You're catching up on bills after a long week. One child is finally asleep, your inbox is full, and then you see it. A notice that an insurance premium was due.

That moment can trigger instant panic. Is your coverage gone? If something happens tonight, will the policy still work? Do you need to start over?

In many cases, the answer is less scary than it first feels because insurance policies often include a grace period. That's the built-in window after a due date when you may still be able to pay and keep coverage in place. If you've ever wondered what is a grace period in insurance, the short answer is this: it's a contractual buffer meant to protect you from losing coverage the second you miss one payment.

For families with life insurance, health insurance, or auto coverage, understanding that buffer matters. It can affect whether a claim is paid, whether a policy lapses, and whether getting coverage back becomes simple or stressful. If you want to get more comfortable with policy language in general, it helps to learn how to read a life insurance policy.

Table of Contents

- What Is a Grace Period and Why Does It Matter

- The Core Concept of an Insurance Grace Period

- How Grace Periods Differ for Life Health and Auto Insurance

- The Timeline What Happens During and After the Grace Period

- A Practical Action Plan for Handling Missed Payments

- Your Questions Answered About Insurance Grace Periods

What Is a Grace Period and Why Does It Matter

Your life insurance premium is due on Friday. The same week, your car needs new tires, your child gets sick, and the autopay card on file has expired. By Monday, one question starts to feel urgent. Are you still covered, or did one missed payment put the policy at risk?

A grace period is the short window after a premium due date when your insurance can remain in force while you catch up on a late payment. For life insurance, that window is often written into the policy and shaped by state rules. If you want to see where payment timing and lapse language usually appear, this guide on how to read a life insurance policy can help.

That matters because a missed due date and a policy lapse are not always the same event.

For families, the grace period is the insurance version of a buffer lane. You are past the due date, but not necessarily past the point of keeping coverage. That can make a big difference if the payment was missed because of a bank issue, a billing error, travel, or a tight month.

It also helps to know what a grace period does not do. It does not erase the bill, and it does not give you unlimited extra time. It gives you a brief chance to fix the problem before the policy moves into lapse or termination status.

The practical value shows up in three moments. Before a missed payment, it gives you room for ordinary life mistakes. During the grace period, it can affect whether a claim is reviewed, paid, or reduced by the premium still owed, depending on the policy and insurance type. After the grace period ends, getting coverage back may require more than just sending money. Reinstatement can involve forms, proof of insurability, or insurer approval.

That is why this term deserves more attention than it usually gets. The primary question is not only whether a grace period exists. The primary question is what happens to your coverage, your claim, and your next steps before, during, and after that missed payment.

The Core Concept of an Insurance Grace Period

The easiest way to think about a grace period is as a buffer zone between “payment due” and “policy lapse.” It doesn't erase the fact that payment is overdue. It gives you a limited window to fix it.

For life insurance, that buffer became more important as billing shifted away from in-person collection and toward recurring billing and automatic payments. Axis Max Life describes the modern grace period as a foundational feature of life insurance administration and a last safety net for people who miss a payment because of forgetfulness or administrative delays in its overview of how insurance grace periods work.

It's a contract feature, not a favor

This is the part many people miss. A grace period is usually part of the policy structure itself. That means the insurer isn't “being nice” if your coverage remains active for a short period after the due date. The policy and applicable law often allow that result.

That's why the term matters so much in life insurance. If your policy includes a grace period and you pay within it, coverage generally continues without interruption. If you don't, the policy may lapse.

A simple analogy that helps

Think of your policy like a bridge toll pass.

- Due date arrives: your account should be funded.

- Grace period begins: the gate doesn't drop instantly.

- You still need to pay: the system is giving you a short chance to correct the miss.

- If you ignore it: access can close, and reopening it may take more work.

That's why “what is a grace period in insurance” is really a question about risk management. The grace period lowers the chance that one missed premium instantly destroys long-term protection.

Coverage during a grace period is often still in force, but it sits in a time-sensitive default state. That's why speed matters more than reassurance.

What the grace period is designed to do

Its purpose is practical:

- Prevent sudden loss of protection: one missed payment doesn't necessarily end coverage on the spot.

- Give policyholders time to cure the default: you can make the overdue payment and often keep the policy intact.

- Reduce avoidable lapses: especially when the missed payment came from an oversight rather than a decision to cancel.

For young families, that design matters most with life insurance because the point of the policy is continuity. A short billing mistake shouldn't automatically cancel a major protection plan.

How Grace Periods Differ for Life Health and Auto Insurance

A missed payment can play out very differently depending on the policy in your hand.

If a parent misses a life insurance premium by a few days, the policy often gets a longer cushion. If that same family misses an auto payment, the timeline can be much tighter. With health insurance, the hardest part is that you may still be inside the grace period while claims are being treated differently behind the scenes.

That is why it helps to compare these policies side by side.

Typical Insurance Grace Periods by Policy Type

| Insurance Type | Typical Grace Period | What to watch for in real life |

|---|---|---|

| Life insurance | Often about 30 to 31 days | Coverage is usually still in force during that window, but the overdue premium still needs to be paid before the period ends. |

| Marketplace health insurance for eligible subsidized enrollees | 90 days | Claims treatment can change after the first month, which can surprise families who assume the full 90 days works the same way throughout. |

| Auto insurance | Varies by insurer and state | The window may be shorter, cancellation rules can be stricter, and waiting too long can create a gap in coverage. |

Life insurance usually gives the clearest runway

Life insurance often works most like a bill with a built-in late window. The due date passes, the grace period starts, and you still have time to catch up before the policy lapses.

State law can make that window longer. For example, the California Department of Insurance explains protections around life insurance lapse and grace periods, which is a good reminder that your policy contract is only part of the answer. Your state's rules matter too.

One practical detail families sometimes miss is what happens after a longer payment problem. If a policy does lapse, reinstatement may require more than sending the missed premium. Some policies may ask for a reinstatement application, proof the insured is still medically insurable, and payment of overdue amounts. If you are reviewing policy features that protect coverage during hardship, it also helps to understand how a waiver of premium rider works.

Health insurance has the most moving parts

Health insurance can be harder to read because the grace period is not always one continuous experience.

For people who receive advance premium tax credits through the Marketplace, HealthCare.gov explains the 90-day grace period and how claims may be handled during that time. The short version is simple. The first month is treated one way. Later months can bring more uncertainty for claims if the overdue premium is not caught up.

That creates a practical risk for families. You may still technically be in the grace period, but a doctor's visit or prescription claim may not move through the system in the same way it did before the missed payment.

Auto insurance calls for the fastest response

Auto insurance is the policy type where assumptions can hurt you fastest.

Some insurers give a short grace period. Some rely heavily on the cancellation notice and the exact date listed there. The Texas Department of Insurance explains that auto insurance cancellation rules depend on the policy and notice requirements, which shows why “I probably still have time” is a risky guess.

A useful way to view auto coverage is this. Life insurance often focuses on preserving long-term protection. Auto insurance often focuses on whether the policy is active on the day you drive, the day you renew registration, or the day an accident happens. A short lapse can create immediate problems.

With auto insurance, the safest move is to read the cancellation notice, check the exact end date, and call the insurer the same day if a payment was missed.

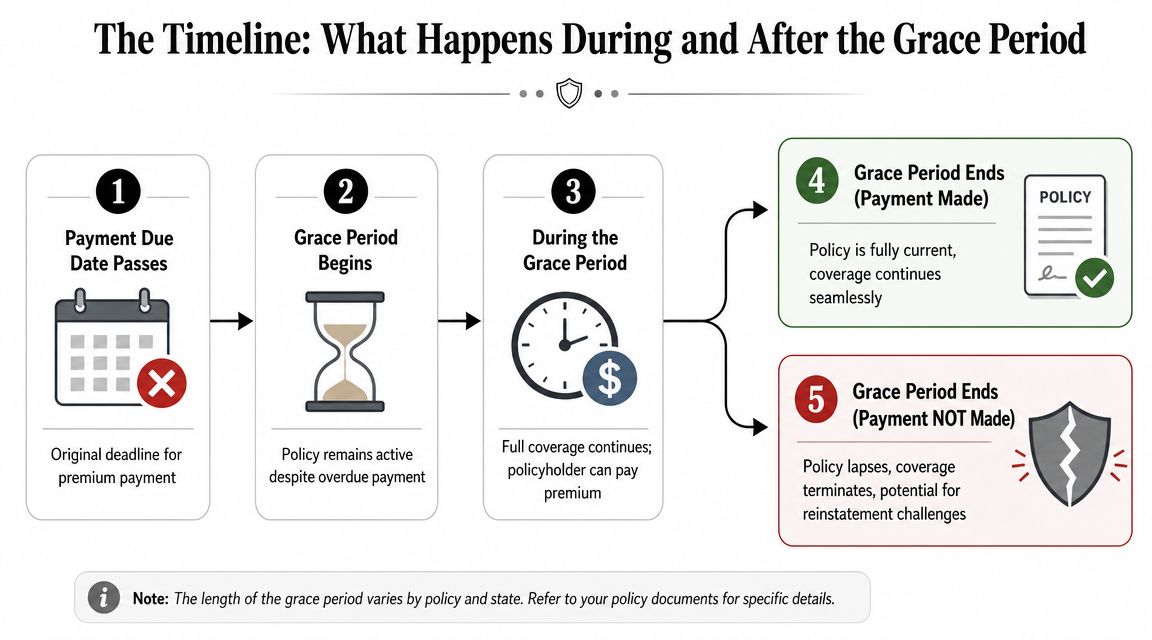

The Timeline What Happens During and After the Grace Period

Your payment due date passes on a busy Tuesday. On Wednesday, your child needs a prescription refill, and on Friday you remember the premium is still unpaid. That is the moment many families ask the wrong question. The useful question is not only whether a grace period exists. It is what your coverage, claims, and next options look like before the deadline, while the payment is late, and after that window closes.

During the grace period

A grace period works a bit like a late window on a bill. You missed the due date, but the contract may still give you a short stretch of time to catch up before coverage stops.

During that window, three facts matter at once. Your payment is overdue. Your policy may still be active for the moment. The insurer is also counting down to a final date, and that date is the one that matters most.

For life insurance, this temporary protection can make a major difference. In many cases, if the insured dies during the grace period, the policy may still pay, with the overdue premium often deducted from the benefit. The key practical point is simple. Late does not always mean uninsured.

For health insurance, claims can get murkier. A doctor visit or prescription claim filed while premiums are overdue may not be handled the same way throughout the grace period. As noted earlier, some claims may be paid at first, while others may be held pending if the missed premium is not brought current.

A good rule for any policy type is to treat the grace period like a yellow traffic light, not a green one. You still may have coverage, but you should not assume every claim will go through normally without checking.

What happens to claims

This type of confusion often results in financial loss.

Submitting a claim during the grace period does not guarantee the claim is safely paid and final. It only means the claim entered the system. Whether it stays paid, gets paused, or gets denied can depend on the policy type, the timing, and whether you catch up before the deadline.

Use this quick framework:

- Before the grace period ends: the insurer may still treat the policy as active, but claim handling can vary.

- If you pay before the deadline: pending claims are more likely to move forward under normal policy rules.

- If you do not pay in time: claims tied to the period after coverage ended may be denied, and even earlier claims can become more complicated.

If you have medical care scheduled, a repair claim open, or a death benefit question in progress, call the insurer and ask a direct question: “Is this claim being processed normally while my premium is overdue?”

If you are switching insurers and a missed payment happens around the same time, review this guide on how to switch insurance providers without creating a coverage gap. Timing mistakes are common when one policy is ending and another is starting.

After the grace period ends

Once the deadline passes without payment, the situation changes fast. The policy can lapse. That usually means coverage stops, and from that point on, a new claim may have no protection at all.

It helps to separate two stages clearly:

- Late: you still have time to fix the missed payment under the policy rules.

- Lapsed: the grace period ended, and the policy is no longer in force.

That difference affects reinstatement too. Reinstatement is not always as simple as paying the old bill. Some insurers let you restore the policy if you act quickly and pay what you owe. Others may require a signed application, proof that the insured is still eligible, or new underwriting, especially for life or health coverage. Auto insurers may require a new policy instead of restoring the old one, depending on the lapse and state rules.

So the timeline usually looks like this. First, you miss the due date. Next, the grace period gives you a short chance to catch up. After that, the policy may lapse. Then, if reinstatement is allowed, you may need to complete extra steps before coverage is active again.

The safest habit is simple. Do not stop at “I paid it.” Ask, “Is my policy fully active now, and is anything else required to reinstate coverage?”

A Practical Action Plan for Handling Missed Payments

Your premium due date passes on a Tuesday. On Wednesday, your child has a doctor visit, or you need to drive to work, and suddenly one question matters: Do we still have coverage right now?

That is the moment to slow down and handle this in order. A missed payment is often fixable, but the steps you take before, during, and after the grace period can change whether coverage stays in place, whether a claim gets paid, and how hard it is to restore the policy if it lapses.

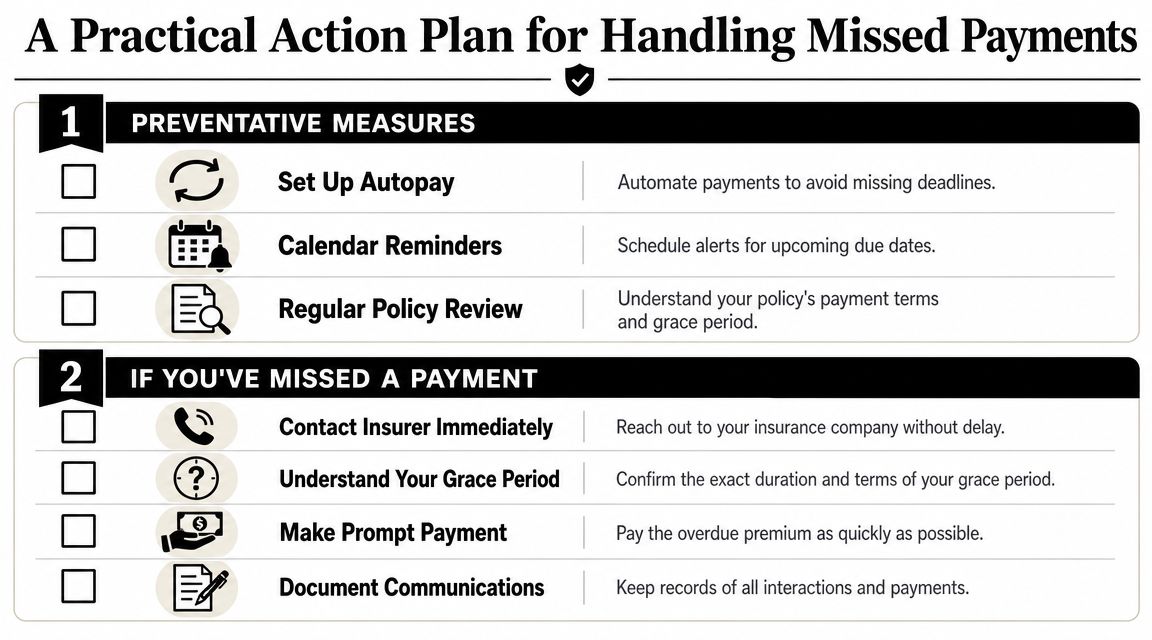

Before you miss a payment

The easiest missed payment to fix is the one that never happens.

Set up a simple backup system. Autopay helps if your income and account balance are steady, but it should not be your only protection. Cards expire. Bank accounts change. Payments can fail without much warning.

A good household routine includes a few basics:

- Turn on autopay if it fits your budget: This lowers the odds that a hectic week leads to a missed bill.

- Add calendar reminders anyway: A reminder a few days before the draft gives you time to catch a card problem or low balance.

- Keep your contact details current: Late notices do not help if they go to an old email address or phone number.

- Review billing settings once a year: Recheck them after changing banks, jobs, cards, or monthly spending plans.

If billing problems are part of why you want a new insurer, read this guide on switching insurance providers without creating a coverage gap before you cancel anything.

If you already missed the due date

Start with one goal. Find out whether you are still inside the grace period and what date ends it.

Then work through these steps:

Read the billing notice and your policy

Look for the due date, grace-period wording, and the last date payment can be accepted to keep the policy in force.Call the insurer right away

Ask clear questions: “Is my policy still active today?” “What is the final date to pay?” “If I file a claim today, how will this late payment affect it?”Ask how claims are handled during the grace period

This part confuses many families. Some policies treat claims during the grace period differently from others. For example, a health insurer may still process covered care during that window under certain rules, while other coverage types may be less forgiving if payment is still outstanding. Get the answer for your specific policy, not a general assumption.Use the fastest payment method available

Online, phone, or same-day payment options may post faster than mailing a check. Ask which method counts as received soonest.Save proof of payment

Keep the confirmation number, screenshot, receipt, and any email showing the amount paid and the time it was accepted.Confirm the policy status after payment posts

Do not stop at “payment submitted.” Ask, “Is my policy fully active with no lapse, and is anything else required from me?”

That last step matters more than it sounds. Payment sent is not always the same as payment posted, and payment posted is not always the same as coverage confirmed.

If the policy already lapsed

A lapse is the point where the grace period has ended and the policy is no longer in force. At that stage, you are no longer solving a late bill. You are trying to restore coverage.

Reinstatement works a lot like reopening a closed account. Sometimes it is simple. Sometimes it is not.

Take these steps in order:

Ask whether reinstatement is still available

Some insurers allow it only for a short time after lapse.Find out exactly what the insurer requires

You may need to pay overdue premiums, pay fees, sign forms, or answer new health or eligibility questions.Ask when coverage becomes active again

This is one of the biggest missed details. Do not assume coverage restarts the moment you make a payment. Ask for the exact effective date.Request written confirmation

Email or portal confirmation is much better than relying on memory from a phone call.Check whether any claims in the gap period are excluded

If the policy had lapsed, claims that happened during that break may not be covered, even if the policy is later reinstated.

This can be especially important with life and health insurance. If the insured person's health or eligibility has changed since the original policy started, reinstatement may involve more than paying the overdue amount.

One smart habit: Write down the date, time, representative name, and what the insurer told you. If there is any dispute later, your notes can save time and reduce confusion.

Your Questions Answered About Insurance Grace Periods

Will using the grace period raise my premium?

A grace period usually does not raise your premium by itself. It is a short window after the due date that gives you time to catch up before the policy ends, as noted earlier in this guide.

What can change is the bill around it. Some insurers charge a late fee. Some do not. Some may stop future claims if the payment never arrives by the deadline. The practical move is simple. Check the notice, log in to your account, or call and ask, “If I pay today, is my policy still active, and is there any extra charge?”

Is a grace period the same as reinstatement?

They are two different stages of the same problem.

A grace period is the overdue window when you may still be able to keep the policy in force by paying what you owe. Reinstatement starts after the policy has lapsed. At that point, you are asking the insurer to turn coverage back on.

A useful way to picture it is a power bill. During the warning period, you can still pay and keep the lights on without a break. After shutoff, getting service back may take extra steps, extra time, and sometimes extra approval. Insurance can work the same way.

Are there always late fees?

No. Late fees depend on the insurer and the policy terms.

The bigger question is often not the fee. It is whether your payment arrives before the grace period ends. A small fee is annoying. A lapse in coverage can be much more expensive if a claim happens at the wrong time.

If I'm in the grace period, are claims automatically safe?

Claims are not automatically safe. This is one of the most confusing parts, and it is where families can get caught off guard.

During the grace period, some policies continue coverage if you make the overdue payment in time. In other cases, claim handling can be delayed, reduced, or denied if the payment is never caught up. Life insurance, health insurance, and auto insurance can each handle this differently.

If you have both a missed payment and a pending claim, ask two direct questions: “Is the policy currently considered in force?” and “How will this claim be handled if I pay within the grace period?” Get the answer in writing if you can.

What if the grace period already ended?

Then the question changes from late payment to reinstatement.

Reinstatement may require more than sending money. The insurer may ask for the overdue premium, forms, fees, or updated health or eligibility information. Just as important, ask for the exact date coverage starts again. If there was a gap, a claim during that gap may not be covered.

What's the main takeaway?

A missed payment has three phases: before, during, and after.

Before the deadline, you still have room to fix the problem. During the grace period, confirm the final payment date and ask how any current claim will be treated. After the grace period ends, ask right away whether reinstatement is available and when coverage would become active again. That sequence helps you avoid the biggest mistake, assuming coverage is still there without checking.

If you're shopping for life insurance that feels simpler to manage, Coveredly offers a digital-first experience built for busy families and professionals. You can explore flexible term life coverage online and find an option that fits real life without the old-school friction.