20-pay life insurance lets you pay premiums for exactly 20 years, then keep your coverage for life with no further premiums. That convenience comes at a real cost: premiums are often 50% to 100% higher than standard whole life, and for a healthy 30-year-old male seeking $500,000 of coverage, a 20-pay policy can cost about $450 to $600 per month.

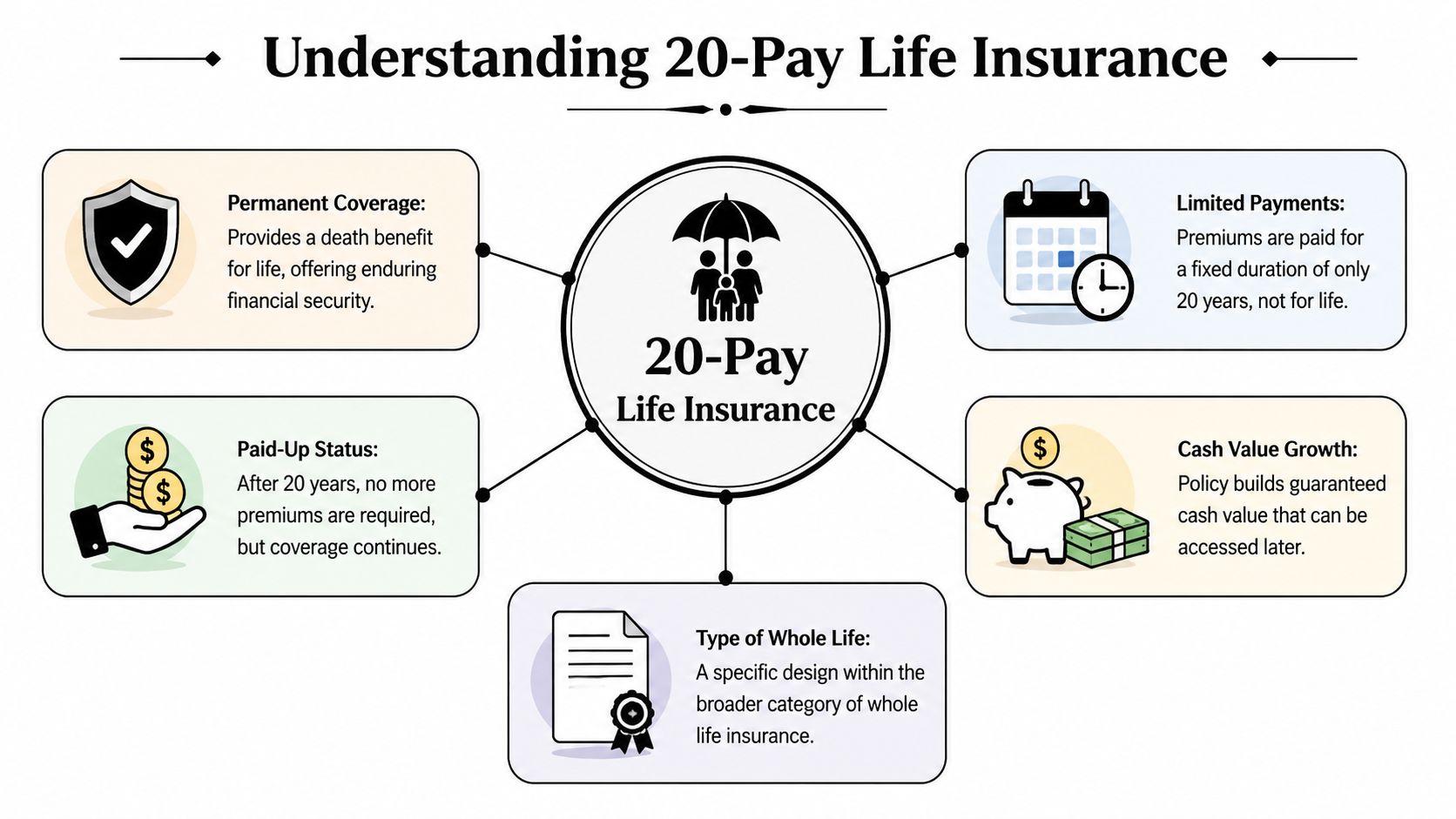

If you're shopping for life insurance right now, you're probably balancing more than one goal at once. You want to protect your family, keep your monthly budget workable, and make choices that won't box you in later. That's where 20 pay life insurance gets interesting. It's a type of whole life policy where you pay premiums for a fixed 20-year period, after which the policy is fully paid for and stays in force for the rest of your life.

For some families, that sounds ideal. You front-load the cost during your working years, then head into retirement without another life insurance bill. For others, the price tag is too high compared with term life. The key is understanding what you're buying, how the cash value works, and what trade-offs you're making.

Table of Contents

- An Introduction to Lifetime Coverage Without Lifetime Premiums

- What Is 20 Pay Life Insurance

- How Premiums and Cash Value Work

- Weighing the Pros and Cons

- Comparing 20 Pay Life Insurance Options

- Who Should Consider 20 Pay Life Insurance

- Smart Buying Tips for 2026

An Introduction to Lifetime Coverage Without Lifetime Premiums

A lot of people don't mind paying for life insurance in their 30s and 40s. That's usually when income is strongest, retirement is still years away, and the need for protection is obvious. The problem comes later, when you still want permanent coverage but don't want another bill following you into your 60s, 70s, or beyond.

That's the appeal of 20 pay life insurance. It offers permanent whole life coverage, but you compress the payments into 20 years instead of stretching them across your entire lifetime. Once the payment period ends, the policy becomes paid-up and stays active.

That changes the planning conversation. Instead of asking only, "Can I afford this premium today?" you also ask, "Do I want to lock in a permanent policy now so I don't have to fund it later?" That's a different mindset from term life, and also different from traditional whole life.

Practical rule: A 20-pay policy makes the most sense when you're intentionally trading a higher current payment for the long-term relief of having no premium in later life.

This product can fit neatly into retirement planning, estate planning, or family protection. But it can also create strain if the premium crowds out other priorities like emergency savings, debt payoff, or retirement investing.

If you want context on broader permanent policy pricing before deciding whether this structure is worth it, it's helpful to review whole life insurance costs and pricing basics.

What Is 20 Pay Life Insurance

The simplest way to understand 20 pay life insurance is to think of it as whole life insurance on an accelerated payment schedule. You still get permanent coverage, a guaranteed death benefit, and cash value growth. What changes is the payment timeline.

The core idea

With standard whole life, you typically keep paying premiums for life. With 20-pay whole life, you pay for exactly 20 years. After that, the policy is fully paid-up, but the coverage continues for life.

A mortgage analogy helps. Traditional whole life is like taking the long payment path. A 20-pay policy is like choosing the shorter loan term. The monthly cost is higher, but you finish sooner and remove the obligation earlier.

That structure is why people often confuse 20 pay life insurance with term insurance. They hear "20 years" and assume the coverage expires. It doesn't. The payments stop after 20 years. The coverage doesn't.

What stays guaranteed

The guarantees matter more than the label. According to MoneyGeek's overview of 20-pay life insurance, feature comparisons show 20-pay has a moderate cost relative to 10-pay whole life, which has steeper payments over a shorter period, and single-premium whole life, which requires the highest upfront cost. The same source notes that for a 35-year-old, 20-pay would finish by age 55, while 10-pay would end by 45 but with much higher premiums.

That same comparison also highlights several core features:

- Level premiums during the payment period so the scheduled premium doesn't rise because you got older or your health changed after issue.

- Guaranteed non-decreasing death benefits in the policy design described.

- Tax-free payouts to beneficiaries under the usual life insurance treatment.

- Dividend potential on participating policies, depending on the insurer and policy design.

A short video can also help if you're more visual than technical.

One more point people often miss: 20 pay life insurance is not a separate universe of insurance. It's a specific whole life design. That matters because you're still evaluating insurer strength, policy illustrations, dividends if applicable, and loan provisions just as you would with other permanent policies.

How Premiums and Cash Value Work

At this point, the product either clicks for a buyer or stops making sense. The higher premium isn't arbitrary. You're funding lifelong coverage in a shorter span, and you're also pushing more money into the policy's cash value earlier.

Why the premium is higher

20-pay premiums are usually much higher than standard whole life because the insurer collects the full funding needed over a limited period rather than over your lifetime. That compressed structure is the reason a policy can later remain in force with no more premiums due.

A concrete example helps. According to Woman's Life on 20-pay whole life mechanics and projections, a healthy 35-year-old male with a $500,000 face amount might pay about $850 per month, for a total of around $204,000 over 20 years.

That number can feel jarring at first. It should. This is not budget-priced coverage. It's a deliberate trade-off: higher premium now in exchange for permanent paid-up coverage later.

How cash value builds

The same source explains why some buyers accept that higher premium. In a 20-pay policy, the cash value growth can accelerate enough to exceed premiums paid by years 15 through 18, and by year 20 the cash value for that same example is typically about $180,000 to $220,000. With a 4% net return assumption in that illustration, it can grow to more than $1 million by age 80.

That doesn't mean every policy performs identically, and it doesn't mean cash value should be treated like a simple investment account. It does mean that larger early premiums can create more substantial policy value sooner than a slower-pay whole life structure.

Think of cash value as a reserve inside the policy, not free money. It can become useful, but it still needs to be managed carefully.

Cash value generally grows on a tax-deferred basis, and many policyholders use loans against that value while the policy remains active. If you want a simple way to think through how policy values may evolve over time, a cash value life insurance calculator can help frame the moving parts before you review a formal illustration.

Where people get into trouble

The flexibility of policy loans is useful, but it's also where misunderstandings cause damage. Loans are typically available without triggering a taxable event while the policy remains in force, but unpaid interest keeps accumulating. If the loan balance and interest grow too large relative to the policy's value, the policy can lapse.

The verified data also notes that unpaid loan interest can compound and offset policy values, and that effective loan rates can be capped at 8% in the described framework from Woman's Life. In plain English, borrowing is easier than repaying, and the policy won't save you from bad math.

Here's the clean way to think about policy loans:

- Borrowing reduces cushion inside the policy.

- Unpaid interest compounds if you don't service the loan.

- A large loan can threaten the policy if it catches up to available cash value.

That's why 20 pay life insurance works best when the buyer wants permanent protection first and views the cash value as a secondary tool, not the main event.

Weighing the Pros and Cons

The right reaction to 20 pay life insurance is usually mixed. There are real strengths here. There are also reasons many families should say no.

Why some buyers love it

The biggest advantage is simple. You can finish paying for permanent life insurance while you're still in your main earning years, then carry that protection into later life without ongoing premiums.

That can be emotionally valuable as much as financially valuable. Some people like knowing the policy is done. No renewals, no premium due in retirement, no worry about keeping up the payment in old age.

Other positives include:

- Permanent protection: Coverage doesn't expire after a set term if the policy stays in force.

- Built-in discipline: The structure forces consistent funding over 20 years.

- Cash value access: The policy can create a reserve you may be able to borrow against later.

For buyers who know they want lifelong insurance anyway, a paid-up policy can feel like removing one more future obligation from the household budget.

Why others should pass

The main drawback is cost. For a healthy 30-year-old male seeking $500,000 of coverage, a 20-pay whole life policy can cost about $450 to $600 per month, while a 20-year term life policy for the same amount is often around $25 to $40 per month, according to Western & Southern's comparison of 20-pay and term pricing. The same source states the total outlay is about $108,000 over 20 years for the 20-pay policy versus about $6,000 for the term policy.

That gap changes the conversation fast.

For a young family with a mortgage, daycare, and retirement contributions to juggle, term life may provide far more protection per dollar. The risk with 20 pay life insurance isn't just that it's expensive. It's that a family can become underinsured because they bought a costly permanent policy instead of a larger affordable term policy.

A practical way to judge the trade-off:

- If the premium feels comfortably manageable and permanent coverage is a firm goal, 20-pay may deserve a closer look.

- If the premium would squeeze savings or force you to reduce coverage, term life is often the cleaner answer.

- If you're attracted mostly by the cash value, slow down and compare that use of money against your other priorities.

Comparing 20 Pay Life Insurance Options

20 pay life insurance is rarely chosen in a vacuum. Policyholders are comparing it to term life, standard whole life, and sometimes other limited-pay versions like 10-pay. The best choice depends on what job you need the policy to do.

A side-by-side comparison

| Feature | 20-Pay Whole Life | Term Life | Traditional Whole Life |

|---|---|---|---|

| Coverage length | Permanent | Temporary for the chosen term | Permanent |

| Premium payment period | Exactly 20 years | For the selected term period | Typically for life |

| Monthly cost | Higher than term and often higher than standard whole life | Usually lowest | Lower than 20-pay, higher than term |

| Cash value | Yes | No | Yes |

| Paid-up point | Yes, after 20 years | Not typically structured this way | Usually not after 20 years |

| Best use case | Buyers who want permanent coverage without lifetime premiums | Families needing affordable income protection | Buyers who want permanent coverage with lower ongoing premiums |

This table shows why 20-pay sits in the middle of two very different planning styles. Term life is built for maximum coverage efficiency. Traditional whole life is built for permanent protection with slower funding pressure. 20-pay is built for permanent protection with a shorter payment window.

How to choose between them

A quick decision lens helps.

Choose term life when your need is mostly temporary. That usually means replacing income while kids are young, covering a mortgage, or protecting a spouse during your working years. The focus here is affordability and higher death benefit per premium dollar.

Choose traditional whole life when you want permanent insurance but don't want to commit to the heavier payment load of a 20-pay structure. You keep the permanence, but you spread the cost over a longer period.

Choose 20 pay life insurance when all three of these are true:

- You want permanent coverage

- You can comfortably afford the higher premium

- You value being done with payments after 20 years

The confusion usually comes from buyers trying to make one product solve every problem. It won't. Term life is usually better for temporary family protection. 20-pay can be better for someone who wants a lifetime death benefit and likes the idea of completing the funding during peak earnings.

If you're newly married or building a family, the right choice often comes down to whether the household needs more coverage now or permanent coverage forever.

Who Should Consider 20 Pay Life Insurance

A product this specific tends to fit certain profiles well and others badly. The easiest way to evaluate it is to picture real households.

A strong fit

Mark and Sarah are a useful example. According to Choice Mutual's explanation of 20-pay whole life, they are parents in their early 30s who chose a $500,000 20-pay policy. Their premiums are higher now, but they expect to be done paying by their 50s while building cash value they may use later for retirement income or policy loans.

That profile makes sense because the decision matches their goals. They aren't just buying the cheapest death benefit. They're buying a long-term structure they want to own outright by midlife.

Other people who may find 20 pay life insurance worth considering include:

- High-earning professionals who want permanent coverage but prefer to finish paying during their working years.

- Estate-focused planners who want a lifelong death benefit and like the predictability of a finite payment period.

- Business owners who value fixed commitments and permanent protection in broader planning.

A weak fit

This product is usually a poor fit when the premium itself becomes the problem.

A young family with a tight budget may need a larger safety net than 20-pay can reasonably provide. If the household can afford only a modest permanent policy but really needs a much larger death benefit for income replacement, term life often does the job better.

The age-based cost examples also show how much pricing matters. Choice Mutual notes that for a 55-year-old female seeking $100,000 of coverage, a 20-pay whole life policy costs about $321 per month, compared with $219 per month for a standard whole life policy in that example. That's a useful reminder that the shorter payment schedule isn't free. You're paying for convenience and acceleration.

Buy 20-pay because you want permanent coverage with a fixed 20-year funding plan. Don't buy it just because the words "cash value" sound attractive.

If that distinction isn't clear, the policy can disappoint you later.

Smart Buying Tips for 2026

If you're seriously considering 20 pay life insurance, shopping carefully matters more than ever. These policies are more complex than term life, and the way they're presented can vary a lot from one insurer or advisor to another.

Questions to ask before you apply

Start with the illustration, not the sales pitch. Ask for a clear explanation of what is guaranteed, what is projected, and how policy loans would affect performance over time.

A smart buyer also asks:

- What is guaranteed in the base policy? Focus on premium schedule, death benefit structure, and paid-up timing.

- How do loans work? You want to know how interest is charged and what happens if the balance grows too large.

- Is this a participating policy? If so, ask how dividends are treated in the illustration.

- What happens if I miss a payment during the 20-year funding period? Payment flexibility matters more than people expect.

Why shopping carefully matters more now

As of early 2026, only about 20% of insurance carriers offer 20-pay policies through a fully digital process, compared with over 80% for term life, according to this 2026 discussion of digital availability and NAIC-related illustration changes. That matters because many buyers are used to getting instant online quotes and quick approvals on term coverage, but permanent policies often still require more advisor involvement and more careful review.

That same source notes recent NAIC updates on cash value crediting rules may impact policy illustrations, which is one more reason not to treat any projection like a promise.

If you want a practical framework before you compare offers, this guide on how to choose the right life insurance policy is a good place to pressure-test your priorities.

20 pay life insurance can be a strong tool. But it only works well when the policy fits your budget, your timeline, and your actual reason for buying life insurance in the first place.

If you're weighing 20 pay life insurance against a more flexible option, Coveredly is worth a look. Coveredly offers online life insurance built for real life, including up to $3 million of term life insurance with no exams for most applicants, so you can compare permanent-policy ideas against a simpler, more affordable protection strategy.