You might be reading this because someone you love just died, and the mail is still coming. Credit card statements. A car loan notice. A mortgage bill. Maybe a hospital invoice. Or maybe you're planning ahead because you just bought a home, got married, or welcomed a baby, and the question hit you all at once: what happens to debt when you die?

That question sounds cold when you're grieving and unnerving when you're planning. But understanding it is one of the most practical things you can do for the people who depend on you. Debt after death isn't rare, and it isn't a sign that someone failed. It's part of modern family finances.

This guide walks through the legal basics, then goes further into what survivors need to do. You'll learn who pays, who doesn't, what creditors can ask for, and how to respond without panic.

Table of Contents

- Thinking About the Unthinkable

- The Fundamental Rule Your Estate Settles Your Debts

- When Debt Passes to Others Co-Signers and Spouses

- How Different Types of Debt Are Handled After Death

- The Executor's Role in Managing Estate Debts

- First Steps for Survivors A Practical Checklist

- Using Life Insurance to Protect Your Family's Future

Thinking About the Unthinkable

A lot of families first face this topic at a happy moment. A couple is reviewing mortgage paperwork. They're talking about nursery colors. One person asks, "If something happened to me, would you be stuck with all this debt?" That isn't pessimism. It's love in practical form.

The first reassuring truth is that this problem is common. A widely cited credit-reporting study reported that 73% of Americans who died in one period had outstanding debt after death, with an average of $61,554 left unpaid according to Debt.org's discussion of debt after death. The same discussion noted credit card balances, mortgages, and auto loans among the most common debts.

That matters because many people assume debt at death is unusual, or that only reckless borrowers leave bills behind. That's not how real life works. Most households carry ordinary obligations while building a life. A mortgage can mean stability. A car loan can mean getting to work. A credit card balance can mean surviving a rough season.

Practical rule: If your family has debt, you haven't done anything strange or irresponsible. You just need a plan for how it would be handled.

The rest of this article is meant to lower the temperature. You don't need to memorize probate law. You do need to understand the basic flow, the exceptions, and the first phone calls to make if you're the person left sorting through it all.

The Fundamental Rule Your Estate Settles Your Debts

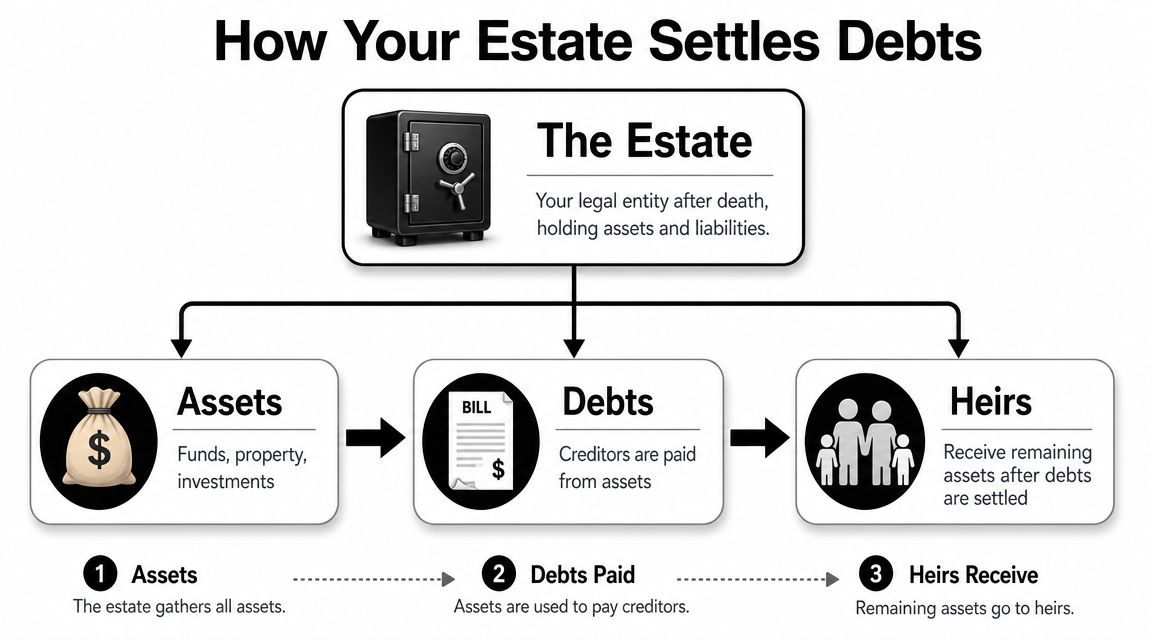

The core answer to what happens to debt when you die is simple. Your estate settles your debts. Your family usually doesn't have to pull out their own checkbook just because you died.

Think of an estate as a temporary financial container. When a person dies, that container holds what they owned and what they owed. Its job is to collect the money and property, deal with valid claims, and then pass along whatever remains.

Why the estate comes first

The Consumer Financial Protection Bureau says that when someone dies, their money and property first go toward repaying debts, and if the estate has no money, the debts usually go unpaid. The CFPB also notes that survivors may still be responsible in some cases, such as co-signing or certain spousal situations under state law, in its explanation of whether debt goes away when a person dies.

That one rule clears up a major fear. Your daughter doesn't inherit your Visa bill just because she's your daughter. Your brother doesn't owe your personal loan because he handled the funeral. Your spouse isn't automatically responsible for every debt in every state because you were married.

Creditors generally look first to the estate. If the estate has enough value, the estate pays legitimate debts. If it doesn't, some creditors may not be fully paid.

What counts as assets and debts

Assets are things the person owned. That can include bank accounts, a house, a car, investments, and personal property.

Debts are what the person owed. That can include credit cards, loans, medical bills, and other obligations.

A simple way to picture the process:

- Someone is appointed to handle the estate

- That person identifies assets and debts

- Valid debts are paid from estate property

- Heirs receive what is left, if anything is left

Heirs are not first in line. Creditors usually get paid before inheritances are distributed.

This is why families are sometimes surprised when a loved one "owned a home" but there still isn't much left to pass on. Ownership alone doesn't tell you what survives probate. Debt claims can reduce what heirs receive.

When Debt Passes to Others Co-Signers and Spouses

The general rule is comforting. The exceptions are where confusion starts. A survivor can become responsible when they were already legally tied to the debt before death, or when state law creates that responsibility.

Joint accounts and co-signed loans

A joint account holder isn't just someone allowed to use an account. They're usually a full owner of the debt. If two people took out a loan together, the surviving borrower is typically still responsible for the remaining balance.

A co-signer is also different from a supportive family member who merely knew about the loan. A co-signer signed the contract and agreed to repay the debt if the main borrower didn't. Death doesn't erase that promise.

Here are the practical differences people often miss:

- Joint borrower: You borrowed the money together. The surviving borrower generally remains liable.

- Co-signer: You backed the loan contract. The lender can still expect payment from you.

- Authorized user: You were allowed to use a credit card, but you usually weren't the owner of the account debt.

That last point matters because many survivors assume any name attached to a card means equal responsibility. That's not always true. Being an authorized user and being a joint account holder are not the same thing.

Spouses and community property rules

Spousal responsibility depends heavily on where you live and how the debt arose. The CFPB identifies community property states as Alaska (if a special agreement is signed), Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin in its guidance linked earlier.

In those states, a surviving spouse may have responsibility for certain debts incurred during the marriage, depending on state law. Outside those situations, "my spouse died, so now I owe all their debts" is often an oversimplification.

A few examples help:

- Example one: Your spouse had a credit card only in their name. In many cases, the estate is the first place that debt is handled.

- Example two: You co-signed your spouse's car loan. You're still on the hook because you signed the loan contract.

- Example three: You live in a community property state. The answer may depend on state rules and whether the debt was considered part of the marital community.

Don't agree to pay a debt just because a caller says you're the "next of kin." That phrase sounds official, but liability usually turns on the account contract and state law, not family title.

If you're unsure whether you're a joint borrower, co-signer, authorized user, or a spouse, pull the original account paperwork before making promises.

How Different Types of Debt Are Handled After Death

Not all debt behaves the same way. The key distinction is whether the debt is tied to property, tied to another borrower, or subject to a special discharge rule.

Secured debt works differently

Some debts are secured, which means the lender has rights in a specific asset. A mortgage is attached to a house. An auto loan is attached to a car. If payments stop and the estate can't resolve the debt, the lender can pursue the collateral through the estate process.

Other debts are unsecured, such as many credit cards and personal loans. Those creditors can make claims against the estate, but they don't usually have a specific house or car to take just because the debt exists.

The outcome also depends on product type. The legal summary at Carolina Family Estate Planning's article on debt after death notes that federal student loans are discharged at death, while secured debts allow lenders to pursue collateral and joint debts remain enforceable against a surviving co-owner.

If you're trying to sort property from probate property, this guide on whether life insurance is part of an estate can help clarify what may pass outside the estate and what may still be exposed to estate administration.

Debt after death quick reference

| Debt Type | What Happens to the Debt? | Key Survivor Considerations |

|---|---|---|

| Mortgage | The lender can pursue the house through the estate because the loan is secured by the property. | If someone wants to keep the home, they need to address ongoing payments and communicate with the servicer. |

| Auto loan | The lender may pursue the vehicle if the loan isn't paid because the debt is secured by the car. | Decide quickly whether keeping the car makes sense for the estate or surviving family. |

| Credit card debt | Usually handled as a claim against the estate if it was in the deceased person's name alone. | Check whether another person was a joint account holder or only an authorized user. |

| Personal loan | Typically a claim against the estate unless another person also signed for it. | Pull the loan agreement before assuming anyone else owes it. |

| Federal student loans | Discharged upon death. | Survivors should still notify the loan servicer and provide the required documentation. |

| Private student loans | Depends on contract terms and whether someone else is legally obligated. | Review the promissory note and any co-signer obligation. |

| Medical bills | Usually treated like other unsecured claims against the estate. | Don't pay from personal funds before confirming whether the estate is responsible. |

| Joint debt | Remains enforceable against the surviving co-owner. | The survivor may need to keep paying even while the estate is being administered. |

One of the biggest mistakes families make is treating all bills the same. They aren't. A mortgage statement, a hospital invoice, and a federal student loan notice may each require a different response.

The Executor's Role in Managing Estate Debts

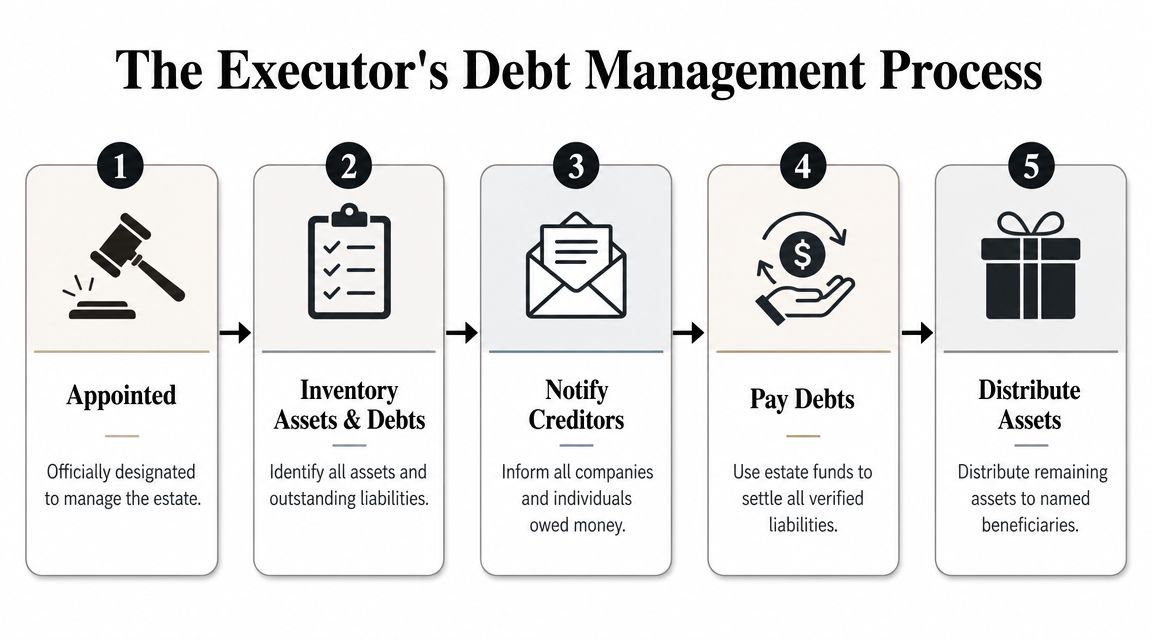

When people hear executor, they often picture a lawyer in a courtroom. In practice, the executor is the person responsible for handling the deceased person's financial wrap-up.

What the executor actually does

The executor's debt-related job usually includes tasks like these:

- Gather records: Find account statements, loan documents, insurance paperwork, tax records, and the will.

- Identify assets: List bank accounts, property, vehicles, investments, and personal property.

- Identify creditors: Make a working list of companies and people the deceased may have owed.

- Review claims: Confirm which bills are legitimate and which may need more documentation.

- Pay valid debts from estate funds: Use estate assets, not personal money, unless the executor separately owes a debt.

- Distribute what's left: Only after debts and administration obligations are handled.

This role is administrative, but it's also protective. A careful executor creates a buffer between grieving relatives and a flood of demands.

Later in the process, this video gives a useful visual overview of how estate administration works in practice.

Why probate feels slow

Families often worry that "nothing is happening" in the first weeks. Usually, a lot is happening. The executor may be waiting on certified death certificates, court appointment paperwork, account access, and responses from creditors.

Probate can feel mechanical during an emotional time, but the sequence exists for a reason. It helps make sure debts are addressed in an orderly way before property is handed out too early.

The executor's job isn't to pay bills fast. It's to pay the right bills, from the right source, in the right order.

That distinction protects the estate and the family. It also prevents a common problem where relatives rush to pay a creditor out of pocket, only to discover later they weren't legally responsible.

First Steps for Survivors A Practical Checklist

The first days after a death are disorienting. During this period, people need a checklist, not a lecture.

What to do in the first days

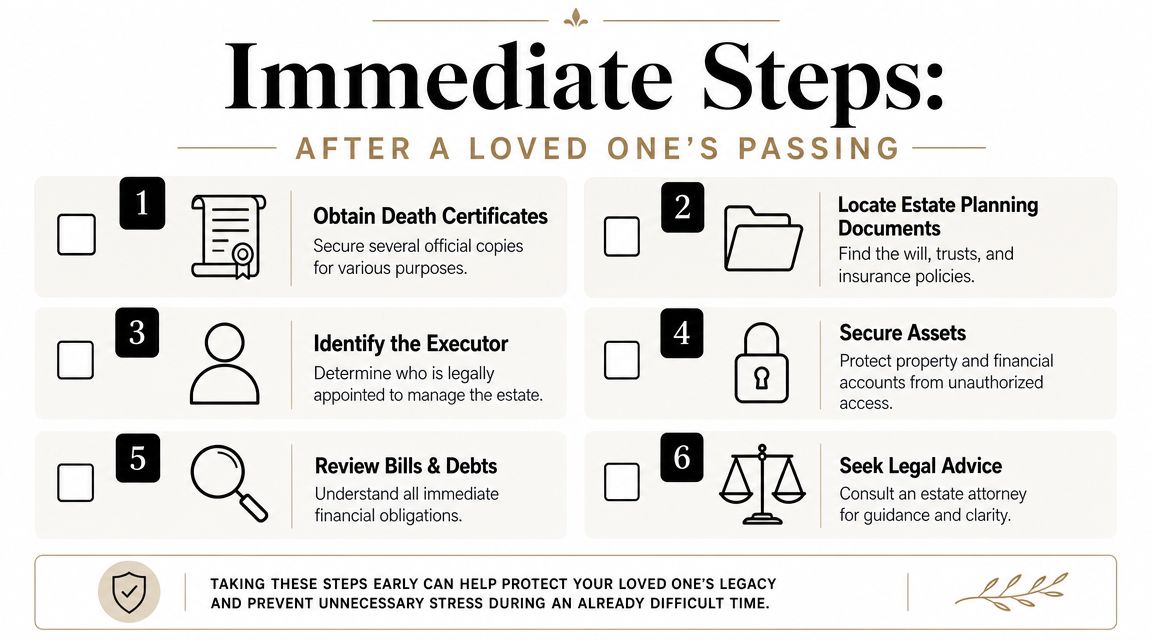

Start with the basics that open up almost everything else:

- Get several certified death certificates. Banks, insurers, loan servicers, and courts often ask for one.

- Find the will and estate documents. Also look for trusts, insurance policies, and account lists.

- Identify the executor or likely estate representative. Creditors will want to know who is authorized to speak.

- Secure property and accounts. Protect mail, vehicles, home access, and important devices or files.

- Make a debt list. Gather statements for the mortgage, credit cards, auto loans, medical bills, and student loans.

- Pause before paying. Don't start sending personal money just because a bill arrived.

If a life insurance policy exists, this step-by-step guide on how to file a life insurance claim can help survivors gather the right documents and start the claim process.

How to talk to creditors and collectors

The Federal Trade Commission says debt collectors may only discuss a deceased person's debt with limited parties, such as an executor, spouse, parent of a minor, guardian, lawyer, or confirmed successor in interest, in its consumer guidance on debts and deceased relatives.

That means not every grieving relative has to take every phone call. It also means a collector doesn't get to pressure a sibling, adult child, or cousin into a payment plan just because they answered the phone.

Use language like this when you call:

- If you're the executor: "I am the executor for the estate. Please note your records and tell me what documentation you need."

- If you're not responsible: "I'm notifying you of the death. I'm not agreeing to pay this debt personally."

- If a collector keeps calling: "Please direct communications to the authorized estate representative."

A few practical cautions matter here:

- Don't promise payment too early: A promise can create confusion and pressure before the estate is reviewed.

- Don't use the deceased person's cards or accounts: Even small charges after death can complicate matters.

- Don't distribute assets casually: Wait until debts and estate procedures are clear.

- Keep a communication log: Write down who called, the company name, the account involved, and what they requested.

If you're not legally responsible, you can say so clearly and calmly. Grief doesn't require you to become a collector's customer service desk.

The process is still emotional, but it becomes more manageable once one person is designated to handle communication and paperwork.

Using Life Insurance to Protect Your Family's Future

Debt after death creates one big practical problem. Survivors often need cash quickly, while estate administration takes time. Mortgage payments, rent, child care, groceries, and funeral costs don't wait politely for probate to finish.

That's where life insurance can change the experience for a family. In many situations, the benefit is paid directly to the named beneficiary rather than being tied up in the estate process. That gives survivors flexibility. They can use the money to keep making mortgage payments, pay off a car loan, cover daily living costs, or buy time to make careful decisions instead of rushed ones.

This is why life insurance isn't only about replacing income. It's also about protecting the rest of the family's financial life from being squeezed at the worst possible moment. When there is liquid money available outside the slow pace of estate settlement, families often have more choices and less panic.

If you're trying to estimate a practical coverage amount, this guide on how much life insurance you need is a helpful starting point.

Planning for what happens to debt when you die isn't morbid. It's one of the clearest ways to make sure your family has breathing room when they need it most.

If you're thinking about protecting your family with life insurance, Coveredly offers a simple online way to explore coverage that fits real life. It's built for busy families and professionals who want flexible term life insurance without a complicated process.