You might be reading this while comparing daycare costs, signing mortgage paperwork, or updating beneficiaries after a wedding. In seasons like that, life insurance often gets pushed to the side because it feels technical and easy to postpone.

Term life insurance is simpler than it sounds. It gives your family a financial cushion for a set number of years, usually the same years when your paycheck is doing the heaviest lifting. If something happened to you during that period, the policy could help cover everyday bills, childcare, college savings, or the mortgage so your family is not forced to rebuild at the worst possible time.

A useful way to frame it is this. Term life is built for protection, not for building savings. That point matters because many people get tripped up by product names and start wondering about options like cash value term life insurance, even though term coverage is generally chosen for straightforward income protection.

Waiting usually makes coverage more expensive, which is one reason this decision matters earlier than many young families expect. So if you have people who rely on your income, understanding what a term life insurance policy is can directly affect how well you protect your home, your budget, and the goals your family is counting on.

Table of Contents

- What Term Life Insurance Is And What It Is Not

- The Mechanics Of A Term Life Policy

- Who Needs Term Life Insurance And Why

- Term Life vs Whole Life Insurance Explained

- How Much Term Life Insurance Costs

- How To Get A Term Life Insurance Policy Today

- Frequently Asked Questions About Term Life

What Term Life Insurance Is And What It Is Not

Think of term life insurance the way you'd think about renting versus buying. Renting gives you housing for a set period. It does the job you need right now, but it doesn't build ownership. Term life insurance works in a similar way. It gives you protection for a fixed period, not forever.

A term life insurance policy is a type of life insurance that provides a guaranteed death benefit for a specific period, such as 10, 20, or 30 years, without building cash value. If the insured person dies during that term, the insurer pays the death benefit to the beneficiaries. If the insured person outlives the term, coverage usually ends and no payout occurs.

What term life does

Term life is built for one job. It replaces financial support if you die during the years your family or business would struggle most without you.

That can mean helping your spouse stay in the house, giving your children a financial cushion, or making sure debts don't fall on the people you love.

What term life does not do

It's not an investment account. It doesn't build a savings component. It doesn't create cash value you can borrow from later.

If you've come across the phrase cash value term life insurance, it helps to know that the defining feature of term insurance is that it does not accumulate cash value. That's one of the reasons it stays simpler and usually more affordable than permanent coverage.

Practical rule: Buy term life for income protection and obligation protection. Don't expect it to function like a savings vehicle.

Term life is also far from a niche product. According to Grand View Research's term insurance market report, the global term insurance market was valued at approximately USD 1.06 trillion in 2023 and is projected to reach about USD 1.9 trillion by 2030. In the United States, term products made up 39.3% of all new life-insurance policies sold in 2022. In other words, lots of people asking the same questions you are end up choosing term.

The Mechanics Of A Term Life Policy

Once you know the definition, the next question is usually, “How does the policy work?” The good news is that term life is one of the easier financial products to understand once you break it into parts.

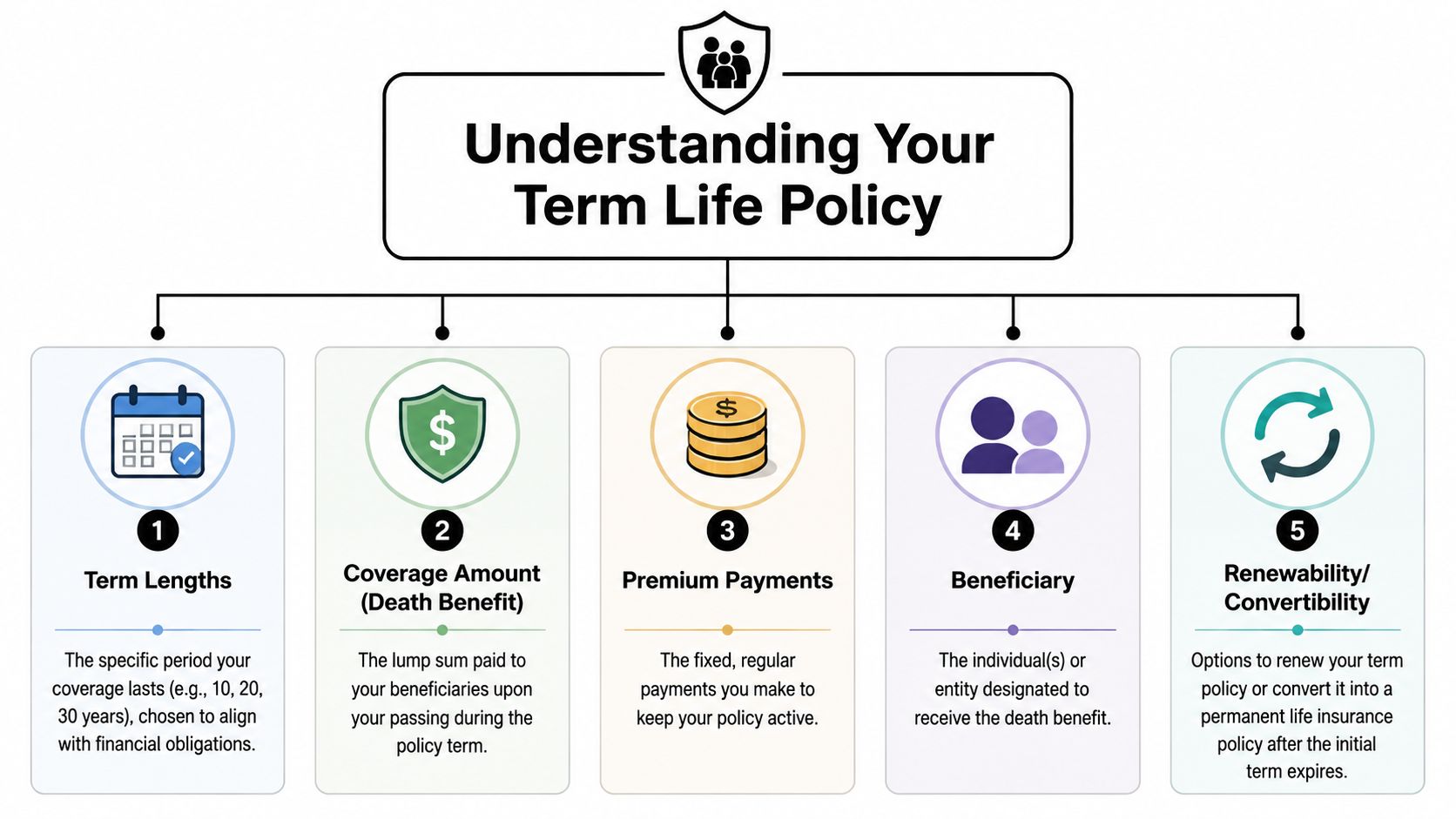

The four moving parts

Most term policies revolve around four decisions:

Term length

This is how long your coverage lasts. Common choices are 10, 20, or 30 years. People often match the term to a real obligation, such as the years left on a mortgage or the period until children are financially independent.Premium

This is the amount you pay to keep the policy active. Many people prefer level term life insurance because the premium stays the same through the policy term.Death benefit

This is the lump sum paid to your beneficiaries if you die while the policy is active. The death benefit is paid tax-free as a lump sum under the policy framework described by Allstate.Beneficiary

This is the person or people you choose to receive the money. For many young families, that's a spouse, children through a trust structure, or another close family member.

Why level premiums matter

One of the biggest reasons people choose term is predictability. A common structure is the level-premium policy, which means your premium stays constant during the term even if your health changes later.

That matters more than many buyers realize. If you develop a medical condition after buying the policy, the locked-in premium can protect your budget during the years when you still need coverage.

By contrast, Titan Wealth International's explanation of term life insurance notes that yearly renewable term policies increase premiums annually as risk rises. That structure can become harder to manage over time.

A level premium turns life insurance into a planning tool, not a moving target.

Why term is usually cheaper

Term life is affordable for a straightforward reason. The insurer may never have to pay a claim if the policy ends before the insured dies. Permanent insurance works differently because it's designed to last for life.

That difference in structure reduces the insurer's long-term risk. It also helps explain why term coverage often gives young families and professionals access to a larger death benefit for a lower monthly cost than permanent options.

Renewability and convertibility

Some policies include features that add flexibility later:

- Renewable policies let you continue coverage after the initial term, usually on a year-to-year basis, though premiums typically rise with age.

- Convertible policies let you switch to permanent coverage without a new medical exam, which can be valuable if your health has changed.

These features don't make a term policy permanent. They just give you options when life changes faster than expected.

Who Needs Term Life Insurance And Why

The question isn't whether term life is “good.” The better question is whether someone would face a financial problem if you weren't around tomorrow. If the answer is yes, term life deserves a serious look.

Newly married couples and new homeowners

A lot changes quickly after marriage. You may combine finances, sign a lease together, buy a home, or start planning for children. At that point, your income often stops being “just yours.” It supports a shared life.

Term life can help cover the years when that partnership is financially vulnerable. If one spouse dies, the surviving spouse may still need to handle the mortgage, utilities, and day-to-day expenses on one income.

Parents with young children

For parents, the purpose becomes even more concrete. Children don't just need food and housing. They need stability, time, and options.

A term policy can create breathing room for the surviving parent. That might mean time off work, help with childcare, or the ability to stay in the same home and school district during a difficult transition.

Parents often choose a term that lasts through the years their children are most financially dependent on them.

For a quick overview of how families think about coverage, this video is a useful starting point:

Professionals and business owners

Term life also matters for people without kids. If someone co-signed a loan with you, depends on your income, or would inherit business obligations, your death could create immediate financial pressure.

Common examples include:

- A business loan that needs to be repaid

- A buy-sell arrangement where remaining owners need funds to continue the company

- A partner who relies on your income even if you don't have children

A simple gut check

You probably need term life if one or more of these statements is true:

- You share expenses with a spouse or partner

- You have children who rely on your income

- You carry a mortgage or significant debt

- You own a business or have business-related obligations

- Someone would need money to maintain stability after your death

If none of those apply, coverage may be less urgent right now. But for many busy young professionals and parents, term life solves a very real problem: it protects the people and commitments that depend on them.

Term Life vs Whole Life Insurance Explained

Most confusion about life insurance starts here. People hear “term” and “whole” and assume one is basic while the other is better. That's not the right framework. These two products are built to do different jobs.

Term life insurance focuses on temporary protection. Whole life insurance combines lifelong coverage with a cash value component. That structural difference affects cost, flexibility, and the reason someone buys it.

Term Life vs. Whole Life Insurance at a Glance

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Coverage length | Fixed period | Lifelong coverage |

| Main purpose | Income protection and risk transfer | Lifelong protection plus cash value |

| Cash value | None | Builds cash value over time |

| Cost for equivalent death benefit | Lower | Typically much higher |

| Payout timing | Only if death occurs during active term | Designed for lifelong coverage |

The cleanest way to think about term life is as pure protection. You pay for coverage during a specific window, and the policy pays only if death happens in that window. There's no savings feature attached.

Whole life works differently. It can build cash value over time, which is why people sometimes look at it as both insurance and a financial asset. But that added feature changes the price.

According to Allstate's overview of term life insurance, term policies contain zero cash value and operate strictly as a risk transfer mechanism. The same overview notes that whole life policies can build cash value over time, and term is typically far less expensive. Related industry guidance cited in the verified data puts whole life premiums at 6x to 10x more than term for an equivalent death benefit.

Why many young families lean toward term

For a young parent or homeowner, the biggest need is often protection during a high-responsibility phase of life. That's when affordable coverage matters most. A larger death benefit at a manageable monthly cost can be more useful than a permanent policy that strains the household budget.

That doesn't make whole life wrong. It means you should match the product to the goal.

- If your goal is protecting income during child-raising years, term often fits.

- If your goal is lifelong coverage with a cash-value component, whole life may fit better.

- If budget is tight, term often lets you prioritize protection first.

The best policy isn't the one with the most features. It's the one that actually protects your family without breaking your budget.

One more key distinction: when a term policy ends, coverage ends unless you renew or convert it. Whole life is built to remain in force as long as required premiums are paid. That permanence can appeal to some buyers, but many younger households choose term because it aligns better with temporary obligations like a mortgage or child-rearing years.

How Much Term Life Insurance Costs

A lot of young parents and homeowners put life insurance in the “deal with later” bucket. That delay can be expensive in a very literal way. With term life, waiting often means paying more for the same protection.

For many healthy applicants, term life is less expensive than they expect. Your premium is mainly based on age, health, tobacco use, the coverage amount, and how long you want the policy to last.

A real cost example

One common benchmark helps make term life feel more concrete. A healthy 30-year-old nonsmoker may be able to buy a 30-year, $500,000 policy for around the cost of a few streaming subscriptions each month. The exact number varies by insurer and health class, but the bigger point is simple. Basic income protection is often more affordable than people assume.

That matters because guessing wrong has a cost. If you assume coverage is out of reach and wait a few years to check, you may end up paying more than you would have if you had looked sooner.

You can also compare options side by side using tools that help compare term life insurance rates.

What changes your premium

Insurers price term life a lot like lenders price a mortgage. They are trying to measure risk over time.

Five factors usually do the heavy lifting:

- Age at purchase. Younger applicants usually get lower rates because insurers expect lower near-term risk.

- Health history. Blood pressure, medical conditions, medications, and family history can affect pricing.

- Smoking or nicotine use. Tobacco rates are often much higher.

- Coverage amount. A larger death benefit usually means a higher premium.

- Term length. A 30-year term usually costs more than a 10-year term because the insurer is covering a longer period.

Age tends to be the easiest factor to understand. It also creates the most avoidable regret.

The cost of waiting

As noted earlier, delaying the purchase of term life can raise cumulative premiums by roughly 8% to 10% for each year you wait over a 30-year horizon. That does not mean every insurer raises every quote by the same percentage each birthday. It means time works against you.

A simple way to think about it is locking in a mortgage rate. If you qualify for a better rate today, waiting does not improve the offer just because you postponed the paperwork. Term life works similarly. Buying younger can let you secure a lower premium for the full level term.

That is why procrastination is not neutral here.

If you wait several years, two things can happen at once. You are older, which usually pushes rates up, and your health has had more time to change. Even a small shift in blood pressure, weight, or medical history can narrow your options.

Buying term life early is often less about fear and more about preserving flexibility and affordability during the years your family depends on your income.

You can see the age effect in published rate examples. Quotacy's sample pricing shows that a 50-year-old male in excellent health could pay about $138 per month for a 30-year, $500,000 term policy, compared with much lower rates at younger ages, according to Quotacy's term life insurance rate chart. Your quote may be higher or lower, but the direction is clear. The same coverage usually gets more expensive as you get older.

Why affordability should be viewed over the full term

Monthly cost matters, especially if you are balancing childcare, a mortgage, or student loans. But the smarter question is not just, “Can I afford this this month?” It is, “What would it cost my family if I wait?”

A level term policy gives you pricing stability during the years when your financial obligations are often at their highest. If you lock in a manageable rate while you are young and healthy, you are not just buying coverage for today. You are buying predictability for the years ahead.

How To Get A Term Life Insurance Policy Today

Buying term life used to feel like a project. Long paperwork, agent appointments, and medical scheduling turned a simple need into a multi-step hassle. Today, the process is often much more direct.

If you're busy, the goal is to make a good decision without turning it into a second job.

Start with the obligation, not the product

Before you apply, think about what needs protection. Your policy should reflect real responsibilities.

A useful way to frame it is to ask:

- Who relies on my income right now?

- What debts or commitments would remain if I died?

- How long would those obligations last?

That gives you the rough shape of the policy. A parent might think in terms of raising children to adulthood. A homeowner might think in terms of the mortgage. A business owner might think in terms of loan protection or continuity.

Gather the basics

Most applications ask for the same core information. Have these ready before you start:

- Personal details like your age, address, and occupation

- Health background including medications and medical history

- Coverage choices such as term length and death benefit

- Beneficiary information so the payout goes where you intend

This step usually goes faster than people expect when you collect everything in advance.

Apply online

Modern life insurance applications are designed for speed. You answer questions, review quotes, choose coverage, and submit your application digitally.

For many applicants, the process is much less intimidating than they imagined. Some policies may also be available without the traditional medical exam, depending on the insurer, the coverage amount, and your profile.

Review the policy before you accept it

Don't stop at the monthly price. Read the details that affect how the coverage behaves later.

Focus on:

- The term length and whether it matches your need

- Premium structure and whether it stays level

- Renewal options if you outlive the initial term

- Conversion options if your needs change

A good term life policy should feel clear, not mysterious. If the language seems confusing, ask questions before you sign. Life insurance is one of those products where clarity now can prevent stress for your family later.

Frequently Asked Questions About Term Life

What happens if I outlive my term policy

In most cases, the policy ends and there's no payout if you're still alive when the term expires. Depending on the policy, you may have the option to renew coverage for another period or convert to a permanent policy. Renewal usually costs more because you're older at that point.

Can I have more than one life insurance policy

Yes. Many people carry more than one policy when they want coverage for different needs. For example, someone might use one policy to protect family income and another to cover a specific debt or business obligation. The key is making sure the total coverage still matches a real financial need and that the premiums fit your budget.

Is the death benefit really tax-free

Under the policy framework described in the verified data, the death benefit is generally paid tax-free as a lump sum to beneficiaries if death occurs during the active policy term. That tax treatment is one reason life insurance can be such a useful protection tool for families. If your estate planning is complex, it's smart to confirm details with a qualified tax or legal professional.

If you're ready to turn this from a “someday” task into a completed one, Coveredly is built for exactly that. It offers online term life insurance designed to be digital, affordable, and flexible, with up to $3 million in coverage and no exams for most applicants. For busy parents, newly married couples, and professionals, it's a straightforward way to get coverage that fits real life.