You're probably here because someone pitched VUL life insurance as a smart two-in-one move. Get life insurance. Build wealth. Stay flexible. Maybe it came up during a chat with a financial advisor, a friend in finance, or one of those late-night research sessions after getting married, having a baby, or realizing people depend on your income.

That pitch is appealing because it promises efficiency. One product, two jobs. But VUL is frequently purchased without the buyer's full understanding. It is acquired because the story sounds polished, and the details are hard to follow in real time.

If you've read a few explanations and still feel fuzzy on how it works, that's normal. VUL can be one of the more complicated types of life insurance. It mixes long-term protection with market-based investing, and that combination creates both flexibility and risk. For a broader foundation before you go deeper, this smart person's guide to life insurance is a helpful starting point.

This guide takes the sales gloss off. You'll see what VUL is, how money moves inside the policy, where people get burned, and when a simpler setup may fit better.

Table of Contents

- Introduction

- What Is Variable Universal Life Insurance?

- How VUL Mechanics Work

- The Real Costs and Market Risks of VUL

- VUL vs Term vs Whole Life Insurance

- Is a VUL Policy Right for You?

Introduction

A common VUL conversation starts like this. You ask about life insurance, expecting to compare term lengths and coverage amounts. Instead, you hear about a policy that can protect your family, build cash value, let you adjust premiums, and grow with the market.

That sounds efficient, especially for a busy young professional who wants to make good financial decisions without building a spreadsheet for every choice. If you're newly married, raising kids, or supporting aging parents, a product that claims to combine protection and investing can feel like a shortcut to doing everything responsibly.

The problem is that VUL isn't a shortcut. It's a layered product. Insurance charges, investment choices, policy fees, and ongoing management all sit under the hood. If you don't understand those moving parts, it's easy to confuse flexibility with simplicity.

Practical rule: If a life insurance product takes more than a few minutes to explain clearly, you should slow down before buying it.

That doesn't mean VUL is automatically bad. It means you need a sharper lens. A key consideration isn't how VUL presents itself. Instead, the critical question is whether it fits your goals, risk tolerance, and budget better than straightforward insurance plus separate investing.

What Is Variable Universal Life Insurance?

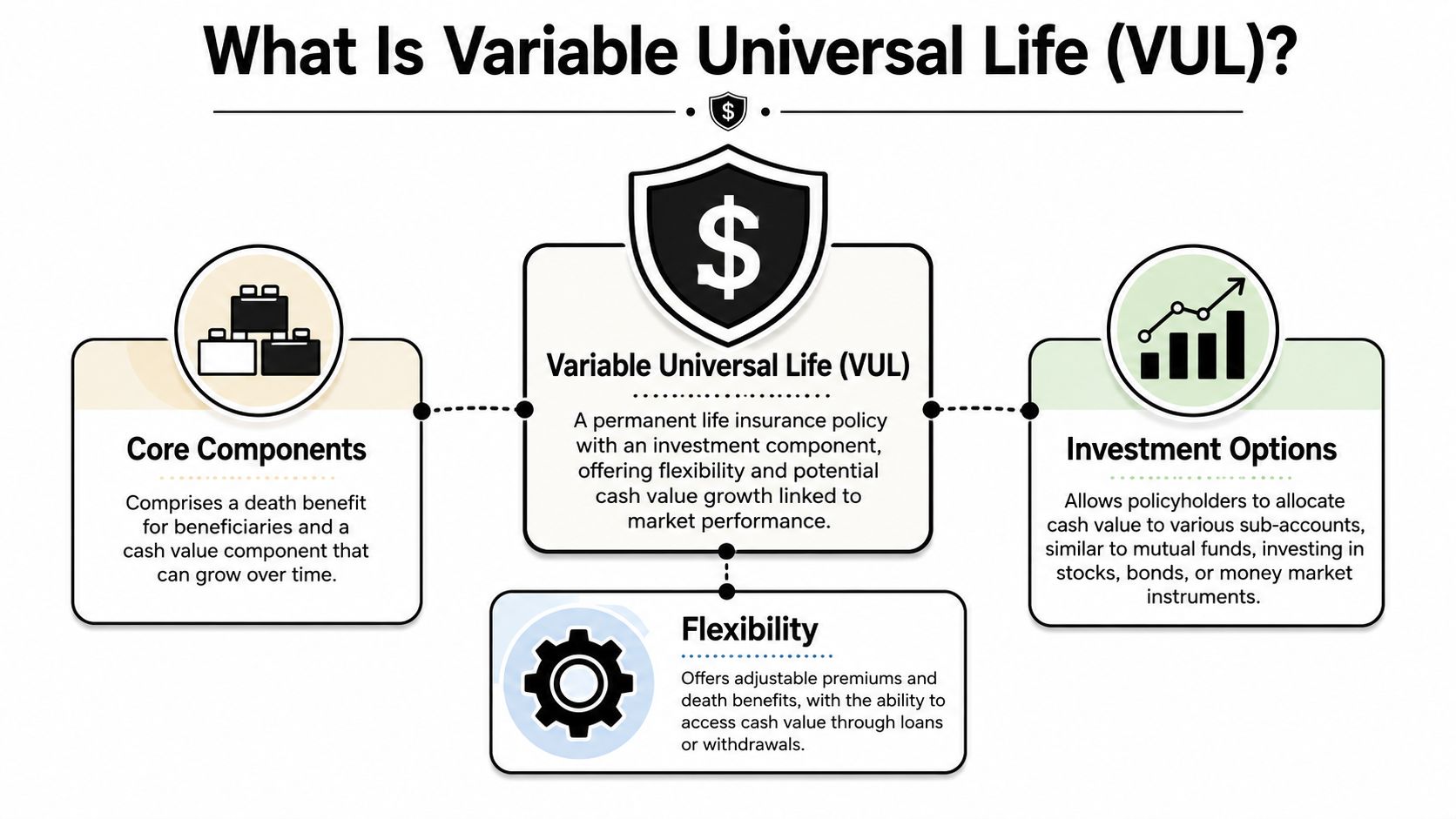

Variable Universal Life insurance, usually shortened to VUL, is a form of permanent life insurance that includes a death benefit and a cash value component you can invest. According to this overview of Variable Universal Life insurance, VUL is a permanent policy that builds cash value in separate accounts similar to mutual funds, and it typically has no endowment age, which means coverage can continue for life as long as there's enough cash value to cover insurance costs.

Think of VUL as a policy with two compartments

One compartment is the insurance chassis. That part exists to pay a death benefit to your beneficiaries when you die.

The other compartment is the investment engine. Money can build inside the policy as cash value, and you direct that money into investment subaccounts. Those subaccounts are generally structured like mutual funds or similar portfolios.

That's the key difference from simpler coverage. With term life, you're mostly buying protection. With VUL, you're buying protection plus an internal investment system.

Why people find VUL attractive

The appeal usually comes down to three ideas:

- Permanent coverage: It isn't built to expire after a set term like 20 or 30 years.

- Cash value growth potential: If the investments perform well, the policy's cash value can grow.

- Flexibility: You may be able to adjust premium payments and parts of the coverage structure over time.

That combination can sound ideal for someone who wants both security and optionality.

Where readers get confused

People often hear “cash value” and assume that means steady growth. That's not how VUL works. The word variable matters. Your cash value is tied to the performance of the investment choices inside the policy. If those investments do poorly, your policy value can fall.

This is why the product needs active attention. You're not just paying for insurance. You're also making allocation decisions that affect whether the policy stays healthy over time.

VUL can work more like owning insurance plus a small investment platform inside the same contract than buying a simple life insurance policy.

The simple definition that actually helps

If you want the plain-English answer to what is VUL life insurance, it's this: a permanent life insurance policy that lets you invest part of its cash value in market-based subaccounts, with the potential for growth and the risk of loss.

That final part matters as much as anything else in this article. Potential for growth and risk of loss come together in the same package.

How VUL Mechanics Work

VUL makes more sense when you follow the money. Each premium payment doesn't go into one bucket. It gets split, and each piece has a job.

Where your premium goes

When you pay into a VUL policy, the insurer first uses part of that money to cover the cost of insurance and other policy expenses. The remaining amount can build cash value inside the policy.

That cash value doesn't just sit there. You usually direct it into a menu of subaccounts. Those subaccounts are similar to mutual funds or comparable investment portfolios, so the value can move up or down with market performance.

This plain-language explanation from Titan Wealth International notes that VUL is a permanent, market-linked policy with flexible premiums and a customizable death benefit, and that the cash value is not guaranteed because it depends on the selected investment options while fees and expenses can reduce accumulated value.

The three moving parts

A VUL policy usually revolves around these connected levers:

Premium flexibility

You may be able to increase, decrease, or sometimes skip premium payments within policy limits.Death benefit structure

The amount your beneficiaries receive can be designed in more than one way.Investment allocation

You choose how the cash value is invested among available subaccounts.

Those levers create flexibility, but they also create responsibility. A VUL owner has more to monitor than someone with a basic term policy.

The death benefit options

According to this summary of VUL death benefit options, VUL policies commonly offer two death benefit designs: a level benefit equal to the original face amount, or a variable benefit equal to the original face amount plus any existing policy account value. The same source notes that premiums are highly flexible and can be increased, decreased, or skipped if the policy's cash value covers costs.

Here's a practical way to think about that:

- Level benefit: More like a fixed target.

- Variable benefit: More like a base amount plus whatever policy value exists.

If your life changes, income rises, or family obligations shift, that flexibility may sound useful. But it also means your decisions inside the policy matter more over time.

Tax treatment and access

Another selling point is tax treatment. This MassMutual explanation of variable life cash value states that cash value grows tax-deferred, owners can access value through loans or withdrawals on a tax-free basis, and beneficiaries typically receive the death benefit income tax-free.

That's a meaningful feature. Tax deferral can make a product more attractive to higher-income buyers who are already using other accounts and want another place to accumulate value.

Still, tax treatment alone doesn't make a policy a good fit. You have to weigh it against the product's costs, investment risk, and maintenance burden.

Why “flexible” doesn't mean carefree

Many buyers hear “you can skip premiums” and think they've found a forgiving policy. That's only partly true. A skipped payment doesn't erase the ongoing cost of insurance. It means the policy may pull what it needs from existing cash value.

If the market has been rough, that cushion may be smaller than you expected. A tool like a cash value life insurance calculator can help you understand how sensitive these policies can be to funding assumptions.

If you underfund a VUL policy for too long, flexibility can turn into pressure later.

That's one of the biggest misunderstandings with VUL. People focus on the freedom to adjust payments. They don't always focus on the fact that the policy still has to pay its own internal costs somehow.

The Real Costs and Market Risks of VUL

The hardest part of VUL isn't understanding the brochure. It's understanding what can go wrong after the brochure is closed.

The investment-first sales story leaves things out

VUL is often marketed as a smarter way to combine protection and growth. That framing can obscure a basic truth. The policy isn't just an investment account. It's an insurance contract with multiple layers of cost built into it.

That matters because every dollar used for policy charges is a dollar that isn't compounding for you inside the investment subaccounts. If returns disappoint, the policy can feel heavy and unforgiving.

Independent criticism has been especially sharp here. The White Coat Investor analysis of VUL policies says they are “rarely a good idea” and can become a “severely under-performing investment” because tax benefits and asset protection often don't offset the costs. That same analysis also warns that the cash value can fall sharply in a down market.

The cost problem

VUL doesn't come with one simple price tag. It can include insurance costs, administrative expenses, and investment-related charges. Even if you understand each item on paper, the combined drag can be hard to appreciate when you're comparing the policy against simple term coverage and a separate brokerage or retirement account.

Here's the practical issue:

- Insurance charges: The policy has to pay for the death benefit.

- Administrative costs: The contract itself has ongoing overhead.

- Investment expenses: The subaccounts have their own cost structure.

- Long-term friction: Layered fees can eat away at policy value if returns are weak or merely average.

For a buyer who mainly wants reliable protection, that's a lot of moving parts.

The market risk is real, not cosmetic

The word variable in VUL is more than branding; VUL cash value rises and falls based on market performance. If the subaccounts lose value, your policy value drops with them.

In some structures, even the death benefit can be affected by poor market performance. That surprises people who assumed “life insurance” meant predictability across the board.

Here's a short explainer if you want to hear the risk argument in a different format.

Policy lapse is the danger people underestimate

A VUL policy can fail in a way that feels backward. You paid premiums. You owned a permanent policy. You expected it to stay in force. But if investment performance is poor, or if you withdraw too much, or if you pay too little for too long, the cash value can get depleted.

This Allstate overview of variable universal life insurance explains that premium payments are flexible and can be skipped if cash value is enough to cover insurance costs, but poor market performance can reduce cash value and risk policy termination if it drops to zero.

That's the part many young families should pause on. A product bought for long-term security can become less secure if it's underfunded or hit by market losses at the wrong time.

Buying VUL because it feels sophisticated can backfire if what you really need is dependable coverage that stays simple under stress.

Why this matters for busy professionals

If your financial life is already full of moving pieces, VUL can add another one that needs supervision. You don't just need conviction about investing. You need discipline around funding, patience during downturns, and comfort with a policy that can become more demanding if assumptions don't hold.

That doesn't make VUL useless. It does make it a poor match for people who want insurance to be boring, clear, and stable.

VUL vs Term vs Whole Life Insurance

When people ask about VUL, they usually aren't choosing in a vacuum. They're deciding between three broad paths: term life, whole life, and Variable Universal Life.

The easiest way to sort them out is to compare what job each one does best. If you want a side-by-side look at universal-style coverage more broadly, this term vs universal life insurance comparison can add context.

Comparison of Life Insurance Types

| Feature | Term Life Insurance | Whole Life Insurance | Variable Universal Life (VUL) |

|---|---|---|---|

| Primary purpose | Pure income protection for a set period | Permanent protection with more conservative cash value features | Permanent protection with market-linked cash value |

| Coverage duration | Temporary | Permanent | Permanent |

| Cash value | No | Yes | Yes |

| Investment risk | No market-based investment component | Generally built for steadier, less hands-on accumulation | Policyholder takes investment risk through subaccounts |

| Premium flexibility | Usually limited | Typically more structured | Flexible within insurer limits |

| Death benefit flexibility | Usually fixed for the term | More structured | Can often be adjusted |

| Complexity | Lowest | Moderate | Highest |

| Best fit | Families who need affordable coverage | Buyers who value permanence and predictability | Buyers comfortable with complexity and market risk |

What term life does better

Term life is usually the cleanest option for young families and professionals with clear protection needs. You pay for coverage during the years when your income matters most to others. If your main concern is replacing income, covering a mortgage, or protecting kids during their dependent years, term often aligns well with that goal.

Its strength is focus. It doesn't try to be an investment account.

What whole life does differently

Whole life appeals to buyers who want permanence and a more structured policy design. It's still more complex than term, but it's generally easier to understand than VUL because the core value proposition tends to be stability rather than market-linked upside.

That makes whole life a different kind of tradeoff. You may gain predictability, but you also give up some flexibility.

Where VUL sits in the lineup

VUL is the option for someone who wants permanent coverage and doesn't mind tying part of the experience to investment markets. This Thrivent explanation of how variable universal life works notes that VUL combines a death benefit with investment subaccounts, flexible premiums, adjustable death benefits, tax-deferred growth, and the risk that poor market performance or excessive withdrawals can drain cash value and terminate the contract.

That's a lot in one product. For the right buyer, that flexibility may be useful. For many others, it can feel like paying extra to make insurance harder to manage.

Simpler insurance often wins because it does one job well and leaves investing to accounts built specifically for investing.

Is a VUL Policy Right for You?

A common VUL buyer story goes like this. You meet with an advisor, hear that your life insurance can also build cash value in the market, and start wondering whether one product can cover two goals at once.

That sounds efficient. Sometimes it is. But combining insurance and investing can also make both jobs harder to evaluate.

Who might consider VUL

VUL tends to fit a narrow group of buyers, not the average person shopping for coverage after getting married, buying a home, or having a child.

A better candidate is someone with a strong financial base already in place. They have an emergency fund, little high-interest debt, and are already using simpler options such as retirement accounts and straightforward life insurance where appropriate. They also have a lasting reason to want permanent coverage, not just a temporary need during peak earning and family-building years.

It also helps if they can tolerate market swings without feeling pressure to change course at the wrong time. VUL asks you to do more than pay a premium. It asks you to monitor a long-term contract whose results depend partly on investment performance and partly on policy costs. That is a lot to keep track of inside something many people only wanted for protection.

In plain terms, VUL can suit a person with higher income, steady cash flow, a long time horizon, and the patience to manage a complex product carefully.

Who should probably avoid it

For many young professionals and young families, VUL solves a problem they do not have.

If your main goal is income replacement, debt protection, or making sure your family can pay the bills if you die, a simpler policy often does that job better. If your budget is still tight, your savings are still growing, or your investing habit is not yet consistent, adding market risk and ongoing policy management to your life insurance can create more friction than value.

The easiest way to frame it is this. Insurance works best when it is boring and reliable. Investing works best when costs are clear and your account is easy to understand. VUL blends those two worlds, which can appeal on paper but create confusion in real life.

It is also a poor fit if you know you will not review statements, ask questions about fees, or respond well to years when returns disappoint. A product that can lose value, require extra funding, or lapse if neglected is rarely the best choice for someone who wants set-it-and-forget-it protection.

Questions to ask before buying

If an advisor suggests VUL, ask the same kind of questions you would ask before buying a house with a variable payment. The sales story usually focuses on the best-case path. Your job is to understand the hard years too.

Ask questions like these:

- What happens if returns are weak for several years? You want to know how much that affects cash value, premiums, and lapse risk.

- What are all the policy charges, and when do they hit hardest? High costs early on can slow growth more than buyers expect.

- How much would I need to contribute to keep this policy healthy in a bad market? A flexible premium does not mean any premium will work forever.

- What is the plain-English reason this policy could fail? If the explanation stays vague, that is a warning sign.

- What would term insurance plus separate investing look like instead? A fair comparison helps you judge whether VUL is solving a real need or just packaging familiar tools in a more expensive way.

If the conversation keeps returning to tax advantages and projected upside, but gives short answers on fees, downside risk, and lapse scenarios, slow down.

The right VUL decision usually starts with skepticism, not excitement. Some buyers will still decide it fits. Many will conclude that keeping insurance and investing separate is easier, cheaper to evaluate, and more aligned with what they need.

If you're sorting through life insurance options and want something simpler, Coveredly helps people find flexible life insurance that fits real life. It's a practical place to explore coverage when you want clarity first, not a complicated sales pitch.