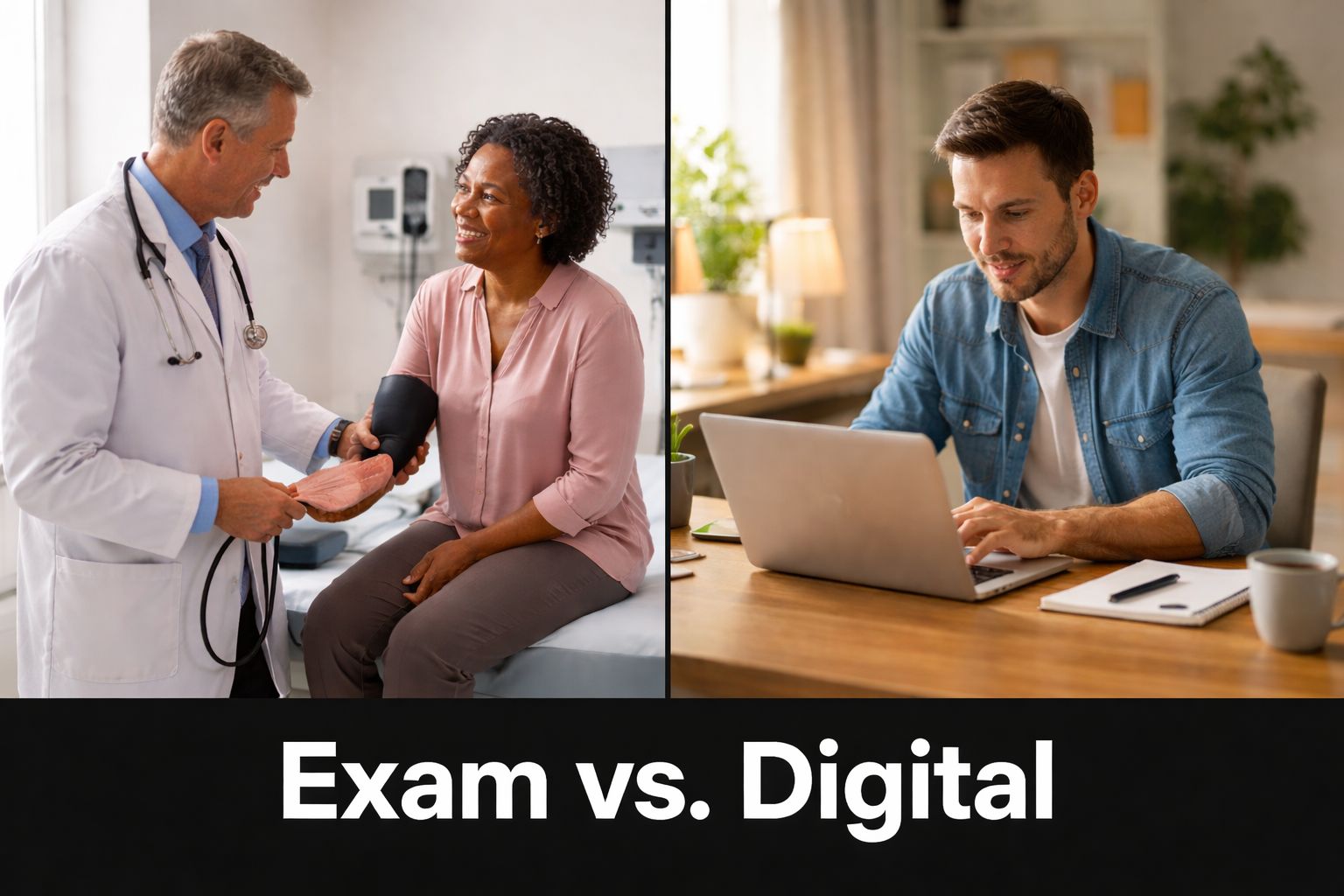

The Underwriting Divide Traditional Exam vs Digital No-Exam

For many buyers, the biggest surprise in a term life insurance comparison isn't price. It's how different the application experience can feel from one insurer to another.

Some policies follow a traditional underwriting route. That can include a medical exam, health questions, and a longer review process. Other policies use accelerated or no-exam workflows that rely on digital applications and other records-based review methods. Neither path is automatically better. The right choice depends on your timeline, your health history, and how much certainty you want before making a decision.

When traditional underwriting makes sense

Traditional underwriting can be a strong option if your situation is more complex. If you're applying for a larger amount of coverage, have a health history that needs context, or want the insurer to assess you with the fullest possible picture, the exam route may be appropriate.

Some applicants also prefer this route because it can feel more complete. They'd rather provide everything upfront than wonder whether a faster process will approve the amount they want.

When no-exam underwriting can be the better fit

No-exam term life is often appealing when timing matters. If you've just had a child, are closing on a home, or want protection in place before a key life event, speed becomes part of the value calculation.

The Financial Planning Association notes that expert comparisons should account for underwriting friction, and that the best policy balances underwriting speed and coverage certainty. It also notes that a no-exam process can be strategically valuable for digitally native buyers who need coverage quickly for a major life event, as discussed in the Financial Planning Association's underwriting comparison discussion.

If you want a clearer sense of how the process works, this guide to life insurance underwriting is a useful reference.

Here's a practical way to compare the two paths:

| Underwriting style | Best for | Trade-off to consider |

|---|---|---|

| Traditional exam | Complex health situations, larger coverage needs, buyers who want full review | More time and more steps |

| Digital no-exam | Time-sensitive buyers, straightforward applications, comfort with online process | May depend more heavily on available records and insurer rules |

Fast isn't automatically better, and slower isn't automatically more thorough for your needs. The better choice is the one that gets the right coverage in force with a process you're comfortable completing.

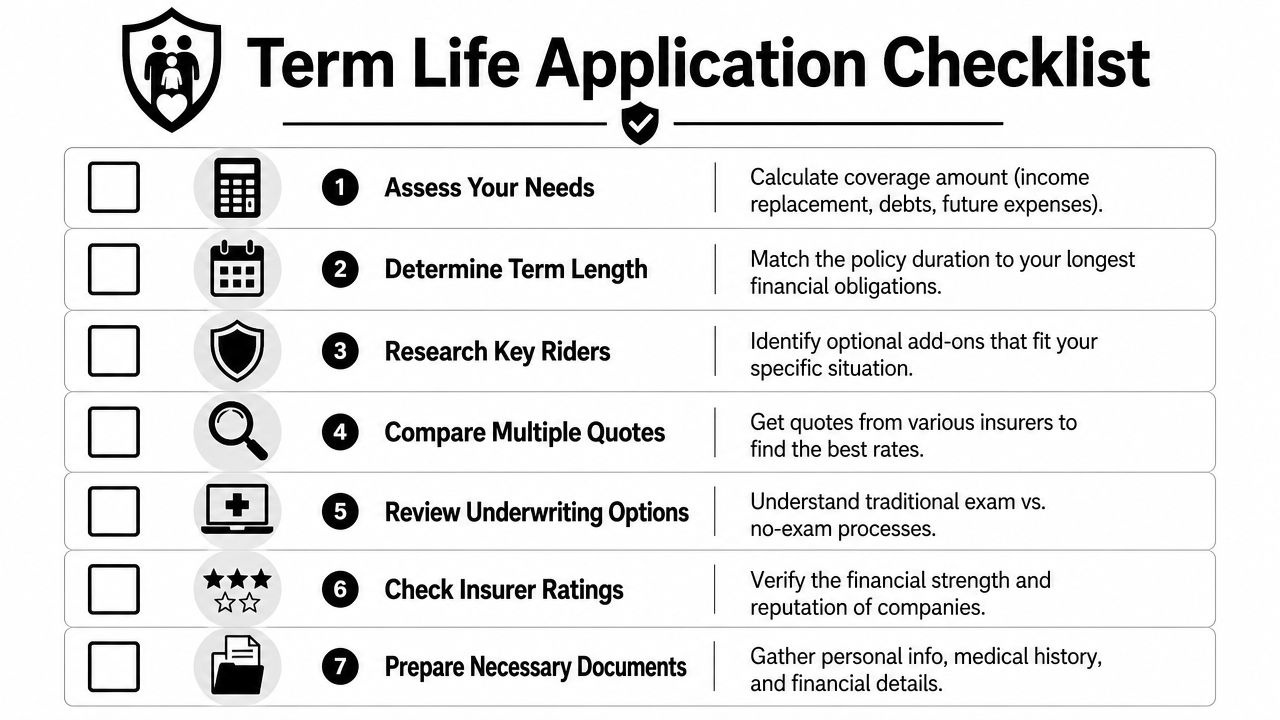

Your Step-by-Step Guide to Comparing Quotes

Once you know what matters in a policy, quote shopping gets much easier. The goal is to compare like with like, not to collect a pile of prices that mean different things.

Get your inputs right first

Start with the information that shapes your quote. Be consistent across every application or quote tool you use.

- Health details: Answer health and prescription questions carefully. Small inconsistencies can create confusion later.

- Coverage target: Pick a death benefit based on your actual needs, not just what sounds affordable.

- Timeline: Decide whether you're covering a mortgage, child-raising years, or a temporary business obligation.

- Budget range: Know what monthly or annual payment feels sustainable.

If you want to begin with a fast online estimate, you can review instant online life insurance quotes before narrowing down policy design details.

Compare policies, not just premiums

Once quotes come in, line them up side by side. Don't stop at the premium. Two similar prices can hide meaningful differences in policy quality.

Use this short review sequence:

- Match term lengths first. A lower quote may reflect a shorter term.

- Verify the death benefit. Make sure the coverage amount is identical across quotes.

- Check whether premiums are level. Budgeting is easier when the payment doesn't surprise you later.

- Review convertibility. If one policy lets you convert later and another doesn't, that matters.

- Inspect riders carefully. Keep the ones that address a genuine risk in your life.

- Look at underwriting requirements. A slower process may still be worth it, or it may not.

A useful way to keep yourself honest is to create your own comparison worksheet.

| Quote item | Policy A | Policy B | What matters most |

|---|---|---|---|

| Coverage amount | Must match | ||

| Term length | Must match | ||

| Premium | Compare after matching terms | ||

| Exam required | Affects convenience and speed | ||

| Convertible | Adds future flexibility | ||

| Key riders | Judge usefulness, not quantity | ||

| Carrier confidence | Look for stability and clarity |

A smart quote comparison feels a little boring. That's good. Boring usually means you're comparing apples to apples instead of reacting to the first low number you see.

Comparing Policies for Your Specific Life Stage

The right term policy often becomes obvious when you look at the life stage behind the purchase. The same product category can serve very different goals.

A quick visual can help frame the differences.

Young family

A couple with small children usually needs the broadest protection. The main concern isn't just paying off a debt. It's replacing income, preserving housing stability, and giving the surviving parent breathing room.

That usually makes level term the cleaner fit because the death benefit stays fixed for the full term. A shrinking payout can create a mismatch if the family still needs a stable pool of funds for childcare, education planning, and everyday living.

Parents who are thinking through this stage in more detail may also find this resource on life insurance for new parents helpful.

Newlyweds

Newly married couples often sit in a middle ground. They may share rent or a mortgage, combine debts, and start planning for children, but their obligations may still be building.

For this group, comparison tends to focus on flexibility. A term policy with a sensible premium, the option to convert later, and straightforward riders can make more sense than over-insuring too early. The point isn't to buy the biggest policy possible. It's to protect the financial life you've started to build together.

This video gives a useful overview for buyers thinking through those trade-offs.

Business professional or debt-focused buyer

The comparison process gains nuance in specific situations. If your main goal is to cover a specific declining debt, such as a mortgage or business loan, decreasing term may deserve a close look.

Prudential explains that a decreasing term policy has a death benefit that declines over time while premiums stay level, which can make it a cost-effective option for a specific declining debt like a mortgage. It's generally less suitable for families that need a fixed payout for long-term income replacement, as outlined in Prudential's explanation of level versus decreasing term life insurance.

That distinction matters. A buyer securing a loan may reasonably care more about balance-sheet protection than income replacement. A parent supporting children usually needs the opposite.

Here's the practical shortcut:

- Choose level term if your survivors would need a steady, unchanged payout.

- Consider decreasing term if you're mainly covering a debt that should shrink over time.

- Prioritize convertibility if your income is rising and future needs may become more permanent.

- Pay attention to underwriting speed if a closing date, financing requirement, or family milestone is approaching.

Your life stage should drive the comparison. Not the ad you saw first.

A Practical Comparison Checklist Before You Apply

Buying term life gets easier when you reduce the decision to a few concrete checks. Save this list and use it before you submit an application.

Use this before you hit submit

- Confirm your coverage need: Include income replacement, debts, and future expenses that would still exist if you weren't there.

- Match the term to your timeline: Think in obligations, not generic policy lengths.

- Decide how much underwriting friction you can tolerate: If speed matters, make that part of your comparison.

- Review convertibility: Future flexibility can be worth more than a tiny difference in premium.

- Scrutinize riders: Keep useful add-ons. Skip decorative ones.

- Check the carrier's reputation: You want a company your beneficiaries won't struggle with later.

- Read the policy summary carefully: Make sure the quote and the issued policy line up.

- Prepare your documents and health history: Cleaner applications usually move more smoothly.

- Review beneficiaries before signing: This step is easy to rush and annoying to fix later.

A good checklist does something simple. It keeps you from making a rushed decision based only on a headline price.

The application should feel clear by the time you start it. If you're still confused about the policy design, pause and compare again before applying.

Common Term Life Insurance Comparison Questions

Even after you've narrowed choices, a few practical questions tend to stick around. These are the ones buyers ask most often.

What happens if I outlive my term policy

In most cases, coverage ends when the term ends. If you still need protection at that point, you may need to renew, convert if the policy allows it, or buy a new policy. The key issue isn't that term ends. It's whether the original term length matched the financial risk you were trying to cover.

Can I have more than one life insurance policy

Yes, many people do. Someone might have one policy through work and another individual term policy. Others layer coverage for different needs, such as one policy tied to family income protection and another tied to a specific debt.

How do health and smoking affect comparisons

They can affect both pricing and which underwriting path is realistic. If your health history is straightforward, a digital or no-exam option may be more attractive. If your history is more involved, you may want a policy and carrier that handles full underwriting well. The most useful comparison is the one based on honest answers from the start.

What is the free look period

This is the review period after a policy is issued when you can examine the contract and decide whether to keep it. Rules vary by insurer and state, so check the specific policy documents. It's your chance to verify that the coverage, riders, and premium match what you expected.

One last question sits underneath all the others. How do you know when you've found the right policy? Usually, it's when the trade-offs are clear. You understand why this term length fits, why this underwriting route fits, and why these features matter for your actual life instead of an imaginary ideal buyer.

If you want a simpler way to shop online, Coveredly offers digital-first life insurance designed to fit real life. You can explore flexible term coverage, compare options with less friction, and move from quote to application in a way that feels clear instead of overwhelming.