You're probably here because life insurance sits in the same mental bucket as taxes, estate planning, and replacing your water heater. Important, but easy to push off. Maybe you just got married, bought a house, had a child, or realized other people now rely on your income. You want protection, but you don't want to overpay or spend weeks chasing paperwork.

That hesitation is common. Roughly 60% of Americans have some sort of life insurance policy, but 33% believe they are underinsured, according to The Zebra's life insurance statistics roundup. Waiting can also get expensive. The same source notes, via Policygenius, that premiums typically rise by 4.5% to 9.2% for each year a buyer waits to purchase coverage.

A cheap life insurance policy can be a smart move. But “cheap” only helps if the policy is also useful. The right goal is lower cost and solid protection, with a process that fits real life.

Table of Contents

- Your Guide to Truly Affordable Financial Protection

- Decoding the Price What Really Drives Your Premium

- Smart Strategies to Lower Your Life Insurance Costs

- Choosing the Right Coverage Without Overspending

- How to Compare Quotes and Find the Best Value Online

- The Modern Application From Online Forms to No-Exam Policies

Your Guide to Truly Affordable Financial Protection

Affordable life insurance matters most when your budget already feels spoken for. Mortgage. Rent. Childcare. Student loans. Groceries that somehow cost more every month. In that environment, searching for a cheap life insurance policy isn't careless. It's rational.

The problem starts when shoppers treat the lowest premium as the finish line. A small monthly payment can feel like a win right up until you ask what the policy would do for your family. If the answer is “not much,” the policy may be inexpensive, but it isn't good value.

That's why practical buyers do better with a different question: what's the lowest-cost policy that still protects the people and obligations that matter most?

Practical rule: Cheap should mean efficient, not stripped down.

For most young families and professionals, that means focusing on term life first. It's usually the cleanest fit for temporary high-responsibility years, when you're covering income, debt, and the cost of keeping a household running if something happens to you.

It also means moving before delay turns into a pricing problem. As noted in the opening data, premiums often rise when you wait. That doesn't mean you need to buy blindly. It means you should get clear on what affects price, what lowers it, and where cutting too far creates risk.

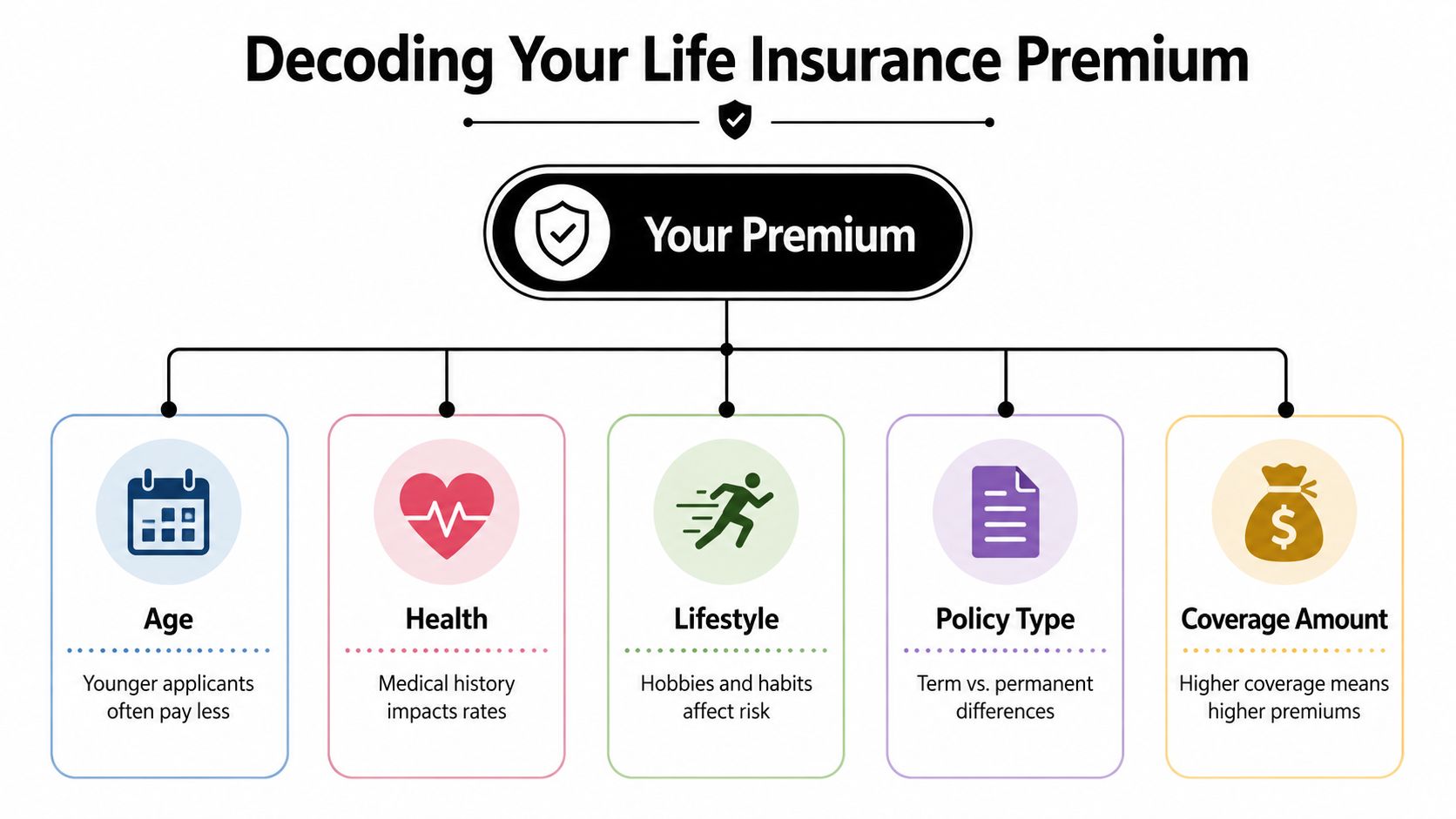

Decoding the Price What Really Drives Your Premium

Life insurance pricing isn't random. Insurers price around risk and policy design. Once you understand the main inputs, quotes stop feeling mysterious and start feeling predictable.

The biggest variables insurers look at

Some factors relate to you. Others relate to the policy you choose.

| Factor | Why it affects cost | What buyers can control |

|---|---|---|

| Age | Younger applicants often qualify for lower rates | Applying earlier |

| Health history | Medical conditions can change risk classification | Managing health where possible |

| Lifestyle | Tobacco use and certain hobbies can raise risk | Avoiding risky habits |

| Coverage amount | More death benefit usually means a higher premium | Choosing a realistic amount |

| Term length | Longer protection generally costs more per month | Matching the term to your need |

Age matters because insurers are covering a longer period of future uncertainty. Health matters because underwriting is trying to estimate the likelihood of a claim. Lifestyle matters for the same reason. Tobacco use, for example, often pushes pricing up meaningfully.

Policy design is where many buyers have the most flexibility. If you ask for a larger death benefit, expect a larger premium. If you pick a longer term, expect a higher monthly payment than a shorter term for the same person.

If you want a more detailed look at how age changes rates over time, this guide to life insurance rates by age is a useful companion.

How term length changes the monthly bill

One of the clearest pricing examples is term length. According to industry data summarized by Self's average life insurance cost analysis, the average 10-year term life policy cost $18.83 per month for a 40-year-old man, while the average 30-year term cost $43.93 per month for the same profile.

That doesn't mean the shorter term is automatically better. It means the insurer is charging more for a longer protection window.

Self's same dataset also shows how coverage amount changes price. For a 40-year-old, the average term life premium across sampled policies was $38.28 per month for $250,000 of coverage. In that dataset, women paid an average monthly cost of $32.64 for a $250,000 policy and $103.25 for a $1,000,000 policy.

A quote is usually telling you two things at once. What the insurer thinks about your risk, and what your policy choices are costing you.

That's why two shoppers with similar health can still see very different prices. One may choose a shorter term and lower face amount. The other may choose a larger benefit and a longer duration because they need it.

Smart Strategies to Lower Your Life Insurance Costs

A lower premium usually comes from better choices, not gimmicks. Some shoppers save money because they match the policy to the actual job it needs to do. Others pay more because they buy the wrong structure, apply at the wrong time, or focus so hard on price that they create cleanup work later.

What usually works

- Buy while your profile is simpler. Rates often look better when you're younger and healthier. If life insurance is already on your to-do list, getting quotes sooner usually gives you more options.

- Use term life for income protection years. If your main goal is replacing income, covering a mortgage, or protecting children during dependent years, term is often the most cost-efficient fit.

- Match the term to the liability. If your biggest concern is a mortgage or the years until your kids are more independent, choose a term that lines up with that window instead of defaulting to the longest option.

- Be accurate on the application. Clean, consistent answers help avoid delays and repricing issues later.

- Consider laddering in some situations. Some buyers split coverage across multiple term lengths so the amount drops as debts decline and savings grow. It's not for everyone, but it can align cost with changing obligations.

What usually backfires

The biggest mistake is shopping for a payment, not a plan. That's how buyers end up with a policy that looks affordable but leaves a surviving spouse with too little room to manage housing, childcare, and debt.

Another weak strategy is choosing permanent coverage when your real need is straightforward term protection. Permanent policies can be appropriate in some financial plans, but they're usually not the first stop for someone who wants a cheap life insurance policy and solid income replacement.

A third problem is picking a very short term just to force the monthly cost down. That can work if the need for coverage is brief. It fails when the coverage expires while your family still depends on your income.

Lowering cost works best when you trim mismatch, not protection.

Choosing the Right Coverage Without Overspending

The market is full of advice on finding the cheapest premium. Much less advice helps you decide how much coverage is still responsible. That gap matters because a low premium can hide a high risk if the benefit amount won't carry your family through the hard years.

Some guidance explicitly warns that chasing the cheapest policy can leave families underinsured. Liberty Mutual's overview on cheap life insurance makes that point clearly, noting that buying too little coverage can be a common mistake when people focus only on price.

Build your coverage around obligations

A good coverage amount starts with what would still need to be paid if you were gone.

Think through the list in practical terms:

- Income replacement: How much of your take-home income would your household need to keep operating?

- Debt payoff: Mortgage, private student loans, personal loans, and credit balances can all pressure the surviving household.

- Childcare and daily support: For many families, this is one of the least appreciated costs.

- Future education goals: Some buyers want room for college funding. Others focus only on the essentials.

- Final expenses and transition costs: Even a well-prepared family has immediate bills and logistical costs.

A quick rule of thumb can be useful as a starting point, but it shouldn't be the final answer. Real life isn't built on rules of thumb. It's built on your mortgage statement, your monthly budget, your children's ages, and whether one income or two keep the house running.

A simple way to pressure-test your number

If you're trying to decide whether a policy amount is enough, ask a blunt question: if your beneficiaries received that payout tomorrow, what would it solve?

Would it pay off the mortgage, or just cover a portion of it? Would it replace income long enough for your partner to adjust career plans or childcare arrangements? Would it reduce stress, or just postpone it?

That exercise usually tells buyers more than any generic formula.

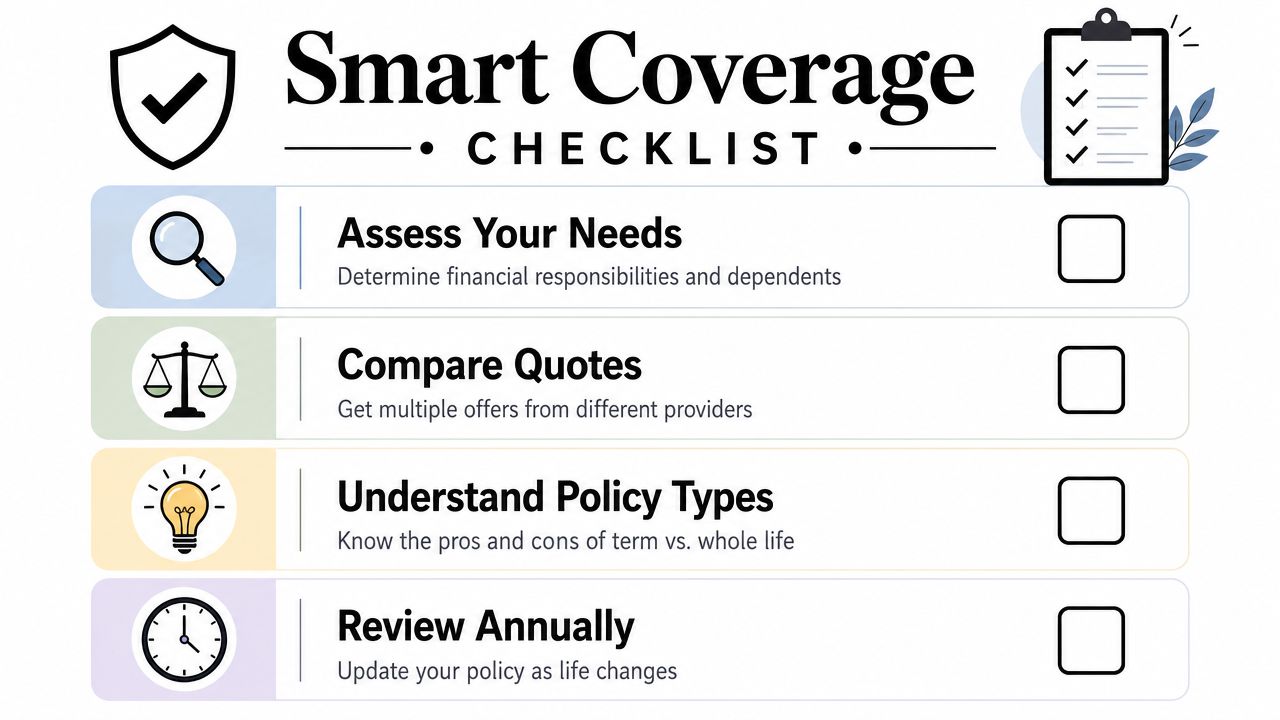

Here's a simple checklist you can use before buying:

- List your fixed obligations. Mortgage, debts, insurance, and recurring household costs.

- List your people obligations. Childcare, education goals, and support a spouse would need.

- Subtract available assets carefully. Only count savings or investments you'd realistically want your family to use.

- Choose the lowest premium that still meets the need. That's value.

Don't buy the smallest policy you can justify. Buy the smallest policy your family can actually live with.

A cheap life insurance policy serves as smart financial planning, not merely bargain hunting.

How to Compare Quotes and Find the Best Value Online

Online shopping makes life insurance faster, but speed can create lazy comparisons. Many buyers look at the monthly premium, pick the lowest number, and stop there. That's fine for a streaming subscription. It's weak due diligence for a contract your family may rely on years from now.

Read quotes like a buyer, not a browser

Start by collecting several quotes for the same broad scenario. Keep the term length and death benefit consistent enough that the comparison is fair. Then look beyond the headline price.

A strong quote review usually includes:

- Carrier reputation: Check the insurer's financial strength through established rating agencies.

- Policy type: Confirm you're comparing term to term, not term to permanent.

- Term length and face amount: Small mismatches can make one quote look cheaper than it really is.

- Conversion option: Some term policies let you convert to permanent coverage later, which can matter if your health changes.

- Application path: Some insurers use accelerated underwriting, while others may require more steps.

If you're comparing options side by side, this page on comparing term life insurance rates can help frame the shopping process.

Red flags worth noticing

Not every cheap quote is a good quote. Watch for signs that the low price may come with trade-offs you don't want.

| What to check | Why it matters |

|---|---|

| Missing policy details | You can't compare value if the term or benefit isn't clear |

| Unclear conversion rules | Flexibility later may matter more than you expect |

| Heavy reliance on teaser pricing | Initial numbers may not reflect your actual underwriting result |

| Friction in the application | Slow, confusing processes often signal a rough buyer experience |

Plain language helps here. If a quote or application path feels hard to understand, don't assume that confusion is normal. A good digital process should make the product easier to evaluate, not harder.

A better insurer doesn't just offer a lower premium. They make the contract, the process, and the trade-offs easier to understand.

The Modern Application From Online Forms to No-Exam Policies

The application experience has changed a lot. Buyers used to assume life insurance meant scheduling a nurse visit, waiting through back-and-forth paperwork, and hoping underwriting eventually came back with a decent rate. That still exists, but it's no longer the only path.

No-exam and accelerated underwriting have widened the menu. Policygenius notes that no-medical-exam life insurance now includes coverage up to $3 million. That matters because it changes the definition of a cheap life insurance policy. It's no longer just “the lowest monthly premium possible.” It can also mean lower friction, faster approval, and enough coverage to be meaningful.

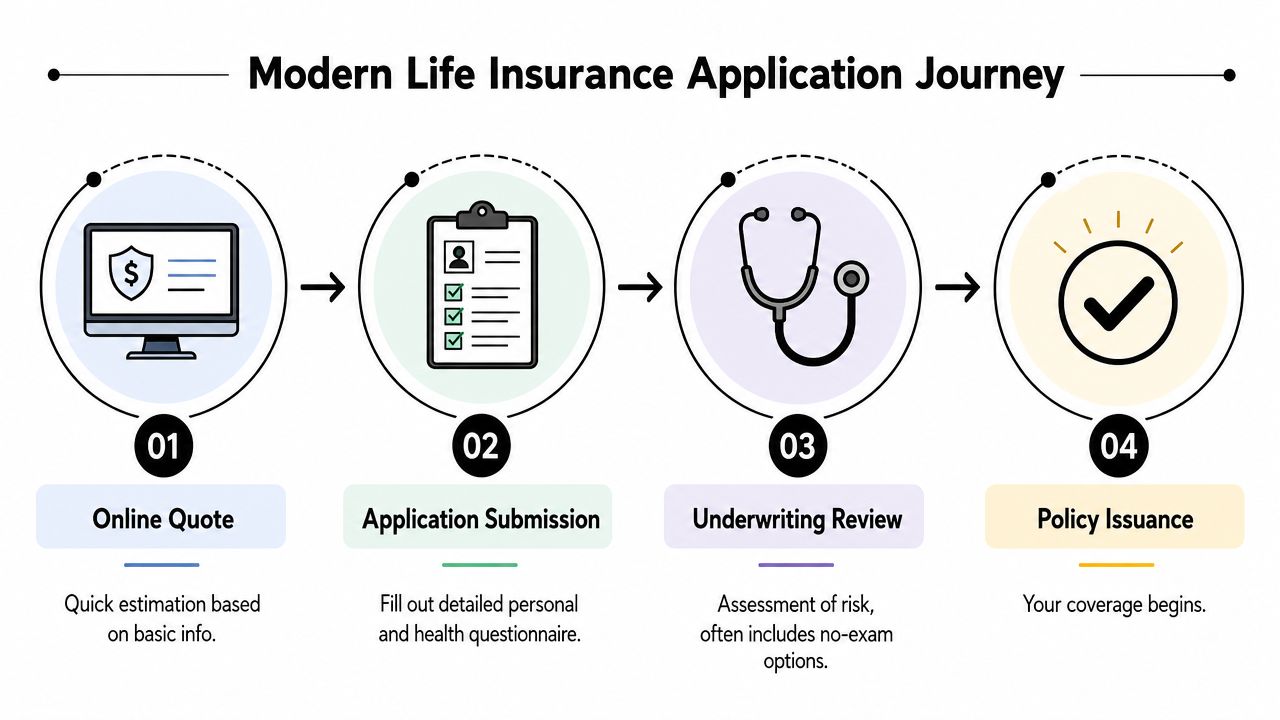

What the application usually looks like now

Most digital-first applications follow a similar path:

- Initial quote. You enter basic details like age, location, and desired coverage.

- Full application. This usually includes beneficiary information, health history, medications, and lifestyle questions.

- Underwriting review. The insurer reviews the application and may use external records or additional questions.

- Decision and policy issue. If approved, you review final terms and activate coverage.

Some buyers still go through traditional full underwriting with a medical exam. Others qualify for accelerated review without one. If you want a sense of how these products are structured, this guide to no-exam term life insurance is a helpful reference.

When no-exam coverage makes sense

No-exam coverage is often attractive for busy professionals, parents with limited time, and buyers who want less scheduling friction. It can also make sense when convenience has real value, especially if the alternative is postponing the purchase again.

But speed isn't automatically the cheapest route in every case. Someone in excellent health may find that a fully underwritten policy delivers a better rate for the same death benefit. That's the core trade-off. Faster and easier versus potentially lower pricing through a more detailed underwriting path.

A practical way to consider it:

- Choose no-exam first if speed, convenience, and an efficient process are high priorities.

- Consider full underwriting if you're highly price-sensitive and comfortable with a longer process.

- Compare both paths when available, especially if you're buying a larger amount of coverage.

The best buyers don't treat no-exam as a shortcut or full underwriting as automatically superior. They use each option for what it does well.

Convenience has value. So does a lower long-term premium. The right choice depends on which one matters more in your situation.

If you want a simpler way to shop, Coveredly is built for people who want life insurance to fit real life. You can explore digital options, compare practical paths to coverage, and see whether fast, flexible term life makes sense for your budget, timeline, and family needs.