The scene is familiar. You're at the kitchen table after bedtime, looking at bank balances, daycare invoices, rent or mortgage payments, and the running list of things your family needs next. A stroller sits in the hallway. Someone still needs to submit the pediatric bill. You both know you need a plan, but every financial task seems connected to five others.

If that feels heavy, it's not because you're doing something wrong. The pressure is real. A 2025 Northwestern Mutual Planning & Progress Study reported that 29% of Gen Z say having children is one of their top affordability concerns, second only to homeownership at 46%, and among those who are already parents, 41% of Gen Z and 42% of Millennials say their monthly child-related spending exceeds their rent or mortgage.

That's why effective financial planning for young families has to be practical. It can't live in a spreadsheet you never open again. It has to help you decide what gets funded first, what gets automated, what gets protected, and what can wait.

The good news is that family finance usually gets better when you simplify it. One clear cash flow system. One safety net. A manageable investing routine. Basic legal documents. A written action plan you can revisit without starting from scratch each time life changes.

Table of Contents

- Map Your Money with a Family Cash Flow Plan

- Build Your Financial Safety Net

- Invest for Your Family's Future Goals

- Secure Your Legacy with Basic Estate Planning

- Your Financial Action Plan and Timeline

Map Your Money with a Family Cash Flow Plan

Friday night, one child is asking for pizza, the baby monitor is buzzing, and a mortgage payment is due next week. You open the banking app and see money in five places, three bills still pending, and no clear answer to one question. What has to be covered first?

That is where a cash flow plan earns its keep. For young families, budgeting is less about tracking every coffee and more about giving each dollar a job before real life gets expensive. It also sets up the rest of the plan, including life insurance. If one income disappeared tomorrow, your budget tells you exactly what needs to be replaced to keep the household running, from the mortgage to daycare to future college savings.

Start with one family snapshot

Start with a one-page view of your household finances. Keep it plain and usable.

- Assets. Checking, savings, retirement accounts, HSAs, and home equity if you own.

- Liabilities. Mortgage, student loans, auto loans, credit cards, and any personal loans.

- Monthly cash flow. Income, fixed bills, irregular costs, and transfers to savings or debt payoff.

This snapshot does two things. It shows how much margin your family has each month, and it shows what your income is responsible for carrying. That second point matters more than many couples realize. I often see families buy life insurance before they have mapped their monthly obligations, which makes it harder to choose a useful coverage amount. A better process is to identify the bills and goals your income supports first, then insure that reality.

If you recently merged households, the first issue is usually logistics. Which accounts stay separate, which bills become joint, and who monitors cash flow each month? Couples who want a practical setup can start with this guide on how to combine finances after marriage.

Practical rule: Your budget should show, within a minute, which expenses must be paid even if one paycheck stops.

Use 50 30 20 as a starting point, not a rulebook

The 50/30/20 framework is useful because it gives families a quick first draft. About half of take-home pay goes to needs, part goes to lifestyle spending, and part goes to saving or extra debt payments.

That split is a reference point, not a moral scorecard. A family with two kids in daycare may spend far more than 50% on needs for several years. A family in a high-cost city may have little room in the "wants" category even with strong income. The value is in seeing the trade-offs clearly.

Use categories that reflect family life:

| Category | What belongs there | Common mistake |

|---|---|---|

| Needs | Housing, groceries, childcare, insurance premiums, utilities, minimum debt payments, transportation for work | Treating convenience purchases as fixed bills |

| Wants | Dining out, entertainment, travel, upgrades, hobbies, gifts above your base plan | Ignoring how small recurring purchases add up |

| Savings and debt | Emergency savings, retirement, extra debt payments, education funds, sinking funds for irregular costs | Waiting to save whatever is left at month end |

One adjustment I recommend to parents is to separate "protected spending" inside the needs category. That includes housing, health coverage, core childcare, and insurance that protects income. Framing it this way changes the conversation. Life insurance stops looking like a separate product and starts looking like part of the cash flow plan that keeps the family's base expenses funded if the worst happens.

Make the system easier than relying on willpower

Busy parents do better with defaults than with daily decisions.

Set up a simple system that runs in the background:

- Track from one shared view. Use a budgeting app, spreadsheet, or shared dashboard that both partners can read quickly.

- Hold a 15-minute weekly check-in. Review upcoming bills, recent spending, and one decision that needs attention.

- Automate transfers on payday. Send money to savings, debt payoff, or education accounts before it gets absorbed into general spending.

- Set a purchase threshold. Decide the dollar amount that requires both partners to agree before buying.

- Review income protection once the budget is built. After you know the monthly number your family depends on, you can judge whether existing life insurance would cover the mortgage, daily bills, and future goals for long enough.

The families who stick with a plan usually remove friction. They simplify accounts, cut duplicate subscriptions, and create one clear process for bills and savings.

A cash flow plan should lower stress, not add paperwork. If it is too detailed to maintain during a week of sick kids, travel, and overtime, it needs to be simpler.

Build Your Financial Safety Net

A flat tire on Monday. A child home sick on Wednesday. A surprise bill on Friday. For young families, financial stress rarely arrives one problem at a time, and that is why a safety net has to cover more than “emergencies” in the abstract. It needs to protect cash flow, protect the household from debt spirals, and keep long-term goals alive when life gets expensive fast.

Emergency cash comes first

Emergency savings give a family room to make good decisions under pressure. Without cash on hand, even a temporary setback can force you to rely on credit cards, skip a bill, or pull money from a long-term account at the wrong time.

A practical target is three to six months of expenses. Keep that money separate from checking so it does not get absorbed into groceries, subscriptions, and everyday spending, but still easy to reach when you need it.

If that number feels out of reach, start smaller. I often tell young parents to aim for one month of core expenses first, then keep building. Progress counts. A starter reserve can cover a deductible, a car repair, or a few weeks of higher childcare costs, which is often enough to stop a bad month from turning into high-interest debt.

If you are also paying down expensive debt, use a split approach:

- Keep the basics current. Housing, utilities, insurance premiums, and minimum debt payments come first.

- Build a starter reserve. Set up automatic transfers, even if the amount is modest.

- Attack high-interest debt next. Once the basic cushion is in place, direct extra cash to the highest-rate balances.

That order works in real life because families need both stability and momentum.

Life insurance belongs inside the plan

Life insurance supports the rest of the plan. It protects the income, services, and time your household depends on so the budget does not collapse after a loss.

That shift in perspective matters. Parents often think about life insurance as a product to buy later, after the budget is cleaner or savings are larger. In practice, it belongs much earlier because it protects the very things you are trying to build: the ability to stay in the home, keep up with bills, continue saving for school, and avoid rushed financial decisions during a crisis.

If one parent dies, the surviving family still has to cover housing, groceries, transportation, childcare, and day-to-day living costs. A policy can also create breathing room for counseling, reduced work hours, extra help at home, or a move that happens on your timeline instead of the bank's.

This applies to both earning parents and stay-at-home parents. The value of a stay-at-home parent's unpaid work is significant. Childcare, school coordination, meals, transportation, and household management all cost real money to replace.

For new parents comparing options, this overview of life insurance for new parents can help you evaluate coverage in plain language and connect it to your household budget.

A family can have a solid monthly plan and still be exposed if the plan depends on one or two people whose income or labor is not protected.

When to shop and how to think about coverage

Coverage is usually easier and less expensive to put in place when you are younger and healthier. Review it when your responsibilities grow. Common trigger points include a new baby, a home purchase, a larger mortgage, one parent cutting back work, or a second child who increases childcare and education costs.

Keep the decision process simple:

| Question | Why it matters |

|---|---|

| Who depends on my income or labor? | A paycheck is not the only thing a family would need to replace. |

| What would need to be paid for if I were gone? | Mortgage or rent, childcare, debt, daily living costs, and future goals all draw from the same pool of money. |

| How much flexibility should this policy create? | More coverage can mean more time for a surviving spouse to grieve, adjust work, or avoid selling assets under pressure. |

| How quickly do we need coverage in place? | Some families need a faster application process because time is limited. |

A good starting point is to estimate what your family would need to stay financially steady for several years, then compare that number with any existing coverage through work. Employer coverage helps, but it is often not enough on its own, and it may not follow you if you change jobs.

The right amount depends on your mortgage, debts, children's ages, your partner's earning capacity, and how much support you want available if life changes suddenly. Buying the lowest-cost policy without doing that math usually creates a false sense of security. Buying coverage based on the life you want your family to be able to continue living is a stronger approach.

Invest for Your Family's Future Goals

Protection keeps a setback from wrecking the plan. Investing gives the plan somewhere to go.

Young families often wait to invest because they assume they need a large amount, perfect timing, or market expertise. You don't. You need consistency, the right account type, and a contribution level you can repeat without derailing your household.

Retirement is the base layer

Retirement investing matters even when college is on your mind. Your children may have several ways to fund education later. You won't have loans for retirement living.

For many households, the first accounts to evaluate are:

- 401(k). Often tied to your employer and payroll deductions, which makes consistent investing easier.

- Roth IRA. Useful for long-term retirement savings with different tax treatment than a workplace plan.

- Spousal retirement planning. Important when one parent has reduced income or stepped out of the workforce.

A useful mental model is this. Retirement investing is your family's future income engine. Education savings is a goal bucket. Fund the engine first, then add to the goal bucket as capacity grows.

Here's a short explainer worth watching before you choose priorities:

Education savings needs its own lane

Once retirement contributions are on track, give education savings a separate account so it doesn't compete invisibly with vacations, home projects, or checking account drift.

A 529 plan is the account many families start with because it's designed for education funding. What matters most at the beginning isn't sophistication. It's creating a dedicated lane for the goal and automating contributions into it.

Open the account before you think you're “ready.” Small, steady transfers beat good intentions that never leave checking.

Parents also benefit from being specific about the goal itself. Are you trying to cover all future education costs, or create a meaningful fund that reduces future pressure? Those are different missions, and they lead to different savings habits.

Keep investing simple and repeatable

The best family investment plan is usually boring on purpose. It doesn't demand constant monitoring. It doesn't encourage emotional decisions. It runs in the background while you handle work, childcare, and life.

Try this operating pattern:

- Automate contributions right after payday.

- Use broad, simple investments inside the accounts you choose.

- Increase contributions gradually when income rises or debt payments fall away.

- Review annually, not obsessively.

Families get into trouble when they treat investing like a side hobby instead of a long-term system. If your plan depends on guessing markets correctly, it's too fragile. If it keeps going even during busy seasons, it's probably built well.

Secure Your Legacy with Basic Estate Planning

Young parents often put this off because it feels legal, heavy, and far away. In practice, basic estate planning is one of the kindest things you can do for your family right now.

The documents that matter most

You don't need a complicated estate strategy to make a major improvement. Most young families should start with a short list of core documents:

- A will. This directs how assets should be handled and who should manage your estate.

- Guardianship designations. If you have minor children, this may be the most emotionally important decision in the whole plan.

- Financial power of attorney. This lets someone handle financial matters if you can't.

- Healthcare power of attorney or similar directive. This names who can make medical decisions and communicate your wishes.

Without these documents, your family may face delay, uncertainty, and conflict at exactly the worst time. Basic estate planning gives people clear authority and direction.

A lot of couples get stuck because they think they need to solve every possible scenario. They don't. Start with naming guardians, choosing decision-makers, and documenting your wishes clearly. You can refine the plan later as assets grow or your family situation changes.

Where life insurance and estate planning meet

Life insurance and estate planning do different jobs. Insurance creates liquidity. Estate documents direct people and decisions. Families need both.

If life insurance is there to fund housing, childcare, and long-term goals, estate planning helps make sure the right people can act and the right children are protected. This is also where beneficiary designations need review. The account may bypass the will, so the paperwork has to match your actual intentions.

If you want a plain-English overview of that connection, this article on whether life insurance is part of an estate is a useful starting point.

Estate planning isn't about expecting the worst. It's about removing confusion for the people you love most.

For financial planning for young families, that peace of mind matters as much as any investment return. It tells your family who steps in, how decisions get made, and what you wanted to happen if you couldn't explain it yourself.

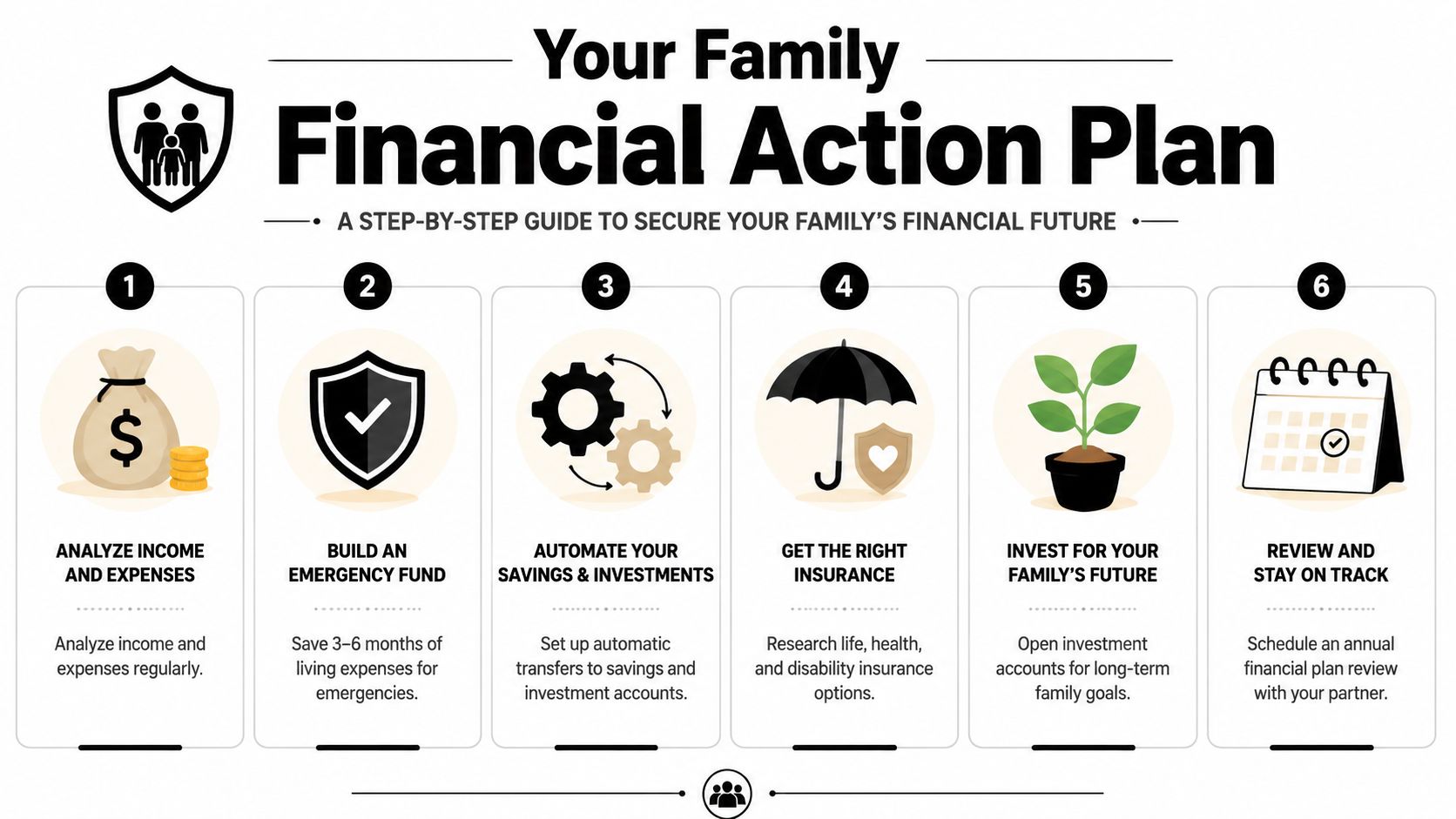

Your Financial Action Plan and Timeline

Most families don't need more advice. They need an order of operations.

A written plan helps because it turns good intentions into visible commitments. According to the 2024 Schwab survey summarized by Annuity.org, 36% of Americans have a written financial plan, and 96% of those people say they feel confident about reaching their financial goals. That's the practical power of writing things down. It reduces ambiguity.

Write it down and make it real

Your plan doesn't need to be polished. One page is enough if it answers these questions:

| Decision | Your answer |

|---|---|

| Monthly essentials | What must be covered first every month |

| Emergency target | Where the cash reserve will live and how you'll fund it |

| Protection | Which insurance policies need review or purchase |

| Long-term goals | Retirement, education, debt freedom, housing, other family priorities |

| Legal basics | Who serves as guardian, agent, executor, or decision-maker |

Write names, account actions, and dates. “Save more” is not a plan. “Transfer money to savings every payday” is a plan.

This month, this quarter, this year

Use a simple timeline so the plan turns into movement.

This month

- List every account and bill. Build your household balance sheet and monthly cash flow view.

- Set category limits. Use your version of the 50/30/20 framework as a starting point.

- Check protection gaps. Review whether your income, debts, and family responsibilities are backed by appropriate life insurance.

- Schedule a money meeting. Put a recurring date on the calendar with your partner.

This quarter

- Open or separate emergency savings. Keep it accessible but out of daily spending flow.

- Automate key transfers. Savings, retirement, and debt payoff should happen without fresh decisions each month.

- Choose one investment priority. Increase retirement contributions or open an education savings account.

- Review beneficiaries. Make sure they reflect your current family structure.

This year

- Create estate documents. Get a will, guardianship designations, and powers of attorney in place.

- Revisit insurance after major life changes. A home purchase, new child, or job shift should trigger a review.

- Adjust the plan after raises or expense changes. Direct new income deliberately instead of letting it disappear.

- Hold an annual review. Treat it like a family planning meeting, not a crisis response.

The strongest plans aren't the most complex. They're the ones your family can keep using when life gets busy.

If you're ready to put protection in place as part of a complete family plan, Coveredly offers online term life insurance designed to fit real life. It's built for young families, newly married couples, and busy professionals who want a faster, more flexible way to secure coverage without turning the process into another full-time project.