You're probably here because life insurance moved from “I should get around to that” to “I need to handle this.” Maybe you got married. Maybe you bought a house. Maybe there's a baby on the way, or a business that depends on your income. The trigger is usually the same: someone else would have a financial mess to clean up if you weren't here.

That's why affordable life insurance online matters. Not because it's another financial product to check off, but because the right policy can keep a mortgage paid, replace income, and buy your family time to make decisions without panic. The tricky part is that “affordable” can mean two different things. It can mean the lowest monthly premium on your screen. Or it can mean the best value for the amount of protection your family needs.

Consumers don't need more complexity. They need a simple way to choose coverage, compare online quotes, and understand whether a fast no-exam policy is worth the tradeoff or whether a fully underwritten policy will save more money over time.

Table of Contents

- Why Affordable Life Insurance Is More Than Just a Price Tag

- How Much Life Insurance Do You Really Need

- Choosing the Right Policy Type and Term Length

- Finding and Comparing the Best Online Quotes

- The Truth About No-Exam vs Fully Underwritten Policies

- Smart Strategies to Lower Your Life Insurance Premiums

- Your Next Step to Securing Affordable Coverage

Why Affordable Life Insurance Is More Than Just a Price Tag

The first mistake people make is treating life insurance like a commodity. If two policies show similar monthly prices, it's tempting to click the cheapest one and move on. That works for streaming services. It doesn't work well for protecting a family.

Real affordability means the policy fits your budget and does the job if your income disappears. For most households, that job is specific. Cover the mortgage. Replace income for a few years. Keep childcare and daily bills from turning into debt. Give a spouse or partner breathing room instead of a forced fire drill.

The need is wider than many people realize. Choice Mutual's life insurance statistics estimate that only 52% of Americans have life insurance, while more than 100 million Americans are uninsured or underinsured. The same research says 30% of Americans would face financial hardship within one month of the unexpected death of a wage earner.

Practical rule: If someone relies on your paycheck, life insurance isn't mainly about you. It's about preserving their options.

That changes how you should shop for affordable life insurance online. The goal isn't to win the lowest quote on a results page. The goal is to buy enough protection at a price you can sustain for the full term.

A policy that feels cheap but leaves your family exposed isn't a bargain. It's an unfinished plan.

How Much Life Insurance Do You Really Need

A low premium feels good right up until you ask what the policy would cover. That's the part people skip. They start with the quote instead of the risk.

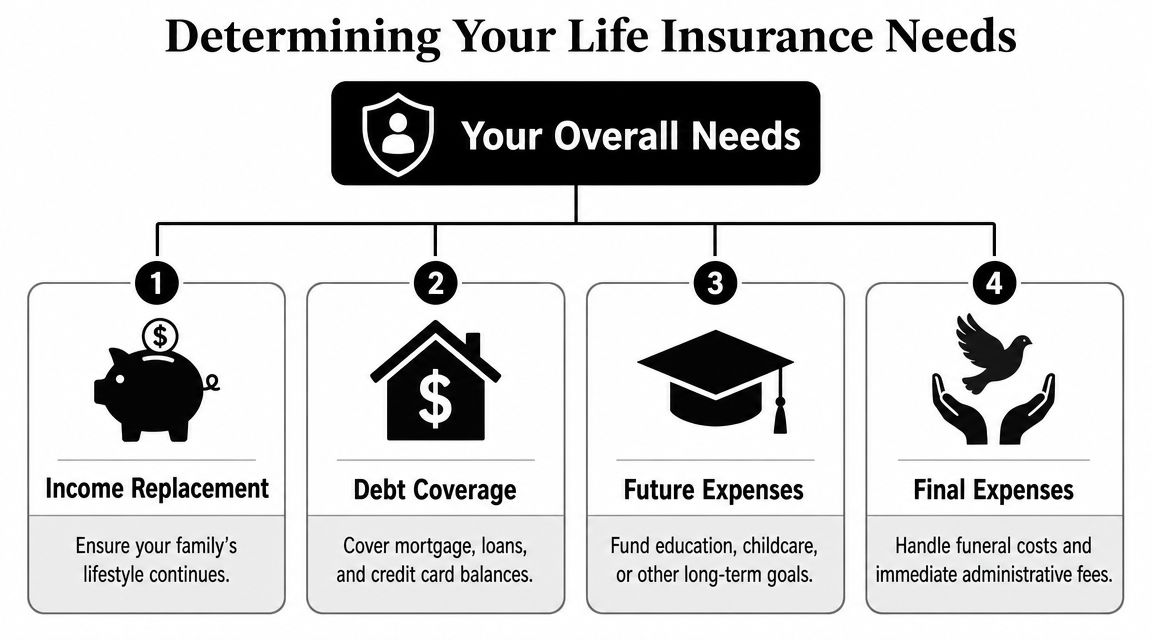

A useful coverage target doesn't require a complicated calculator. Start with what would still need to be paid if you weren't around, then work backward into a coverage amount that makes sense.

Start with obligations, not premiums

Many buyers anchor on the monthly number first. That's how people end up underinsured. Neutral guidance notes that people need to compare policy size, term length, and future obligations, and that a policy that looks affordable at $250,000 may still fall short for childcare, housing, and income replacement over 10-20 years in many families, as discussed by the University of Maryland Alumni Insurance Program.

Think in practical categories:

- Income replacement: How long would your family need your income replaced to stay stable?

- Debt payoff: Would you want credit cards, personal loans, or business debt cleared?

- Mortgage protection: Should your partner be able to stay in the home?

- Future costs: Childcare, education, or a period of reduced work for the surviving parent can change the number fast.

Use a simple DIME-style checklist

You don't need to be rigid about formulas, but a DIME-style approach is a solid starting point:

| Category | What to include |

|---|---|

| Debt | Personal loans, credit cards, business obligations you'd want covered |

| Income | The amount of income your household would need replaced for a meaningful period |

| Mortgage | Remaining home loan or rent support if staying in the home matters |

| Education | Childcare, school costs, or future education support |

Two examples make this more concrete.

A professional couple with a new baby might want enough coverage to eliminate major debts, cover the mortgage, and replace income during the years when childcare is expensive and savings are still growing. In that case, the cheapest policy on the screen may not be enough even if the premium looks attractive.

A small business owner may need coverage that protects both family and operations. If a spouse depends on business income, a minimal policy can leave both the household and the company under pressure at the same time.

Buy the amount that solves the problem, then shop hard for the best price on that amount.

That's the right sequence. If you reverse it, affordable life insurance online can look cheaper than it really is because you're comparing premiums on coverage that may not protect the people you care about.

Choosing the Right Policy Type and Term Length

Once you know the coverage amount, the next decision matters even more than most buyers think. You need the right type of life insurance and the right term. Get this wrong and the premium can jump from manageable to unnecessary.

Why term usually wins on affordability

For buyers focused on affordable life insurance online, term life insurance is usually the first place to look. It's built for a defined period when your financial responsibilities are highest, such as raising kids, paying a mortgage, or building a business.

The cost gap between term and whole life is dramatic. NerdWallet's comparison of life insurance types cites an average of $26 per month for a healthy 40-year-old buying a 20-year, $500,000 term policy. For the same coverage in whole life, the averages are $5,524 per year for men and $4,967 per year for women.

That doesn't make whole life bad. It makes it a different tool. Whole life is permanent coverage with a different pricing structure. If your main goal is protecting your family during peak earning and spending years, term is usually the cleaner fit.

Term life is protection first. If affordability is the priority, that's often exactly what you want.

How to pick the term length that fits your life

Choosing the term isn't about guessing. Match it to the period when your household is financially exposed.

Here's a practical way to consider this:

- Shorter term: Better for temporary obligations that should decline sooner, like a smaller debt load or a later-in-life purchase.

- Mid-range term: Often a strong fit for families with young children, especially if the goal is to protect the years before kids become more independent.

- Longer term: Makes sense when you're covering a long mortgage runway, young dependents, or a household that would need more time to absorb the loss of income.

A simple test helps. Ask, “When would the people who depend on me be financially strong enough that this policy matters much less?” That answer usually points you toward the right term length faster than any sales pitch will.

California's Department of Insurance is referenced in NerdWallet's overview as recommending that buyers match policy type to both their goals and what they can realistically afford long term. That's good advice. The best policy isn't the one with the most features. It's the one you'll keep in force for the years your family needs it.

Finding and Comparing the Best Online Quotes

Online shopping makes life insurance much easier, but it also creates a new problem. You can get flooded with quotes that look comparable and aren't. One policy may be term, another may include different underwriting assumptions, and another may use a different health class than you'd receive.

What a useful quote comparison looks like

For a real apples-to-apples comparison, keep these details identical across every quote:

- Coverage amount: Don't compare one quote for a lower death benefit against another for a higher one.

- Term length: A shorter term will often look cheaper, but that doesn't make it a better value.

- Policy type: Compare term to term. Don't mix term and permanent products.

- Applicant profile: Use the same smoking status, health information, and demographic inputs each time.

For benchmarking, NerdWallet's cheap life insurance comparison lists sample monthly premiums for a 20-year, $500,000 term policy at $28.03 for a male and $23.78 for a female at Banner Life, with nearby competitors clustered around $28.04 to $31.33 for men and $23.79 to $26.18 for women. The same article states that the average cost for a healthy 40-year-old buying a 20-year, $500,000 term policy is $26 per month.

Those numbers are useful as a reality check, not a promise. If you're healthy and your quote lands near that range, you're probably looking at a competitive offer. If it comes in much higher, there may be a health, tobacco, or underwriting reason worth reviewing.

A broader quote-shopping walkthrough is useful if you want to see how digital marketplaces organize options and filters. This guide to best online life insurance quotes is a good example of what to review before choosing a policy.

What to have ready before you apply

Quoting is easier when you gather your information first. Ethos outlines a practical buying flow that starts with estimating your needs, then comparing quotes from multiple insurers, and then moving through underwriting and policy review before paying the first premium in its guide on how to buy life insurance.

Have these details ready:

- Basic personal information: Age, contact details, and beneficiary information.

- Health history: Current conditions, medications, past diagnoses, and family health history if asked.

- Lifestyle details: Tobacco use, high-risk hobbies, and driving history.

- Financial obligations: Mortgage balance, loans, and income information if you're still refining your coverage target.

The best online process feels simple. It's still insurance. Accuracy matters. If you rush inputs just to get to the lowest quote faster, you can end up comparing numbers that won't survive underwriting.

The Truth About No-Exam vs Fully Underwritten Policies

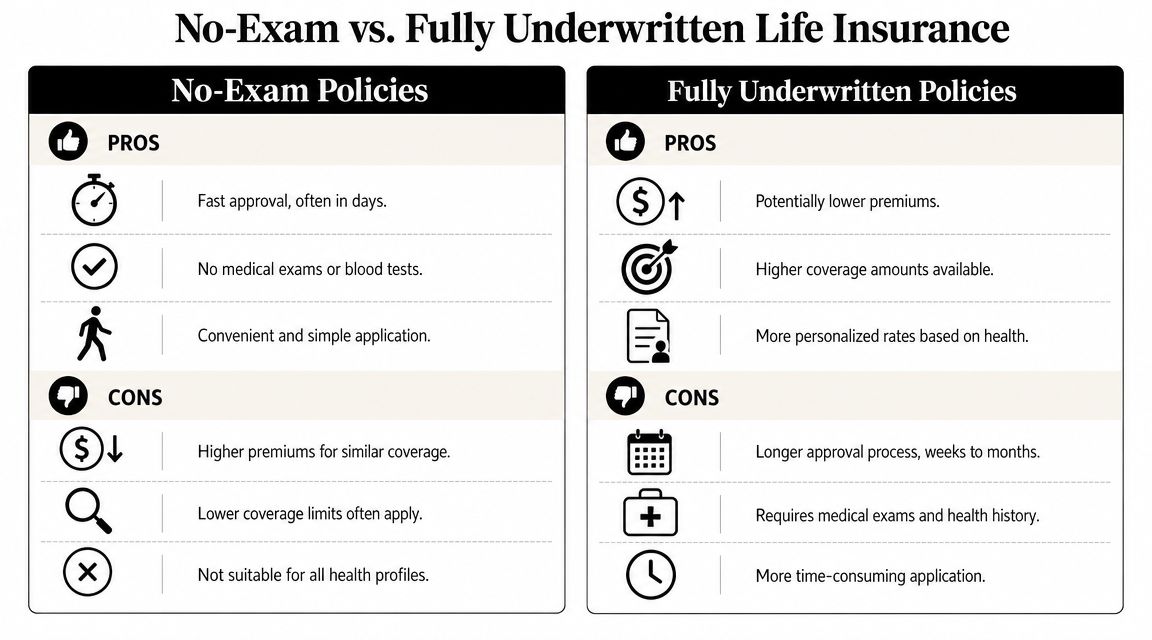

Much confusion surrounds no-exam policies. People hear “no-exam” and assume it's automatically the best path for affordable life insurance online because it's faster and easier. Sometimes it is. Sometimes it isn't.

What no-exam really means

A no-exam policy usually means you don't have to schedule a medical exam or blood draw. It does not mean the insurer skips underwriting entirely.

According to Policygenius on no-medical-exam life insurance, no-exam policies can be easier to get, but fully underwritten policies are commonly the cheaper option for the same death benefit because the insurer has more health data. The same source notes that no-exam applications still rely on health questionnaires, prescription history, driving records, and public records, while accelerated digital underwriting is making approvals faster without removing medical risk checks altogether.

That matters because many buyers chase speed without understanding the pricing tradeoff.

Here's a practical comparison:

| Policy path | Usually strongest advantage | Common downside |

|---|---|---|

| No-exam | Faster and more convenient | May cost more for similar coverage |

| Fully underwritten | Better shot at the lowest premium | More steps and a longer process |

For a quick overview of how insurers evaluate applications, this explanation of life insurance underwriting gives useful context.

Here's a short video that helps visualize the difference in process and expectations.

When fully underwritten is the better bargain

If you're healthy, patient, and trying to squeeze the most value out of a larger policy, a fully underwritten route often deserves serious consideration. Insurers can price more precisely when they have more information, and that precision often works in favor of healthier applicants.

No-exam coverage makes a lot of sense in a few situations:

- You need coverage quickly: A pending loan, business requirement, or family deadline can make speed more valuable than shaving the premium.

- You prefer a simpler process: Some buyers will pay a bit more to skip appointments and keep everything digital.

- Your application may still fit accelerated underwriting well: Some online-first processes can move quickly without making the premium feel heavily penalized.

Fully underwritten coverage often makes more sense when:

- You want the lowest long-term cost: Especially for larger death benefits.

- You're comfortable with a longer approval cycle: Savings can compound over years of premiums.

- Your health profile is strong: More data can help you earn a better class rather than a broader estimate.

Fast approval is valuable. But if you'll keep the policy for many years, the cheaper policy over time may be the one that asks more from you up front.

That's the central tradeoff. Don't ask only, “How fast can I get approved?” Ask, “What will this policy cost me for the years I'm likely to own it?”

Smart Strategies to Lower Your Life Insurance Premiums

You have more control over pricing than commonly assumed. Not total control, but enough to make a meaningful difference.

Ways to improve price without cutting protection

Some strategies are simple. Others require a little patience.

- Apply before life gets messier: Rates are generally better when you're younger and healthier. If coverage is already on your list, delaying rarely helps.

- Choose term if affordability is the goal: Permanent coverage has its place, but buyers focused on efficient protection usually get better value from term.

- Be precise about the amount and riders: Extra features can be useful, but they can also add cost. Keep what solves a real problem.

- Compare multiple carriers: Price variation between insurers is real. One quote is not the market.

- Consider whether your health profile deserves full underwriting: If you're in strong health, the cheaper path may be the one with more review.

- Revisit your rating if your health has improved: If you've made significant positive changes, review whether your current pricing still reflects your profile.

A rating class drives a lot of your premium. If you want to better understand how carriers think about risk tiers, this guide to life insurance rating is worth a read.

One caution. Don't cut the death benefit just to hit a prettier monthly number. The best premium strategy is usually to improve the fit and underwriting path, not to hollow out the coverage.

Your Next Step to Securing Affordable Coverage

The strongest move is simple. Figure out how much coverage your family would need, choose a policy type that matches that goal, compare quotes carefully, and don't assume no-exam is always the cheapest option. Sometimes speed wins. Sometimes underwriting saves more.

Affordable life insurance online isn't about buying the smallest premium you can find. It's about buying the most useful protection you can comfortably keep in force. When you approach it that way, the decision gets clearer and a lot less stressful.

If you want a simple place to start, get a quote from Coveredly. It's built for people who want online life insurance that's flexible, straightforward, and designed to fit real life without a drawn-out process.