The often-quoted average cost for life insurance in the U.S. is about $26 per month, or roughly $312 per year, but that number hides how much prices vary by age, policy type, and coverage amount. In many real-world cases, especially for young and healthy buyers shopping for term coverage, life insurance costs far less than people expect.

A lot of people put off buying coverage because they assume it will be expensive, complicated, or both. That assumption makes sense. Insurance pricing feels opaque, and “average” numbers rarely tell you what you'd pay.

The surprising part is that many shoppers are not just a little off. They're wildly off. Once you see how rates are built, the topic gets much less intimidating, especially if you're comparing term life, whole life, and no-exam options side by side.

Table of Contents

- The Real Cost of Life Insurance Is Less Than You Think

- What Actually Determines Your Life Insurance Rate

- Average Term Life Insurance Costs by Age and Coverage

- Term Versus Whole Life Insurance and How Costs Differ

- Actionable Tips to Lower Your Life Insurance Premium

- Find Your Affordable Rate in Minutes

The Real Cost of Life Insurance Is Less Than You Think

If you had to guess what life insurance costs, you'd probably land too high. Many people do.

LIMRA's 2025 Insurance Barometer Study found that respondents guessed a $250,000 level-term policy for a 31 to 35-year-old male in good health would cost about $1,486, which was more than 7 times the actual cost, according to Protective's summary of the study. That gap explains why so many families delay a decision they could probably fit into the budget.

The phrase average cost for life insurance also creates confusion because it can mean two very different things. Some people mean the average monthly premium. Others are really thinking about how much coverage people buy, what kind of policy they choose, or whether they're looking at term versus whole life.

Practical rule: Don't ask only, “What's the average?” Ask, “What would someone my age, with my health, buying my type of policy, likely pay?”

That question gets you closer to reality.

For many households, term life is the most useful reference point because it's built for income replacement and debt protection during your working years. A newly married couple, a parent with young children, or a business professional with a mortgage often doesn't need a permanent policy first. They need an affordable safety net.

Averages can still help as a starting point. They just shouldn't be the finish line. The job is to separate broad benchmarks from the price you'd see based on your own age, health, and policy choice.

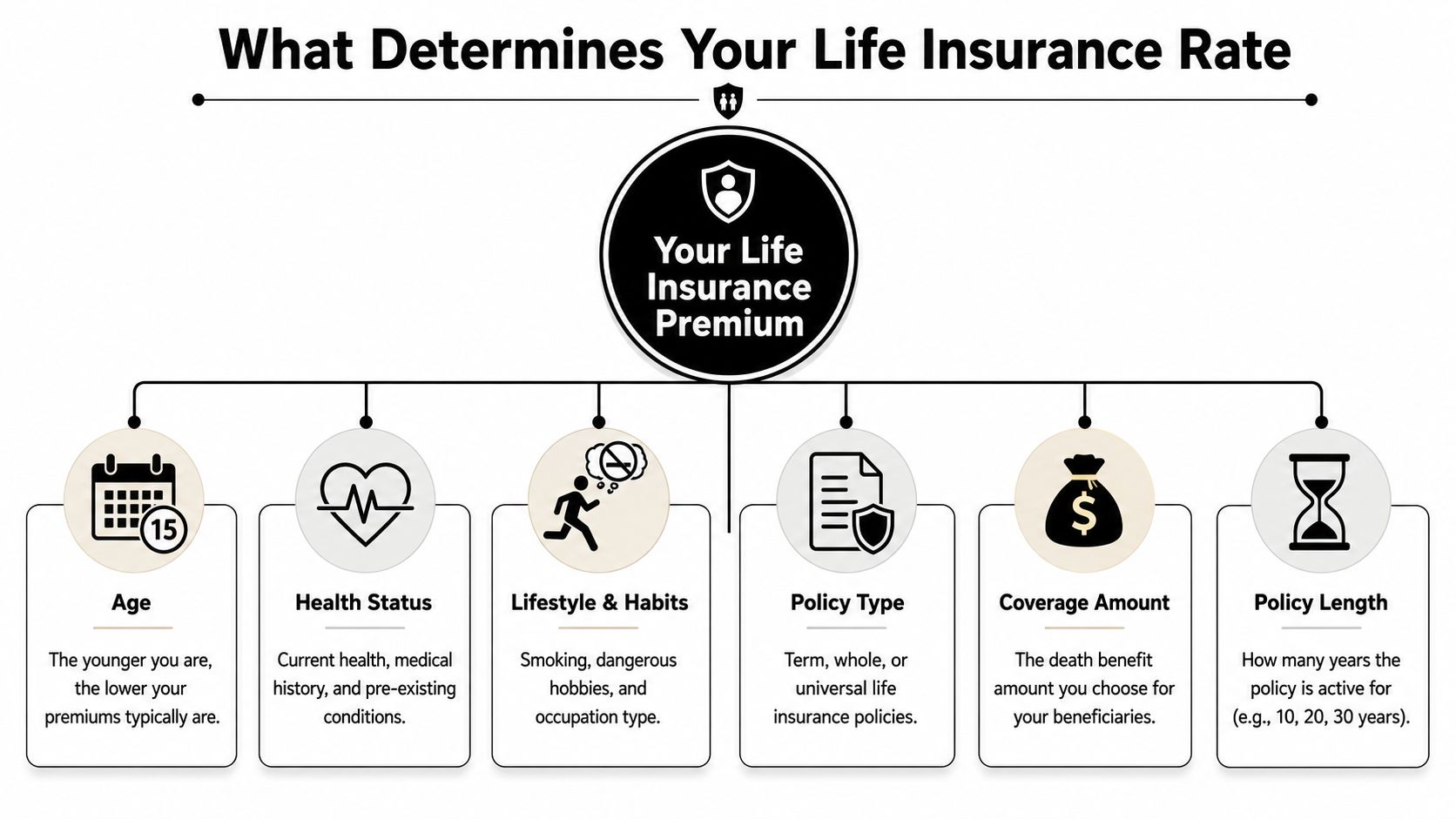

What Actually Determines Your Life Insurance Rate

A life insurance quote can feel mysterious at first, but the price usually comes down to a handful of very ordinary details. Insurers are asking a practical question: how likely is it that they will need to pay the benefit during the policy period, and how large would that benefit be?

Once you know the main pricing factors, the quote starts to feel a lot less random.

Age changes the math fast

Age is one of the biggest drivers of cost because it affects risk over time. Buying younger usually means lower rates, especially for term coverage, since the insurer expects fewer health complications during the policy period.

Baldwin's market overview gives a useful example at Baldwin's life insurance cost guide. It shows how a healthy 30-year-old non-smoker can often pay far less for a 20-year term policy than someone applying at 50 or 65 for the same coverage amount.

That gap matters. Many people delay coverage because they assume life insurance will already be expensive, when age often makes waiting costlier than expected.

Health and habits shape your underwriting class

Your health profile is another major piece of the quote. Insurers often review medical history, prescriptions, height and weight, tobacco use, and sometimes high-risk hobbies or job duties. These details help place you into an underwriting class, and that class has a direct effect on your monthly premium.

If the term "underwriting class" sounds technical, it helps to picture it like a pricing tier based on risk. Stronger overall health usually leads to better rates. Tobacco use, unmanaged medical conditions, or a history of serious illness can push prices higher.

If you want a plain-English explanation of that process, Coveredly's guide to underwriting life insurance walks through how insurers review applicants.

No-exam term life fits into this same basic framework. The insurer still evaluates risk, just with a different process and data sources instead of a medical exam. For many healthy applicants, that can mean getting coverage faster than they expected, without the long, complicated process they may have been bracing for.

Policy choices affect the price more than many buyers expect

Your rate is not based only on you. It is also based on what you are buying.

Three policy choices usually matter most:

- Policy type: Term life usually costs less than whole life because it covers a set number of years, not your entire lifetime.

- Term length: A 30-year term often costs more than a 10-year or 20-year term because the insurer covers a longer period.

- Coverage amount: A larger death benefit raises the premium, but often in a more manageable way than buyers expect.

A simple way to think about it is shopping for a car insurance policy with different coverage limits and deductibles. The driver matters, but the policy design matters too. In life insurance, a healthy applicant choosing a modest term length and a practical coverage amount can often find pricing that feels far more affordable than the average person expects.

That is one reason no-exam term life gets attention. If your goal is a straightforward safety net for income replacement, childcare costs, or a mortgage, a simple term policy may land much closer to your monthly budget than you assumed.

Average Term Life Insurance Costs by Age and Coverage

This is the part most readers want. What might term life look like in dollars?

A widely useful benchmark comes from Progressive's consumer guide, which says a 20-year, $250,000 term policy for a healthy 30-year-old costs under $200 per year on average. The same guide also notes that a 10-year, $250,000 term policy for a healthy 20 to 40-year-old is about $24 to $31 per month, according to Progressive's overview of life insurance pricing.

A useful benchmark for term life

Those two figures tell you something important. Term life is often not just cheaper than expected. It can be surprisingly manageable for people who assume coverage is out of reach.

Here's a simple sample table to help you think about pricing by age and coverage. Because the verified data set does not provide exact rates for every age, gender, and coverage combination, the table uses qualitative guidance rather than invented numbers.

| Age | Gender | $250,000 Coverage | $500,000 Coverage | $1,000,000 Coverage |

|---|---|---|---|---|

| 30 | Male | Often very affordable for healthy applicants | Can still be budget-friendly in term coverage | Usually higher, but may still be within reach depending on health |

| 30 | Female | Often very affordable for healthy applicants | Often competitive for healthy applicants | Higher than lower face amounts, but still worth quoting |

| 40 | Male | Commonly higher than age 30 | Moderate increase versus younger buyers | Meaningful jump, especially with longer terms |

| 40 | Female | Commonly higher than age 30 | Moderate increase versus younger buyers | Higher, but health class still matters a lot |

| 50 | Male | Noticeably higher than at younger ages | Can move into a more serious monthly budget item | Often expensive enough to require careful planning |

| 50 | Female | Noticeably higher than at younger ages | Often somewhat lower than comparable male pricing | Larger face amounts deserve side-by-side quote comparisons |

That's not as tidy as a rate card, but it's more honest than making up precision that doesn't exist in the source material.

Why the sample table is directional

The pattern is clear even without a fully numeric matrix.

- Younger buyers usually pay less. Age is one of the fastest-moving cost drivers.

- Bigger policies cost more, but not always in a linear-feeling way. A jump in face amount may be more affordable than you expect if your health profile is strong.

- Health class can outweigh assumptions. Two people of the same age may see very different offers.

If you want a broader age-based view before applying, Coveredly's life insurance rates by age guide can help you compare how timing affects affordability.

The smartest way to use average cost figures is as a filter, not a quote. They tell you whether coverage is generally affordable. They don't tell you your exact premium.

That distinction matters. It keeps you from walking away too early because a generic “average” sounded high, or getting overconfident because a best-case example sounded low.

Term Versus Whole Life Insurance and How Costs Differ

Why do so many people assume life insurance is expensive? A big reason is that term life and whole life get discussed as if they were close substitutes, even though they are built for different jobs and priced very differently.

Term life works like paying for protection during the years your family would feel the biggest financial hit if your income disappeared. Whole life is permanent coverage that also includes a cash value component, which makes it a more complex and much more expensive product.

That distinction matters more than many shoppers realize. If someone looks at whole life prices first, they can easily walk away thinking all life insurance is out of reach. In reality, basic term coverage, especially no-exam term options, is often far more affordable than people expect.

Term life is usually the budget-friendly choice

Term is popular for a simple reason. It gives you a death benefit for a set period, such as 10, 20, or 30 years, without asking you to pay for lifelong coverage features you may not need.

For a lot of households, that lines up with real life. You may want coverage until the mortgage is smaller, the kids are grown, or your retirement savings are in better shape. In that case, paying for permanent insurance can feel a bit like buying a house when what you needed was a reliable rental for a specific season.

No-exam term life can make that path even easier. If your goal is straightforward protection at a manageable monthly cost, this type of policy is often where the affordability gap becomes clear.

Whole life costs more because it does more

Whole life can make sense in some situations, but the price is usually much higher because the policy is designed to stay in force for life and build cash value over time.

That does not make it bad. It means you should compare it carefully.

Here is the practical difference:

- Term life is usually the better fit if your priority is the most coverage for the lowest cost.

- Whole life may fit people who want permanent coverage and are comfortable paying much higher premiums.

- Comparing term and whole life by price alone can be misleading because you are not buying the same type of product.

A lot of confusion starts here. Someone sees a whole life quote, assumes that is the normal price of life insurance, and decides to wait. Then they never see the term options that could have fit their budget all along.

If you want a clearer side-by-side explanation, Coveredly's guide to term vs. whole life insurance breaks down the tradeoffs in plain language.

For many readers, this is the decision that changes the conversation from "life insurance costs too much" to "I was looking at the wrong kind of policy."

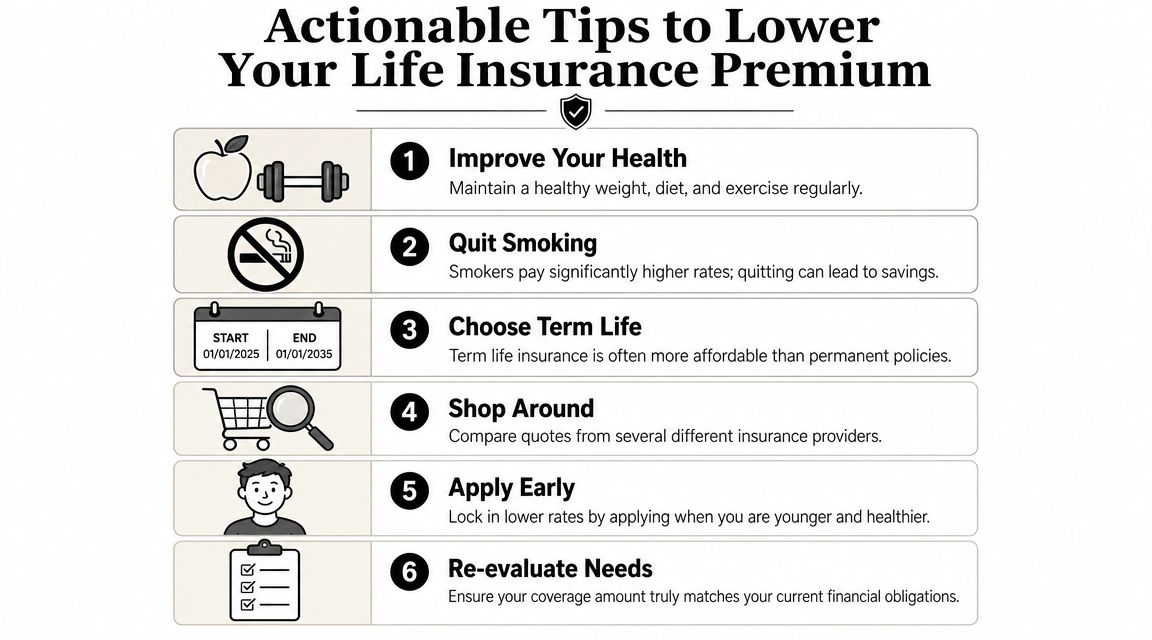

Actionable Tips to Lower Your Life Insurance Premium

Individuals often have more control over pricing than they realize. You can't change your age today, but you can make several choices that shape what you'll pay.

A good starting point is to focus on fit, not just on getting “the cheapest policy.” A lower premium only helps if the coverage still matches your family's real needs.

Changes you can control

- Apply while you're younger and healthier. Waiting usually means a higher premium, especially if your health changes.

- Choose term if budget is the priority. For many households, term gives the most protection per dollar.

- Be realistic about coverage amount. Enough matters more than excess. A policy should support the people who depend on you without stretching your budget.

- Compare policy designs, not just monthly price. A cheaper premium with the wrong term length can be a poor fit.

- Work on insurable habits. Tobacco use, unmanaged health issues, and inconsistent medical follow-up can all affect pricing.

A good quote is one you can keep. Affordable coverage that stays in force beats ideal coverage you never buy.

If you prefer to learn visually before shopping, this short video gives a simple overview of life insurance basics.

When no-exam life insurance makes sense

No-exam life insurance appeals to people who want a faster application and less friction. That can be especially attractive if you're balancing work, family, and a packed schedule.

The tradeoff is worth understanding. Sofi's consumer guidance notes that no-exam life insurance can be quicker but may have higher premiums and lower limits, and it also points out that many consumers still overestimate the cost of a standard policy by more than 2x, which can make comparisons even more confusing, according to Sofi's review of life insurance costs and no-exam options.

That doesn't mean no-exam is a bad deal. It means you should compare it with clear expectations:

- Convenience may justify a modest pricing difference if speed matters to you.

- Limits may be lower than some fully underwritten options.

- The right answer depends on your timeline, health profile, and coverage goal.

People often assume “faster” means “way more expensive.” Sometimes it does not. The only reliable way to know is to compare actual offers rather than relying on old assumptions.

Find Your Affordable Rate in Minutes

The biggest lesson here is simple. The average cost for life insurance is often lower than people think, and broad averages only tell part of the story.

Your real price depends on a handful of understandable factors. Age matters. Health matters. The kind of policy you choose matters a lot. And for many people, term life is the option that keeps meaningful coverage within budget.

You also don't need to understand every insurance term before taking action. You just need enough clarity to avoid the common traps, especially assuming coverage is automatically too expensive or ruling out no-exam options without comparing them.

The best life insurance quote is the real one with your name on it, not the number you guessed before shopping.

If you've been delaying this because the process felt hard or the cost felt unknown, that's exactly why it helps to get an actual quote. A few minutes of comparison can replace a lot of uncertainty.

If you want to see what affordable term coverage can look like for your situation, Coveredly makes it easy to explore life insurance online with a digital, flexible experience. It's a practical next step for anyone who wants to check real pricing, compare options, and find out whether no-exam term life fits their needs.