You might be dealing with this right now. A new employer sends over onboarding forms and asks you to complete a health risk assessment. Or an insurer asks for health information and you wonder whether this is a routine questionnaire, a medical exam, or something that could affect what you pay for coverage.

That uncertainty is normal. It's not widely understood what a health risk assessment is, how it works, or why it shows up in both workplace wellness and insurance conversations. It can feel personal because it is personal. You're being asked about your body, your habits, and in some cases your family history.

The good news is that an HRA is much easier to understand once you see it for what it is. Think of it as a structured way to take stock of your health today so decisions about care, benefits, and sometimes insurance can be made with more clarity. When you understand the process, it feels less like a black box and more like a tool you can use to protect both your health and your financial stability.

Table of Contents

- An Introduction to Health Risk Assessments

- What Exactly Is a Health Risk Assessment

- The Common Components and Types of HRAs

- How Employers and Insurers Use HRA Data

- Your Privacy During the HRA Process

- From HRA Insights to Smart Insurance Choices

An Introduction to Health Risk Assessments

A health risk assessment, often shortened to HRA, is one of those terms people hear before they understand it. If you're filling one out for work, for Medicare-related enrollment, or during an insurance process, you might wonder whether you're being judged, diagnosed, or sorted into a pricing bucket.

In practice, it's usually much more straightforward than that. An HRA gathers health information in a structured way so a plan, employer, or care team can spot risks early and connect people to the right next step. That could mean preventive care, follow-up with a doctor, wellness support, or more informed insurance decisions.

Early visibility significantly alters outcomes. One reason HRAs exist is to close gaps in preventive care. The Commonwealth Fund notes that approximately 33% of breast cancer cases are not detected until they reach a late stage, where treatment costs are significantly higher, which highlights why earlier risk identification matters for both health and finances (Commonwealth Fund on health risk assessments).

A useful way to think about an HRA is this. It doesn't predict your future with certainty. It helps people make better decisions before small issues become expensive problems.

That last part is where many readers connect the dots. Health decisions and money decisions are tied together. Missing preventive care can affect out-of-pocket costs, time away from work, and the types of insurance options available to you later.

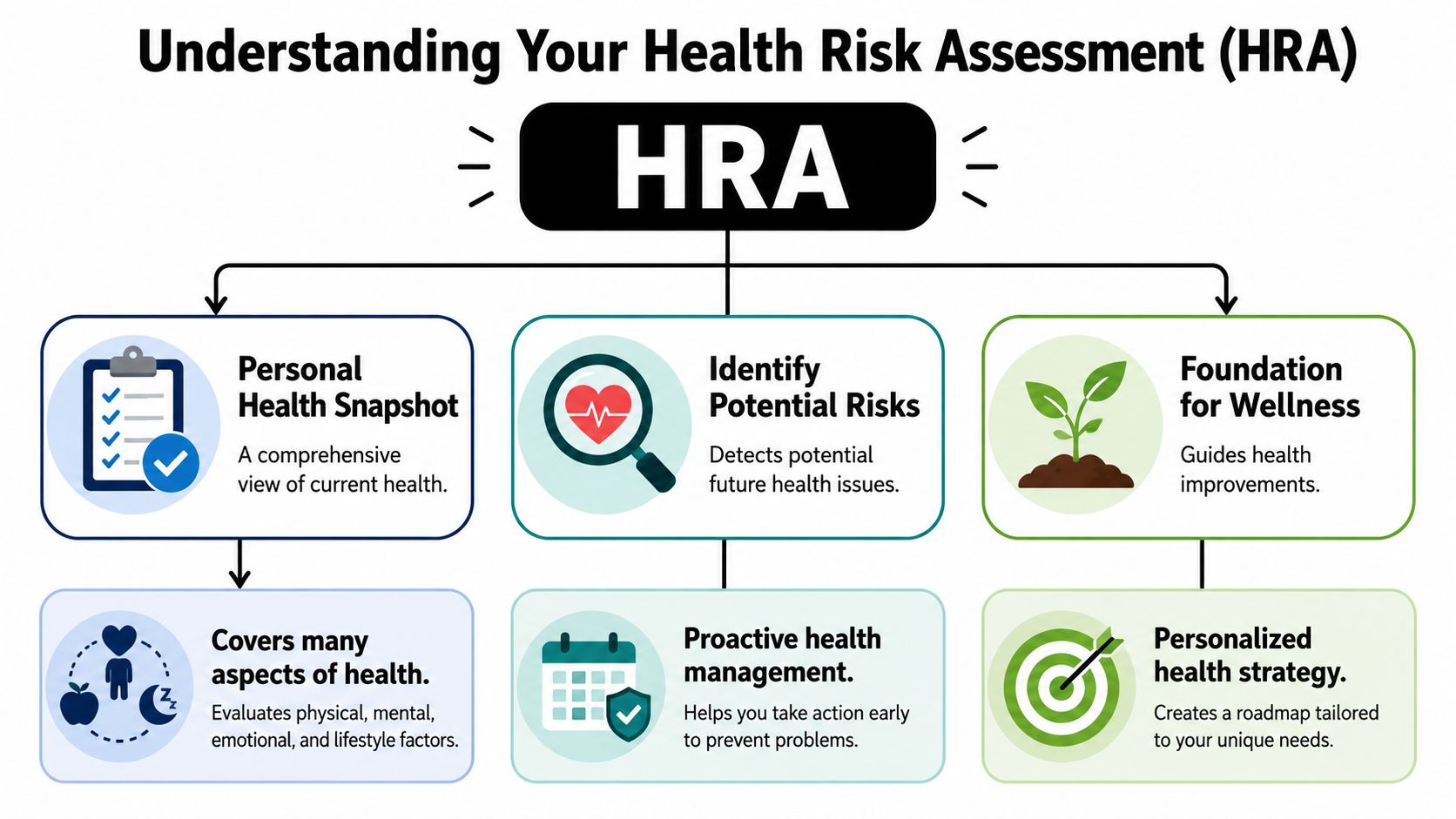

If you've been asking what is a health risk assessment, the short answer is that it's a structured health snapshot. The more helpful answer is that it's a tool that can influence wellness programs, clinical follow-up, and sometimes the path you take to secure financial protection for your family.

What Exactly Is a Health Risk Assessment

You fill out a health questionnaire during open enrollment, then months later you apply for life insurance and get asked many of the same health questions again. That overlap surprises people. Workplace wellness, clinical screening, and insurance underwriting often feel like separate systems, but they all rely on one basic idea: better information can lead to better decisions.

A Health Risk Assessment is a structured process that gathers health information, reviews it for patterns, and returns guidance based on what it finds. The CDC describes it as having three core elements: a confidential questionnaire, a quantitative risk calculation or scoring algorithm, and personalized feedback that connects the individual to specific health interventions (CDC definition summarized on Wikipedia).

In plain English, an HRA helps organize scattered pieces of health information so someone can decide what to do next.

A planning tool, not a verdict

People often hear the word "assessment" and assume judgment. They picture a pass-or-fail test or a medical exam that labels them high risk. That is usually not what is happening.

An HRA works more like a planning worksheet. A financial advisor would not build a retirement plan from one number on one statement. They would ask about income, debt, savings habits, dependents, and goals because context changes the recommendation. An HRA follows that same logic with health information. It gathers details that make the next step more useful.

That distinction matters for your peace of mind. The goal is not to catch you doing something wrong. The goal is to spot patterns early enough that you, your employer, a health plan, or an insurer can respond in a smarter way.

The three moving parts

An HRA usually works through three connected parts:

The confidential questionnaire

You answer questions about health history, daily habits, current conditions, and sometimes family background. Those answers provide context that a lab value alone cannot.The scoring or risk calculation

A formula reviews your answers and estimates where future problems may be more likely. It does not predict your future with certainty. It sorts information into risk patterns that can guide attention and follow-up.The personalized feedback

This is the part that gives the process value. Useful feedback may point you toward preventive care, a doctor visit, wellness coaching, or another action that fits the risk identified.

Without feedback, it is just data collection.

Practical rule: If a questionnaire asks for personal health details but provides no explanation, no follow-up, and no path toward prevention or care, it is missing the part that makes an HRA useful.

This also helps explain why HRAs matter financially. In the workplace, the results may shape wellness outreach or benefit recommendations. In insurance, similar health details can affect underwriting, pricing, or whether an exam is requested. If you are comparing traditional coverage with life insurance options that may not require a medical exam, understanding the HRA process gives you a clearer sense of why some applications ask for detailed health information and others rely on different underwriting models.

The short version is simple. An HRA is a method for turning health details into next-step guidance. For readers thinking about both wellness and financial protection, that makes it more than a form. It is one of the places where health planning and insurance planning start to meet.

The Common Components and Types of HRAs

The easiest way to understand an HRA is to look at what goes into it. Most HRAs combine information you report about yourself with, in some settings, biometric data collected through screenings or provider records.

What you report yourself

The self-reported portion usually feels familiar. It often asks about everyday behaviors and background factors that shape health risk over time.

Common categories include:

- Lifestyle habits such as exercise, diet, smoking, sleep, and alcohol use

- Personal medical history including diagnosed conditions, medications, or past procedures

- Family history because some health patterns run in families

- Mental and social factors such as stress, support systems, or barriers to care

- General health status covering how you view your overall health and daily functioning

These questions matter because risk doesn't come from one source. It usually develops from a mix of behavior, biology, and access to care.

What a biometric screening may add

Some HRAs stop with the questionnaire. Others add a biometric layer. For Medicare beneficiaries, clinical validity has a more specific standard. To be clinically valid for Medicare beneficiaries, an HRA must include specific biometric assessments, including blood lipids (HDL/LDL cholesterol, triglycerides), blood glucose, and systolic/diastolic blood pressure, reconciling self-reported data with provider-obtained metrics (CMS guidance on clinically valid HRA biometric assessments).

That tells you something useful. Self-reported information has value, but measured data can sharpen the picture.

A simple comparison helps:

| HRA input | Example | Why it matters |

|---|---|---|

| Self-reported information | You say you exercise rarely or have a family history of diabetes | It gives context that numbers alone can't show |

| Biometric information | Blood pressure, blood glucose, blood lipids | It helps confirm current health status with measurable data |

| Combined view | Questionnaire plus screening | It creates a fuller risk profile |

If you're trying to understand how this overlaps with insurance processes, some traditional underwriting paths may involve similar kinds of health review or follow-up. If you want a clearer picture of where medical exams fit into life insurance, this guide to life insurance medical exam topics can help connect the dots.

Not every risk assessment is a personal HRA

People sometimes mix up personal health HRAs with environmental or toxicological risk assessments. They aren't the same thing. A personal HRA focuses on an individual or covered population's health factors. Environmental health risk assessment uses a separate framework to study hazards, exposure, dose-response, and risk characterization in relation to chemicals or other stressors.

That distinction matters because the same words can mean different things in different industries. When an employer, doctor, or insurer talks about an HRA, they're almost always talking about your health profile and preventive planning, not a laboratory-style analysis of chemical exposure.

How Employers and Insurers Use HRA Data

You fill out a health questionnaire at work, then later apply for life insurance and see another set of health questions. That can feel like the same information is being pulled into the same system. It usually is not.

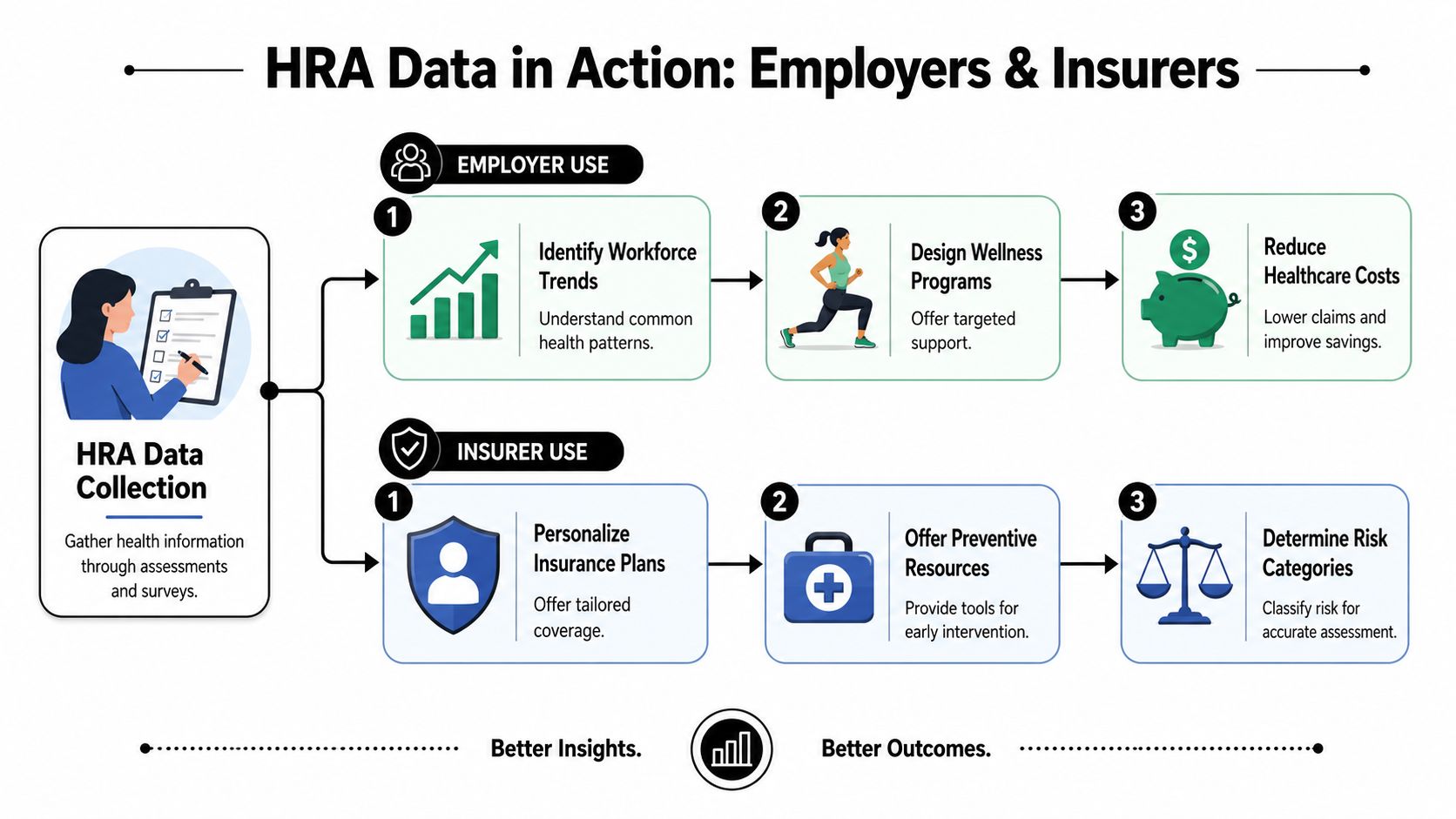

The questions may look similar, but the purpose behind them is different. An employer usually uses HRA results to spot patterns across a workforce and decide where support is needed. An insurer uses health information to estimate risk for one applicant and decide how to price or approve coverage. That distinction matters because it affects both your privacy expectations and your financial planning.

Employers use HRA data to plan benefits, not price your policy

In a workplace setting, an HRA works a lot like a budget review for health benefits. A company is trying to see where the bigger pressure points are so it can spend wellness dollars more wisely.

If a large share of employees report stress, poor sleep, or trouble getting preventive care, the employer may respond by adjusting programs and communication. That can mean adding screening reminders, improving benefits education, expanding mental health support, or making it easier to access primary care.

The value is in the pattern, not in following one person around.

A few common examples make this clearer:

- Frequent reports of high stress can lead to counseling resources or mental health benefit reminders.

- Repeated signs of unmanaged blood pressure or blood sugar concerns can lead to screening campaigns and preventive outreach.

- Reports that employees do not understand their benefits can push the employer to simplify enrollment materials or explain coverage better.

For you, that can translate into earlier support and fewer expensive surprises later. Better preventive care often protects more than health. It can also help protect your out-of-pocket costs.

Insurers use health information to evaluate individual risk

Insurance works from a different starting point. The insurer is not trying to improve a whole workforce. It is trying to answer a narrower question: how much risk does this one application represent?

That is why traditional life insurance underwriting may involve health questionnaires, prescription history, medical records, and sometimes a medical exam. If you want to see how that process is typically structured, this guide to underwriting in life insurance gives useful context.

A practical way to view it is this. An employer uses HRA data like a company looking at neighborhood traffic patterns before adding a stoplight. An insurer uses health data more like a lender reviewing one borrower's finances before approving a loan. Both are assessing risk. They are just making different decisions from it.

Why this difference matters for your insurance choices

Here, workplace wellness, clinical data, and personal finance start to overlap in a real-world way.

If your health profile suggests higher risk, a traditional insurer may ask more questions or require more documentation. That can affect how long underwriting takes and what rate you are offered. By contrast, some modern no-exam life insurance options rely on efficient underwriting, which can reduce the need for lab work or in-person screening for eligible applicants.

That does not mean health stops mattering. It means the path can look different.

For someone comparing coverage options, this matters for peace of mind as much as convenience. A traditional route may offer one set of pricing and requirements. A no-exam option may offer a faster, simpler application experience. Understanding how health data is used helps you choose the route that fits your timeline, budget, and comfort level.

One set of health questions can lead to wellness support at work. A similar set can shape an insurance offer at home. Knowing which system you are in helps you make smarter decisions with fewer surprises.

Your Privacy During the HRA Process

Privacy is usually the underlying concern behind the technical questions. People don't just ask what is a health risk assessment. They also want to know who sees it, what happens to the answers, and whether personal details can be used in ways they didn't expect.

That concern is reasonable. Health information is sensitive, and any legitimate HRA process should treat it that way.

What stays private

A strong baseline fact helps here. Health risk assessments are confidential tools used by employers to measure workforce health. Employees complete secure health questionnaires and optional biometric screenings to reveal trends and guide preventive wellness strategies, with data used to identify gaps in care (CDC health status page describing confidential HRA use).

The key word is confidential. In practice, that usually means your identifiable health information is handled under clear privacy rules, secure systems, and limited-access processes. In employer settings, organizations often rely on aggregate or de-identified trends for planning rather than handing managers a file of personal medical details.

That's an important distinction:

- Identifiable data points to you as an individual

- Aggregate data groups responses together to show trends without centering one person's identity

If your employer says an HRA supports wellness planning, the useful question isn't just "Are they collecting information?" It's "How is that information separated, stored, and reported?"

Your answers should lead to support, not office gossip. A legitimate HRA process is built with that principle in mind.

What to look for before you participate

You don't need to be a compliance expert to spot whether an HRA process looks credible. A few practical checks go a long way.

Secure access

Use caution if a form asks for detailed health information through a casual email attachment or an unprotected page. Reputable programs typically use secure portals.Clear privacy language

You should be able to find a privacy notice explaining who collects the information, how it's used, and whether results are shared in summarized form.Defined purpose

The HRA should connect to a real use case such as wellness planning, preventive care, enrollment requirements, or benefit design. Vague collection without a clear purpose is a red flag.Optional versus required elements

Some parts, especially biometric screenings in certain employer settings, may be optional. Others, such as Medicare-related assessments in specific contexts, can be part of standard care or plan administration.

Many readers also wonder about HIPAA. While the exact legal setup can vary by program, the practical takeaway is simple. Legitimate health processes are expected to protect personal information, limit unnecessary access, and communicate how data is handled. If that information isn't available, ask for it before you proceed.

Peace of mind comes from understanding the rules of the road. You don't have to participate blindly.

From HRA Insights to Smart Insurance Choices

A health risk assessment gives you knowledge. That's its real value. It can show where preventive action makes sense, where follow-up care could save trouble later, and where your current health picture may affect insurance decisions.

For some people, that information feeds into a traditional underwriting process. For others, it creates a different insight. If your health picture is relatively straightforward, you may not want a slow, exam-heavy route just to put financial protection in place.

Turning health knowledge into financial action

That shift matters for young families, newly married couples, and busy professionals. They often don't need more paperwork. They need a practical way to turn health awareness into coverage that protects income, debts, children, or a partner.

Modern no-exam life insurance options fit that need well. They can reduce friction for people who want coverage without scheduling a nurse visit, lab work, or a long back-and-forth process. If you're comparing options, this guide on how to choose the right life insurance policy is a strong place to start.

The main takeaway is simple. An HRA isn't just a health form. It's a decision tool. It helps reveal where risk may exist, where prevention may help, and how you might want to approach insurance planning.

If you've been asking what is a health risk assessment, the answer is no longer just a definition. It's a process that sits at the intersection of wellness, healthcare, benefits, and financial planning. Once you see that connection, the form becomes less intimidating and more useful.

If you're ready to turn health awareness into practical protection, Coveredly offers a modern way to explore life insurance online. Their approach is built for real life: digital, flexible, and designed to help many applicants get term coverage without the hassle of traditional exams.