You've probably looked at life insurance before, then closed the tab when you realized it might mean scheduling a nurse visit, answering a long list of questions, and waiting days or weeks for an answer. That old process still exists, but it's no longer the only path.

Today, many no exam life insurance companies let you apply online, answer health questions, and get a decision much faster. For busy professionals, newly married couples, and parents with a mortgage or a new baby, that speed matters. But speed alone isn't enough. The important question is whether a no-exam policy gives you the amount of protection your family needs.

That's where people get stuck. They know they want convenience, but they don't want to trade away the core purpose of life insurance. This guide is built to help you sort through that trade-off in plain language.

Table of Contents

- Get Life Insurance Faster Than You Can Order a Pizza

- What Is No Exam Life Insurance Really

- The Trade Offs Speed vs Scrutiny

- How Insurers Underwrite Without an Exam

- How to Evaluate No Exam Life Insurance Companies

- A Decision Checklist for Young Families and Professionals

- Common Questions About No Exam Policies

Get Life Insurance Faster Than You Can Order a Pizza

It's 9:30 p.m. The kids are asleep, your inbox is finally quiet, and you remember the life insurance task you have been meaning to finish since the new baby arrived or the mortgage closed. In the past, that usually meant forms, phone calls, a medical exam appointment, and a waiting period that could stretch for weeks.

Now, many no exam life insurance companies offer a much faster path. You answer health and lifestyle questions online, the insurer checks outside records, and you may get a decision the same day. For busy professionals and young parents, that can turn life insurance from a postponed project into something you complete.

Speed is only part of the story, though.

A fast application helps if your main problem is time. It does not help much if the policy amount is too small, the price is higher than expected, or the company's underwriting rules make approval less likely for your health history. A quick quote is useful only if the coverage would still carry the load your family depends on.

That is the question for high-need households. If your income supports rent or a mortgage, child care, college savings, or other shared goals, ask whether no-exam coverage is enough, not just whether it is convenient. The faster route can be a strong fit, but only if it covers the gap you are trying to protect.

A good way to frame it is this: speed gets the policy issued sooner, but protection is what your family would use. If you want a clearer baseline for how this kind of coverage works, this guide to simplified issue life insurance basics can help.

Fast doesn't automatically mean better. The best no-exam policy is the one that matches both your timeline and your protection needs.

Before you apply, keep a few practical questions in mind. How much coverage can this company approve without an exam? Is that enough to replace income, cover debts, and give your family breathing room? If the answer is no, a slower application may still be the smarter choice.

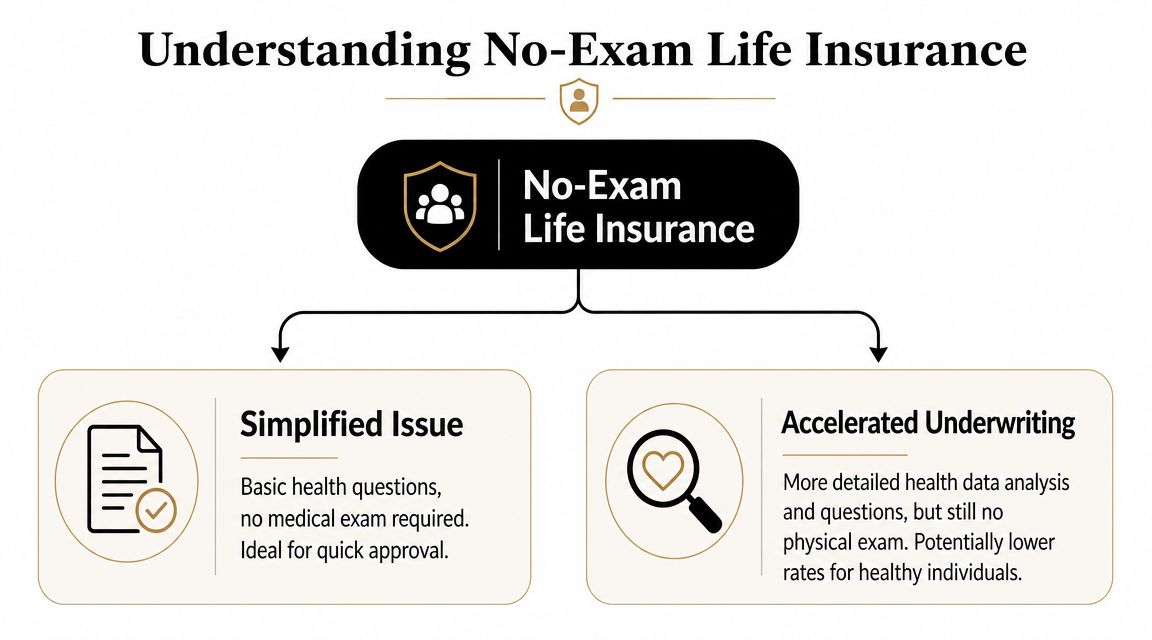

What Is No Exam Life Insurance Really

No-exam life insurance sounds almost too simple, so people often assume there must be a catch. There isn't a trick, but there is a process. The insurer still underwrites you. It just uses different tools.

Two ways no-exam coverage usually works

The easiest way to think about it is this:

- Simplified issue asks you a set of health and lifestyle questions and uses those answers to make a decision.

- Accelerated underwriting also asks questions, but it leans more heavily on digital records and automated checks to verify what you report.

In practice, the line between them can blur in marketing. What matters to you is understanding whether the company is relying mainly on your application answers, on external data, or on both.

If you want a deeper primer on this category, simplified issue life insurance basics can help clarify the terminology.

Why insurers can move faster now

No-exam life insurance is usually simplified issue underwriting. Instead of blood and urine tests, the insurer prices risk from an online health questionnaire plus external data sources such as prescription history, motor vehicle records, and public records. That substitution can move decisions from days or weeks to minutes or same-day in many cases, as described by Mutual of Omaha's explanation of life insurance with no medical exam.

Here's a simple analogy. Traditional underwriting is like a full inspection before buying a house. No-exam underwriting is closer to reviewing the seller disclosure, pulling records, and using digital tools to decide whether the home fits your standards. It's still a real review. It just avoids part of the old manual process.

That distinction helps clear up a common misunderstanding. “No exam” does not mean “no underwriting.” It means the insurer is replacing physical testing with a faster mix of questions and data.

Practical rule: If a policy promises speed, ask what information the insurer still checks behind the scenes. Faster approval doesn't mean less evaluation. It means a different kind of evaluation.

For many applicants, especially those in generally good health, that's a welcome change.

The Trade Offs Speed vs Scrutiny

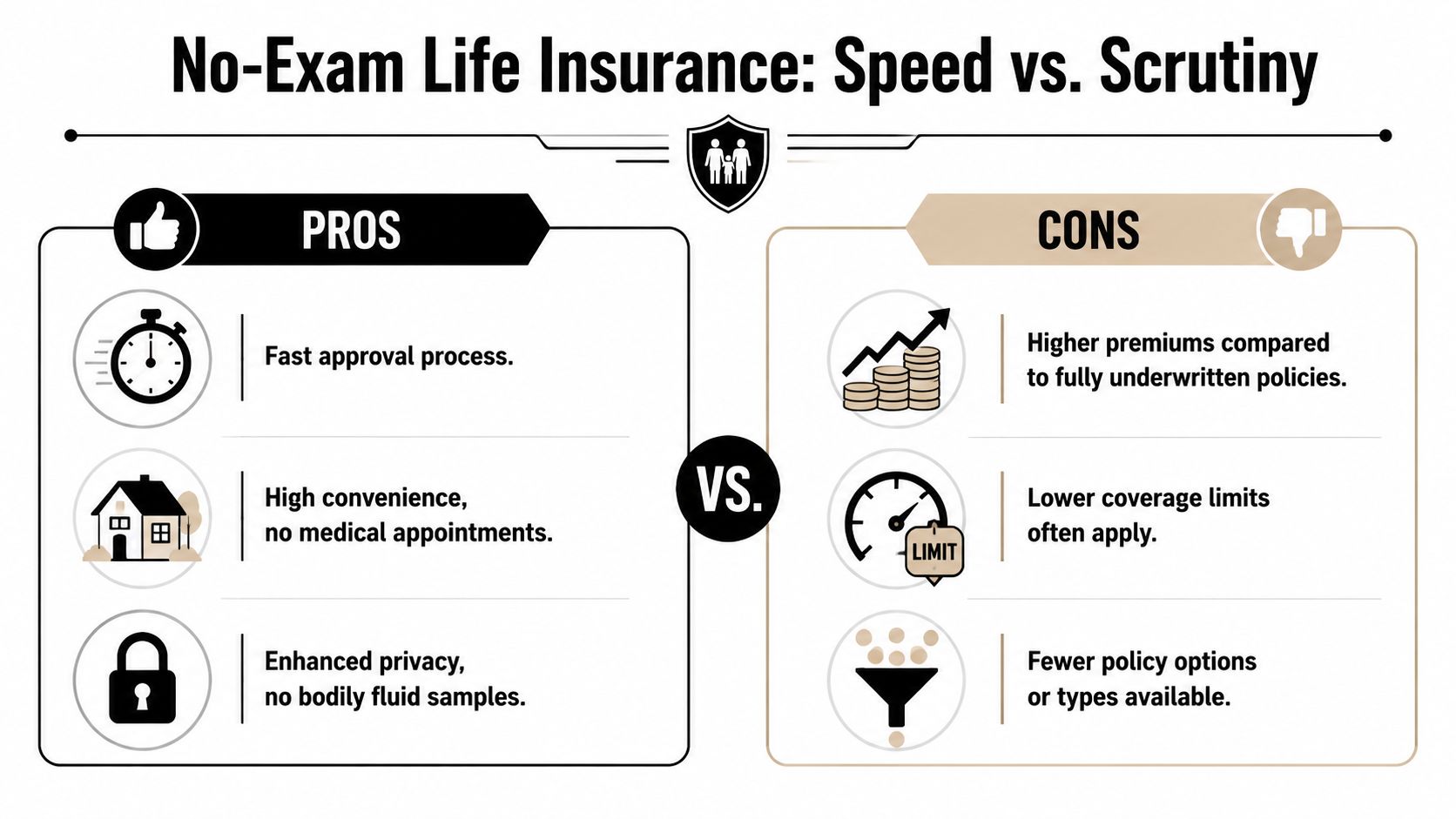

Convenience usually comes with a trade-off. No-exam life insurance is no different.

Why people like no-exam policies

The appeal is straightforward. You skip the nurse appointment, avoid lab work, and often move through the application from your laptop or phone. For people balancing deadlines, daycare pickup, or travel, that ease is a real benefit.

There's also a privacy angle. Some buyers don't want a home exam or don't want to deal with blood draws. No-exam options remove that friction.

And speed can be meaningful, not just convenient. If you've had a major life change, such as getting married, taking on a mortgage, or having a child, getting coverage in force quickly can matter more than optimizing every detail.

Where the compromise shows up

The trade-off usually appears in price, maximum coverage, or both.

Independent consumer guides consistently say no-exam policies usually cost more than fully underwritten policies because insurers accept more risk without the exam. The same guide also notes how limits can vary by age. One major insurer offers no-exam term coverage up to $1 million for ages 18 to 45 and up to $500,000 for ages 46 to 60, according to Western & Southern's overview of no-medical-exam life insurance.

That's where buyers can get tripped up. They compare two policies with the same term length and assume the no-exam option is just a faster version of the traditional one. Sometimes it is close. Sometimes it isn't.

A simple side-by-side view helps:

| Factor | No-exam approach | Fully underwritten approach |

|---|---|---|

| Approval speed | Often faster | Usually slower |

| Medical testing | Usually none | Usually required |

| Pricing | Often higher | Often lower for healthy applicants |

| Coverage ceiling | May be capped | Often broader at higher amounts |

| Convenience | High | Lower |

For many households, the extra cost is worth it if it gets solid protection in place quickly. But if you need the lowest possible premium or the highest possible death benefit, more scrutiny can work in your favor.

Some no exam life insurance companies also reserve their best headline offers for applicants who fit a narrower health profile than the ads suggest. That doesn't mean they're misleading. It means you should treat “up to” language carefully.

Before you choose based on speed, ask three practical questions:

- How much coverage do I need? Don't start with the quote. Start with the family need.

- What happens if I apply and the company offers less than I requested? That outcome is common enough to plan for.

- Would a traditional application save enough money to justify the slower process? For healthy applicants with larger needs, sometimes yes.

How Insurers Underwrite Without an Exam

People often hear “instant decision” and assume the insurer is taking a wild guess. That's not how it works. The company is still trying to assess risk. It's just doing that through digital checks instead of a paramedical appointment.

What you'll usually be asked

Most applications start with a health questionnaire. The exact wording varies, but insurers often ask about recent diagnoses, medications, tobacco use, height and weight, and whether you've had certain major conditions.

After that, many companies compare your answers with outside records. That can include prescription history, motor vehicle records, and public records. Some may also review information tied to prior insurance activity or request additional records if something needs clarification.

If you want a plain-English look at that process, this overview of life insurance underwriting is a useful companion.

Here's the key point. No-exam underwriting is still underwriting. The insurer is not skipping due diligence. It's moving due diligence into databases, application logic, and automated decision models.

Why honesty matters more than people think

Applicants sometimes create problems for themselves. They treat a digital form casually because it feels quick. But the application is still a legal insurance application.

If you understate a health issue, forget a prescription, or answer carelessly, the system may flag the inconsistency. Best case, that can slow your application. In other cases, it can lead to a different offer or a decline.

Accuracy beats speed. Taking a few extra minutes to complete the application carefully can save you a lot of frustration later.

It also helps to prepare before you apply. Have your doctor names, medication details, and basic health history in front of you. That lowers the odds of mistakes and reduces the back-and-forth if the insurer asks follow-up questions.

This is one of the biggest reasons some no exam life insurance companies feel easier than others. The strongest ones don't just ask fewer questions. They ask clearer questions and make it easier to answer them correctly.

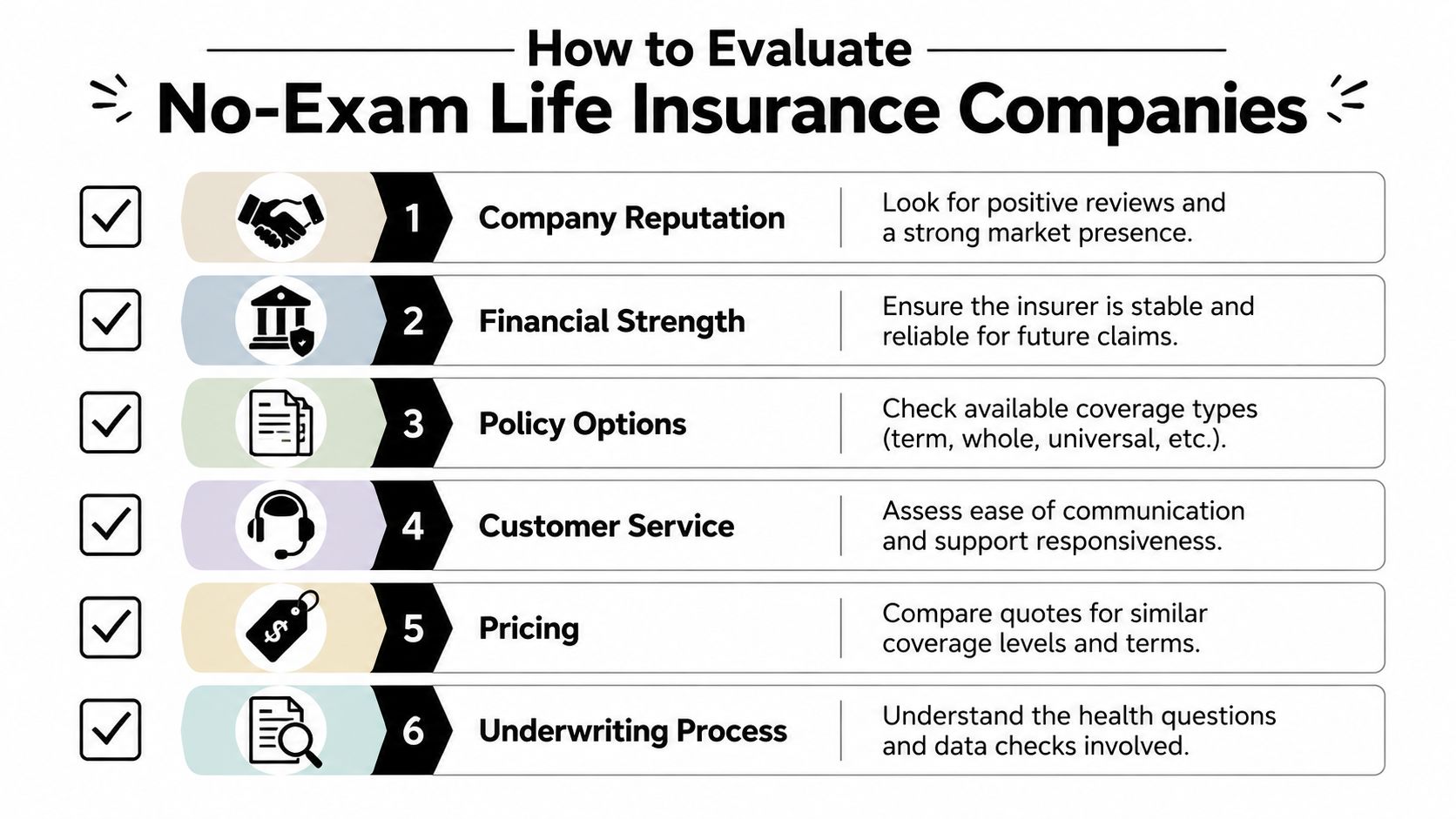

How to Evaluate No Exam Life Insurance Companies

You can get a fast quote in minutes. The better question is whether that quote would effectively protect your household if something happened next year.

Start with the coverage fit

No-exam life insurance covers a wide range of products. One company may offer a smaller policy built for burial costs. Another may offer term coverage large enough to protect a mortgage, replace income, and buy your family time to adjust.

That is why your first filter should be coverage fit, not just price.

A quick way to frame it is this: a no-exam policy is only useful if it can carry the financial weight your family would face without you. For a young professional or parent, that usually means asking practical questions. How much income would need to be replaced? How long would your partner need breathing room? Would the policy cover debts, childcare, or college savings goals?

If you are still working through those priorities, this guide to financial planning for young families can help you sort the insurance decision into the bigger household plan.

Use this framework when comparing providers:

| Criteria | What to Look For | Practical Implication |

|---|---|---|

| Coverage amount | A range that matches your actual need | A low premium does not help if the death benefit leaves a large gap |

| Policy type | Term or permanent options that match your goal | Income replacement and lifelong coverage solve different problems |

| Underwriting style | Clear explanation of questions and data checks | Fewer surprises during review and a better sense of what could delay approval |

| Application experience | Clear forms, understandable questions, and obvious next steps | Busy applicants make fewer mistakes when the process is easy to follow |

| Financial strength | A carrier with a solid reputation for long-term stability | Your family may depend on this company years from now |

| Service quality | Helpful human support when your case is not straightforward | Good technology helps, but real support matters if an issue comes up |

Then compare the company behind the quote

A no-exam policy is still a long-term promise. Speed gets your application through the front door. Company quality determines what happens after that.

Start with the coverage ceiling. If your household needs a larger death benefit, remove companies that are unlikely to approve enough coverage. There is no point comparing polished applications if the final offer would still leave your family underinsured.

Next, look at the details people often skip. Rider options can matter more than a small price difference. An accelerated death benefit, for example, can give a family more flexibility during a serious illness. Waiver of premium can matter if your budget would be strained after a disability.

Transparency is another good signal. Strong no-exam insurers explain what they review, what might trigger follow-up questions, and how long the process usually takes. That does not guarantee approval, but it does help you judge whether the company is built for real planning or just fast marketing.

A few practical checks can save time:

- Check the maximum coverage first. Make sure the company can meet your target before you compare smaller features.

- Read the policy features. Riders, conversion options, and term lengths affect how useful the policy will be later.

- Review how clearly the insurer explains underwriting. Clear expectations reduce frustration if the company asks for more information.

- Pay attention to age and health cutoffs. Some carriers become stricter, or offer less coverage, for older applicants or more complex health profiles.

- Test the support experience. If you have a question now, see how easy it is to get a clear answer before you apply.

A fast quote solves one problem. Enough coverage, from a dependable insurer, solves the right problem.

A Decision Checklist for Young Families and Professionals

If you're in your working years, the biggest question usually isn't whether no-exam coverage exists. It's whether it's enough.

Some carriers now offer $2 million to $3 million without a medical exam, but the practical planning question is whether that meets the common 10 to 12 times annual income rule of thumb for full income replacement, especially for families in their 30s and 40s, as discussed in Policygenius's guide to no-medical-exam life insurance.

That rule of thumb isn't perfect, but it's a helpful starting point. If one spouse earns a strong income and the family depends on it for mortgage payments, childcare, and everyday living, a fast policy with a lower ceiling may only cover part of the need.

For readers thinking through family protection more broadly, financial planning ideas for young families can help place insurance in the bigger picture.

When no-exam coverage is often a strong fit

No-exam coverage tends to make a lot of sense when the household needs protection quickly and the amount available lines up with the actual need.

A strong fit often looks like this:

- You need coverage soon. Maybe you just had a child, refinanced a home, or want to stop putting this task off.

- Your health profile is fairly straightforward. Simpler cases often move more smoothly through digital underwriting.

- Your target coverage falls within available limits. If the amount you need is realistic for no-exam underwriting, convenience can win.

- You value simplicity. For many busy households, a completed policy now is better than a perfect policy that stays on the to-do list.

When a traditional route may still be smarter

Sometimes speed isn't the priority. Adequacy is.

You may want to explore a traditional fully underwritten policy if:

- Your coverage need is very high. This matters for higher earners, families with large debts, or business owners.

- You're exceptionally healthy and price-sensitive. A traditional exam can help some applicants qualify for stronger rates.

- Your situation is more complex. If health history, financial documentation, or planning goals are layered, the broader traditional market may serve you better.

Here's the practical checklist I'd give a client:

- Estimate the need first. Use income replacement, debt payoff, and child-related costs to set a target.

- Compare that target to no-exam limits. Don't assume a company's headline maximum is what you'll qualify for.

- Decide what matters more right now. Fast placement, lower cost, or larger coverage.

- Apply with clear expectations. If the no-exam offer comes back lower than needed, treat it as one option, not the final answer.

For many young families, no exam life insurance companies are a very good solution. Just make sure the policy is solving the fundamental problem, not just the scheduling problem.

Common Questions About No Exam Policies

Can you be denied for no-exam life insurance

Yes. No exam doesn't mean guaranteed approval. If your health answers, prescription history, driving record, or other records raise concerns, an insurer can decline the application or offer a smaller policy than you requested.

Is there a waiting period before the death benefit pays

It depends on the type of policy. Many no-exam term and simplified-issue policies are designed as mainstream coverage, not as guaranteed-issue final-expense products. Some guaranteed-issue policies in the broader market can work differently, so it's important to read the policy details and ask how the death benefit works from day one.

What if the application includes inaccurate information

That can create delays, changes to the offer, or problems later if the insurer finds a material mismatch. Fill out the application slowly and carefully. If you're unsure about a diagnosis date or medication, look it up before submitting.

Are no-exam policies only for small amounts of coverage

No. Some no exam life insurance companies now serve buyers who need meaningful term coverage, not just starter policies or burial coverage. Still, availability depends on age, health profile, and the insurer's rules, so the right question isn't “Do these policies exist?” It's “Will this company offer enough for my situation?”

If you want a digital-first option built for busy families and professionals, Coveredly is worth a look. Coveredly offers online life insurance with up to $3mm of term life insurance and no exams for most, designed to fit real life instead of slowing it down.