You're probably in one of these moments right now. You just got married and combined finances. You bought a house and signed a mortgage that suddenly feels very real. Or you had your first child and realized that “we should get life insurance” moved from vague adult advice to an actual item on your to-do list.

That's where individuals often get stuck. They start comparing whole life and term life insurance, hit a wall of jargon, and end up more confused than when they started. One policy sounds cheap and simple. The other sounds permanent and “smart” because it builds cash value. Both can be useful. They are not interchangeable.

My opinion is straightforward. Most young couples should start with term life. It's built for the years when your income matters most to other people. Whole life has a place, but it's a narrower one, and you should buy it for a specific reason, not because an illustration made it sound appealing.

This guide is built to help you choose, not just compare features. You'll get a plain-English breakdown, a practical cost discussion, and a decision flow based on real life stages like marriage, having a child, and starting a business.

Table of Contents

- Introduction Planning Your Financial Safety Net

- Whole Life vs Term Life The Core Differences Explained

- The Real Cost of Coverage A Detailed Price Comparison

- The Cash Value Component Investment or Expensive Feature

- Choosing at Key Life Stages Scenarios and A Decision Flowchart

- How to Buy Your Policy The Modern Way

- Frequently Asked Questions About Life Insurance Policies

Introduction Planning Your Financial Safety Net

A young couple sits down after dinner to review bills. One income covers most of the mortgage. The other handles childcare costs, groceries, and savings. Then the obvious question shows up. What happens if one of us dies too soon?

That's the core purpose of life insurance. It's not a financial trick. It's not just a tax topic. It's income protection for the people who depend on you.

For most households, the decision starts with two options. Term life insurance is temporary coverage designed for a specific stretch of years. Whole life insurance is permanent coverage that also includes a cash value feature. Those aren't just technical differences. They lead to very different monthly costs, planning choices, and expectations.

Practical rule: Buy life insurance to solve a problem your family would actually face. Don't buy a policy because the product sounds impressive.

If you're early in family life, your biggest risks are usually practical. Replacing income. Paying off debts. Keeping a spouse in the home. Making sure your child's routine doesn't collapse financially after a tragedy. Those are term-life problems more often than whole-life problems.

Still, whole life shouldn't be dismissed out of hand. Some households want lifelong coverage. Some want an additional conservative asset inside a broader financial plan. Some business owners and high earners use it more intentionally than the average family does.

The right choice depends on what job you need the policy to do, how long that job lasts, and how much complexity you're willing to manage.

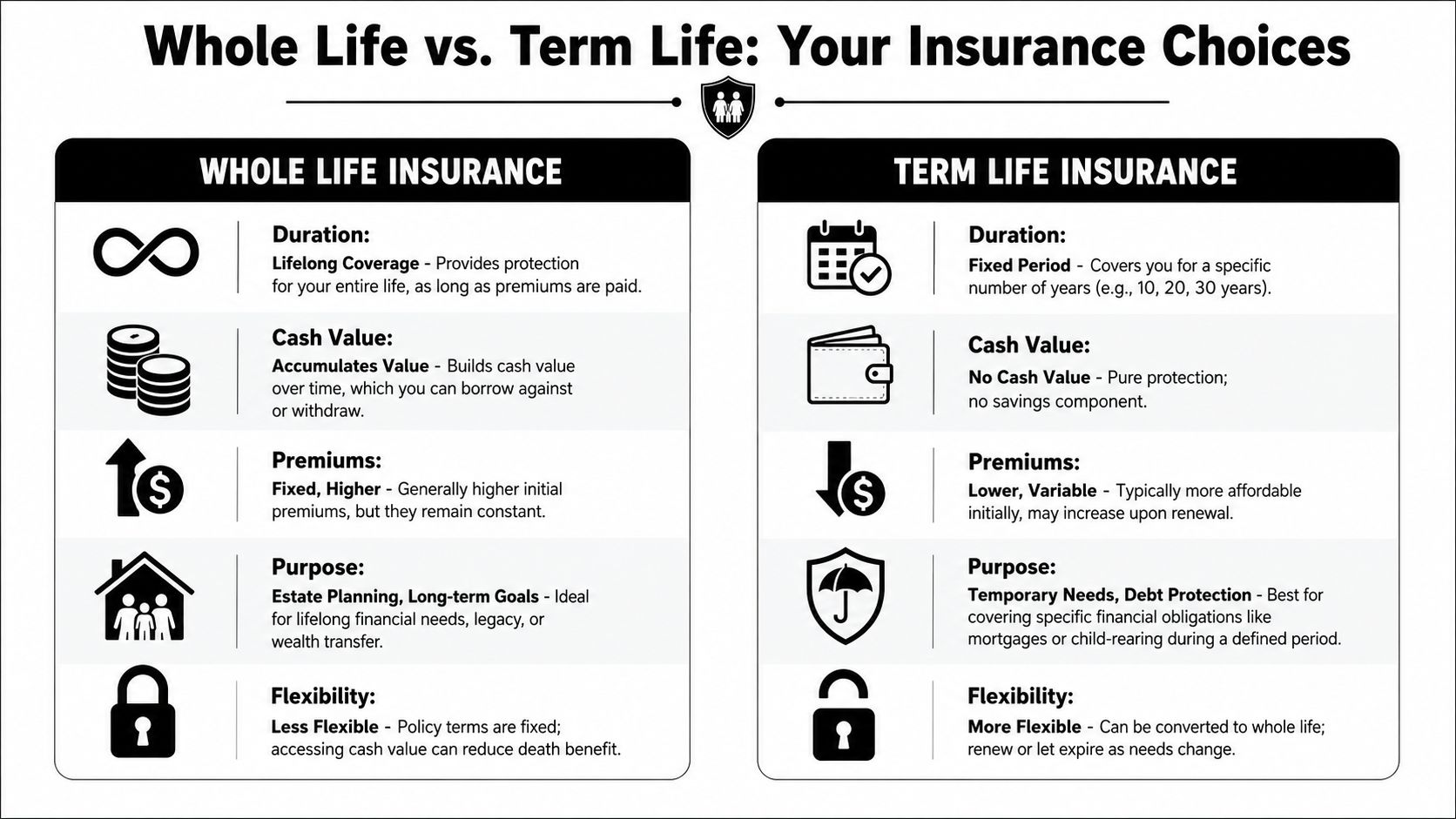

Whole Life vs Term Life The Core Differences Explained

The fastest way to understand whole life and term life insurance is to stop thinking of them as competitors and start thinking of them as tools built for different jobs.

The side-by-side view that actually matters

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Coverage length | Usually a fixed 10-, 20-, or 30-year period | Designed for lifetime coverage if premiums are paid |

| Premiums | Typically lower during the chosen term | Typically fixed and higher |

| Cash value | None | Includes a cash value account |

| Main purpose | Temporary income protection and debt coverage | Lifelong protection plus a cash value feature |

| Complexity | Usually easier to understand and manage | More moving parts, especially if you borrow or withdraw from the policy |

According to Allstate's explanation of whole life insurance, whole life is a permanent form of life insurance that can last your entire life as long as premiums are paid, and it includes a cash value component that grows tax-deferred and can often be borrowed against. By contrast, term life usually lasts a fixed period, commonly 10 to 30 years, and doesn't build cash value. The same explanation notes that a policy with cash value and a guaranteed death benefit costs on average 8 times more than a comparable term policy.

That one fact explains most of the confusion in this market. People compare the two policies as if they should cost about the same. They shouldn't. One is pure insurance for a temporary need. The other is insurance plus a built-in long-term feature set.

A quick visual can help if you prefer to see the distinction in motion.

How these policies behave in real life

Term life is usually the cleaner answer for young families because the risk itself is temporary. Your child won't be financially dependent forever. Your mortgage balance won't last forever. Your highest vulnerability often sits inside a defined window.

Whole life is better matched to permanent goals. That could mean lifelong protection for estate planning, leaving a legacy, or adding a more conservative insurance-based asset to a broader plan. But there's a catch. Whole life is more complex to use well.

Policy loans or withdrawals can reduce the death benefit. That matters more than most buyers realize.

That's one reason I push clients to avoid buying whole life based on a vague promise that it “builds wealth.” If you want whole life, you should know exactly why you want the permanent death benefit and exactly how you expect to use the cash value.

The Real Cost of Coverage A Detailed Price Comparison

Price is where the choice gets real. People can talk about “building value” all day, but the premium has to fit your actual budget.

Why whole life costs so much more

Here's the cleanest concrete example in the verified data. According to Forvis Mazars on whole life vs. term life insurance, for a 40-year-old male seeking a $1 million death benefit, average annual premiums are about $16,500 for whole life versus about $650 for term life.

That gap is not small. It changes your household cash flow.

Whole life costs more because the premium isn't funding just a death benefit during a fixed period. It also supports lifelong coverage and the policy's cash value component. Term life strips the product down to the core job. If you die during the term, the policy pays. If you outlive the term, it ends.

What that trade-off means for a young couple

For a newly married couple or first-time parents, the practical question isn't “Which product has more features?” It's “Which product lets us protect the family without crowding out every other goal?”

In many households, the answer is term life. It leaves room for retirement savings, an emergency fund, childcare, and debt payoff. That's why “buy term and invest the difference” became such a common rule of thumb. It's not perfect advice for every person, but it reflects a valid priority. Protection first. Flexibility second. Complexity later if needed.

If you want a closer look at premium mechanics and what affects the price, this guide on how much whole life insurance costs is a useful next read.

The biggest mistake I see is not choosing the “wrong” type of life insurance. It's buying too little coverage because the premium felt uncomfortable.

If term lets you buy enough protection now, that's often the better move than forcing a whole life premium that strains the rest of your plan.

The Cash Value Component Investment or Expensive Feature

Cash value is the part of whole life that gets sold hardest and understood least.

What cash value is and what it is not

Whole life includes a cash value account, and that feature can matter. But don't confuse “has cash value” with “is a great investment.” According to Guardian Life's term vs. whole life overview, whole life is often marketed like a savings or investment vehicle, but it's better understood as insurance with a cash-value feature, not a pure investment.

That distinction matters because young families often hear the sales pitch before they hear the limitations.

Cash value can usually be accessed through policy loans or withdrawals. But that access isn't free of consequences. If you borrow against the policy or withdraw from it, the death benefit can be reduced. In plain English, using the policy during your life can shrink what your family receives later.

When cash value can make sense

Cash value is most appealing when you already have the basics handled and want another long-horizon asset inside your plan. That usually means you're already funding retirement, carrying manageable debt, and buying whole life intentionally rather than hopefully.

For younger households, ask these questions before you get excited about cash value:

- What problem am I solving? If the goal is protecting income during child-raising years, term usually fits better.

- Can I comfortably afford the premium for years? Whole life is unforgiving when the budget gets tight.

- Do I understand the trade-off? Accessing value through loans or withdrawals can reduce what beneficiaries ultimately receive.

- Am I buying insurance or chasing an investment story? Those are not the same thing.

If you've seen confusing discussions about “cash value term life,” this explainer on cash value and term life insurance differences helps clear up the wording.

My blunt view is this. If you're a young couple still building your emergency fund and retirement savings, whole life's cash value is often an expensive feature rather than an urgent need. That doesn't make it bad. It just means you shouldn't put it ahead of the basics.

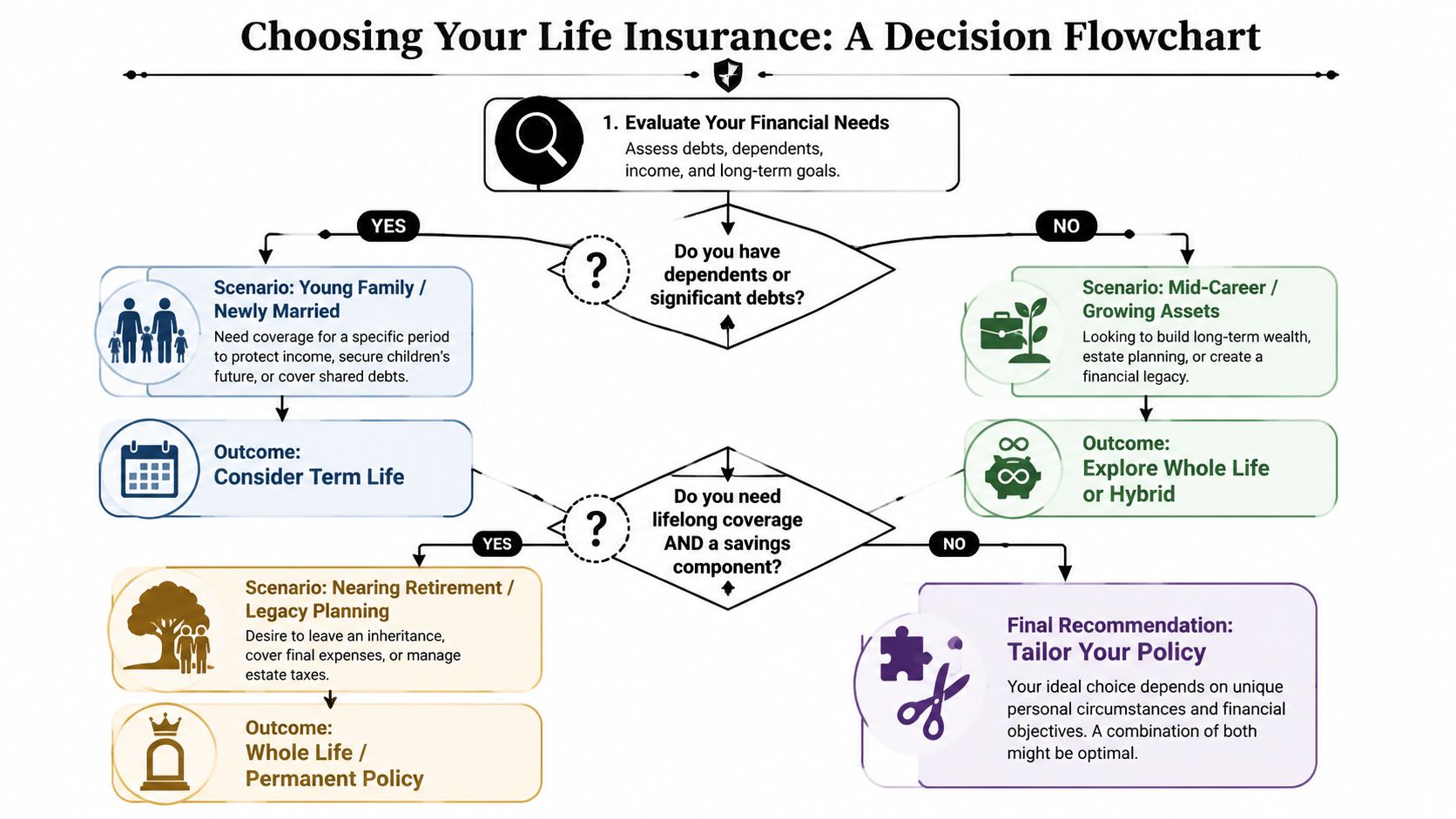

Choosing at Key Life Stages Scenarios and A Decision Flowchart

The decision becomes practical. Your life stage usually points to the right answer faster than product marketing does.

Newly married with shared debts

If you just got married and now share rent, a mortgage, student loans, or a lifestyle built on both incomes, term life is usually the obvious choice.

Why? Because your biggest financial exposure is concentrated in the next stretch of years. One death could leave the other person covering debt payments, housing costs, and daily bills alone. That's exactly what term is built for.

A practical recommendation: choose a term length spanning the years when one income loss would be financially disruptive. Keep it simple and prioritize enough coverage over fancy features.

First child and rising responsibilities

Once you have a child, the case for term life gets even stronger. You're protecting more than a spouse now. You're protecting future time. Childcare. School years. The ability for the surviving parent to keep life stable.

For most parents in this stage, I'd still recommend term life first. You need strong coverage during the years your child depends on you most. That's the core job.

If your main fear is “Could my family keep going without my income?”, term life is usually the right first answer.

Starting a business

Business owners add another layer. You may have personal dependents and business obligations at the same time. A partner might rely on you. A loan might be tied to the company. Your family may depend on irregular income that took years to build.

In that case, term life often still does the heavy lifting because it can cover the years of peak business risk. But a more customized arrangement may make sense, especially if your business planning, estate goals, and personal cash flow are becoming more complex.

If you already own term and want to understand whether changing part of it later could make sense, review the basics of converting term life to whole life.

When whole life belongs in the conversation

Whole life becomes more compelling when your need is permanent, not temporary. That's a very different decision from “I need life insurance because I have a toddler and a mortgage.”

There is one important nuance here. A Financial Planning Association analysis found that for a couple age 40, an integrated strategy using whole life as a volatility buffer produced 63% more lifetime spending and 56% more legacy wealth than a strategy of buying term and investing the difference. The same analysis showed that outcomes varied widely, which tells you exactly how to interpret the finding. Whole life can be powerful inside a broader plan. It is not automatically superior in a vacuum.

So here's my direct recommendation by scenario:

- Newly married with shared debts: Buy term.

- Parents with young children: Buy term.

- Business owner with temporary risk and tight cash flow: Start with term.

- High-income household with strong savings, permanent goals, and interest in legacy planning: Explore whole life carefully.

- Not sure: Default to term, then revisit later if your planning needs become more complex.

How to Buy Your Policy The Modern Way

Buying life insurance shouldn't feel like applying for a secret club. The process is much easier when you start with the job the policy needs to do.

Start with the job the policy needs to do

Think in obligations, not product labels.

Make a short list of what your family would need covered if you died. Focus on things like replacing income, keeping the home, handling debts, and preserving stability for your children. Then choose the policy type that lines up with that time horizon. Temporary problem, term policy. Permanent objective, whole life conversation.

Keep your selection process grounded with a few simple checks:

- Match the term to the need. If your biggest obligations are child-raising years or a mortgage, pick a term that covers that window.

- Protect the household budget. A policy that looks impressive but strains your monthly finances is the wrong policy.

- Use jargon as a warning sign. If an explanation gets slippery around fees, policy loans, or death benefit reductions, slow down.

Keep the buying process simple

The modern buying experience is much better than the old stereotype. Many shoppers can compare options online, answer health questions digitally, and move much faster than they expect.

That's especially helpful for young professionals and parents who don't want a long, drawn-out process. The easier the process is, the more likely you are to finish it. And finished coverage beats perfect intentions every time.

My advice is simple. Don't wait until your schedule clears up, the house is fully organized, or you've read every opinion online. If people depend on your income, get the application moving.

Frequently Asked Questions About Life Insurance Policies

Can you own both term life and whole life

Yes. Some people use term life for large temporary needs and whole life for a separate permanent objective. That can make sense if you know why each policy exists. It's a poor setup if you're mixing products because no one gave you a clear recommendation.

Can you convert term life to whole life later

Sometimes, yes. It depends on the policy. Some term policies include a conversion option that lets you move into permanent coverage later without starting from scratch on insurability. That option can be useful if you want affordable protection now but think your planning needs may change over time.

What riders should young families look at

Don't start with riders. Start with the base policy doing the main job correctly. A rider can be useful, but it shouldn't distract you from the bigger question of whether you bought enough coverage and chose the right policy type.

If you don't understand what a rider does, skip it until someone explains it in plain English.

What's the biggest mistake people make

They delay. Or they overcomplicate the decision and end up uninsured.

The second biggest mistake is buying whole life because it sounded more advanced, when term would have solved the actual problem better. Advanced isn't automatically better. Appropriate is better.

Buy the policy that protects your family now. You can always make your planning more sophisticated later.

If you're ready to stop researching and get covered, Coveredly offers a simple digital way to shop for life insurance that fits real life. For many applicants, that means access to term coverage without the old-school hassle, with a process built for busy families and professionals who want protection without the paperwork marathon.