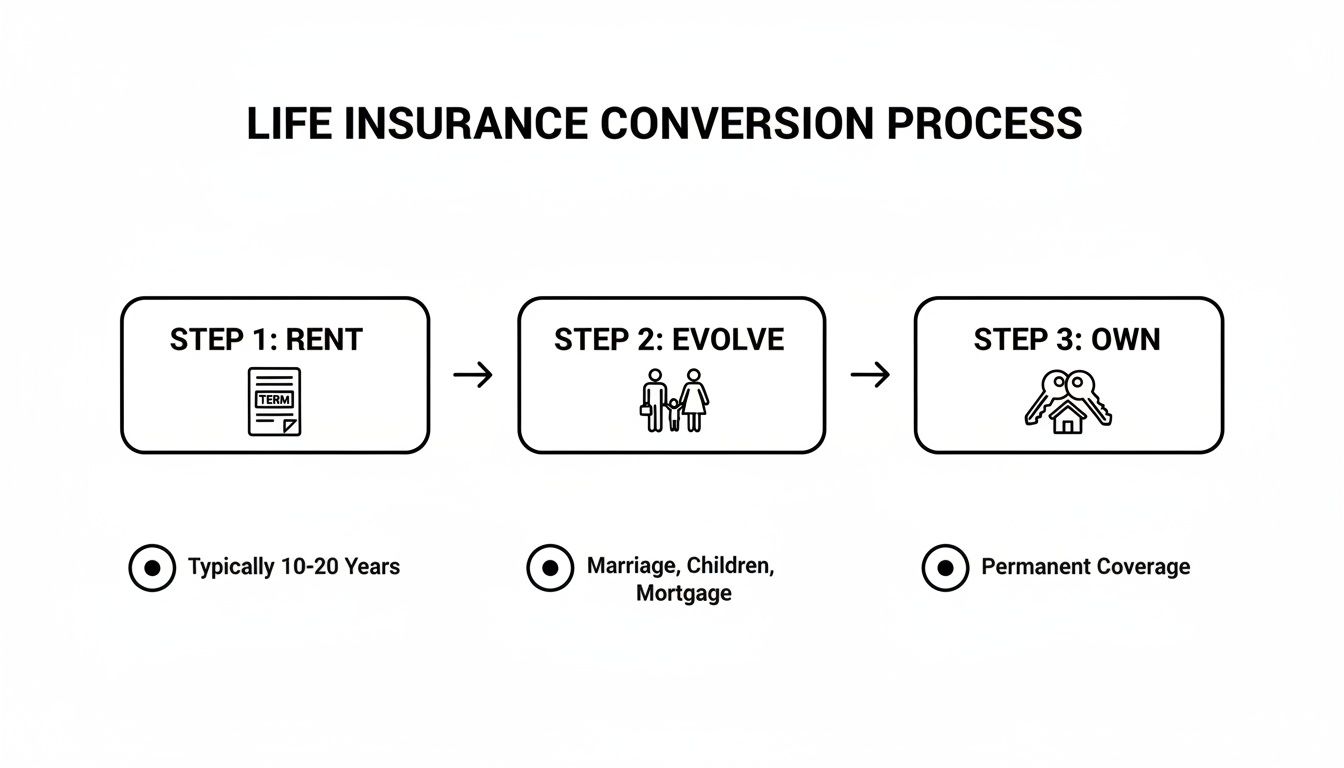

Converting your term life insurance to a whole life policy is a big financial decision, almost like choosing to buy a home after renting for years. You’re shifting from temporary coverage to a permanent asset that builds its own cash value over time.

The biggest benefit? Locking in coverage for life at your original health rating, often without needing another medical exam. This is a crucial element of any term life conversion strategy.

Is Converting Your Term Life Policy a Smart Move?

Think of your term life policy as renting financial protection. It’s affordable and perfect for covering big, temporary needs—like a mortgage or raising young children. But what happens when that "lease" is up?

For many people, converting to a whole life policy is the logical next step. It’s like turning that rental into permanent homeownership. This move not only gives you lifelong coverage but also introduces a savings component, making your policy a more versatile financial tool.

This isn’t just a simple paperwork change; it's a strategic move for your long-term peace of mind. One of the most powerful reasons to convert is to protect your insurability. If your health has changed for the worse since you first bought your term policy, a conversion lets you get permanent coverage without facing a new medical exam—an exam that could otherwise lead to sky-high premiums or even a denial.

A Real-World Scenario for a Growing Family

Let's look at a common situation I see all the time. Imagine a man in his early 30s, newly married with a baby on the way. He does the smart thing and buys a 20-year term life policy to protect his family affordably.

Fast forward 15 years. His kids are getting closer to college, the mortgage is smaller, and he’s starting to think about retirement. But his health isn't what it was back then. This is the exact moment where converting can be a game-changer.

Industry data shows a surprising number of term policies lapse before they pay out, which can leave families exposed at the worst possible time. By converting his term life to whole life, he can lock in his insurability based on his younger, healthier self. While Social Security data shows a 50-year-old male has a low probability of passing away, the cost of a new policy at that age would be drastically higher due to his age and any new health issues.

The core value of a term life conversion is simple: It guarantees you can keep your life insurance coverage, no matter how your health or life circumstances change. It’s a safety net for your future self.

Understanding the Fundamental Shift

When you decide to convert, you're fundamentally changing what your insurance does for you. You’re moving from a product designed purely for protection to one that combines that protection with a financial growth component.

This table breaks down what that shift looks like in practice.

Term Life vs. Whole Life At a Glance

| Feature | Term Life Insurance | Whole Life Insurance (Post-Conversion) |

|---|---|---|

| Coverage Duration | For a specific period (e.g., 10, 20, 30 years) | Lifelong, as long as premiums are paid |

| Premiums | Lower, fixed for the term | Higher, but builds equity |

| Cash Value | None | Builds a tax-deferred cash value over time |

| Primary Purpose | Pure death benefit protection | Death benefit + a savings/investment tool |

| Complexity | Simple and straightforward | More complex, with features like policy loans |

As you can see, the change is significant. You move from a simple, temporary safety net to a permanent, multi-faceted financial asset.

If you're weighing your options, getting a firm grasp on these differences is the first step. You might find our detailed guide on the differences between term and whole life insurance helpful for a deeper dive. This foundational knowledge is key to making a choice you'll be happy with for years to come.

Your Guide to the Policy Conversion Process

So, you have a term life policy. That’s a smart move for protecting your family during your most critical financial years. But what happens when those years start to wind down and you realize your need for coverage might not have an expiration date?

This is where one of the most valuable—and often overlooked—features of your policy comes in: the option to convert term life to whole life. Let's walk through exactly how this works, step by step, so you can make a confident decision.

The journey is a lot like the shift from renting a home to owning one. You start with temporary protection, but as your life evolves, you might decide to secure permanent ownership of your coverage.

Find Your Conversion Rider

First things first: you’ll need to pull out your original term life policy documents. Don’t worry if they’re a bit dusty. You’re hunting for a specific clause called a conversion rider or conversion privilege.

This is the golden ticket. It's the part of your contract that grants you the right to switch your temporary policy to a permanent one, usually without needing a new medical exam. Think of it as a pre-approved upgrade you wisely secured when you first bought the policy. Finding this rider is your green light.

Check Your Deadlines and Eligibility

Once you've located the rider, the clock starts ticking. You need to zero in on two critical details: your eligibility and the deadline. Insurers don't leave this window open forever.

Most policies will specify a conversion period. This could be:

- Within a set number of years (e.g., the first 10 years of a 20-year term).

- Before you reach a specific age (like before your 65th or 70th birthday).

- Anytime before the term policy officially expires.

Missing this deadline is a big deal—it means you forfeit your right to convert without proving your health again. It’s absolutely crucial to know this date. Pro tip: the sooner you convert, the lower your new premiums will be, since they’re based on your age at the time you make the switch.

Request a Conversion Illustration

With your eligibility confirmed, it’s time to get some real numbers. Reach out to your insurance company or agent and ask for an in-force illustration for converting your policy.

This isn’t a bill or a commitment. It’s a detailed projection that shows you exactly what the new whole life policy would look like. It will break down several key figures:

- The new premium: This will be higher than your term premium, and for good reason. It’s buying you lifelong coverage and building cash value.

- Guaranteed cash value growth: You’ll see a year-by-year table showing how the policy's savings component is projected to grow.

- The death benefit: This confirms the payout amount. Many insurers also allow a partial conversion, letting you convert just a piece of your term coverage to make the new premium more manageable.

Take your time with the illustration. This document turns the abstract idea of "converting" into concrete numbers that will shape your budget and long-term financial plan. It's the foundation for your decision.

Compare the Costs and Handle the Paperwork

Now for the final decision. Lay the new premium from the illustration next to your monthly budget. Does the cost of permanent protection and a growing cash value asset fit into your financial picture? Weigh that against the alternative—your term policy eventually expiring and leaving you with no coverage.

For many of the young professionals and new parents we work with at Coveredly, locking in permanent coverage is worth every penny. Your future health is an unknown, but your family’s need for financial security is a constant.

If you decide to move forward, the last step is the paperwork. Your insurer will give you a simple conversion application. Because you’re just exercising a right that’s already in your contract, you typically won’t have to answer any medical questions or take an exam.

Once the forms are submitted and approved, you're all set. You’ve successfully upgraded your temporary protection into a permanent financial asset for your family.

When Should You Convert Your Policy? Timing is Everything

Knowing how to convert your term policy is just the first step. The real art is knowing when. Certain life milestones are natural signals that it might be time to make your coverage a permanent part of your financial strategy.

Maybe your term policy was originally for covering the mortgage and protecting your kids while they were young. But what happens when those needs change? Paying off your house or watching your youngest head off to college are huge achievements—and perfect moments to reassess your life insurance.

The same goes for your career. A major promotion, a successful business sale, or a significant jump in your income can completely shift your financial picture. Suddenly, you might be thinking less about pure income replacement and more about estate planning or building a tax-advantaged asset for retirement. These are prime opportunities to consider the switch from term to permanent coverage.

Finding Your Conversion “Sweet Spot”

There's often a financial "sweet spot" for converting your term policy, and it's usually midway through the term period. By then, you're likely on more solid financial ground than when you first bought the policy, making the higher premiums of whole life more affordable.

At the same time, you haven't waited so long that age-related premium hikes become a major hurdle. Converting earlier locks in a lower permanent rate based on your age at the time of the switch—not when you first bought the policy.

Think of these common moments as green lights for conversion:

- You Got a Big Raise: A promotion or new job means you can now comfortably handle permanent premiums without straining your budget.

- Your Family’s Needs Have Changed: You might have a new child, or perhaps you've taken on the responsibility of caring for an aging parent, extending your need for coverage indefinitely.

- You’ve Had a Health Scare: This is a big one. If you've developed a new health condition, converting allows you to secure lifelong coverage using the better health rating you had when you were younger. It’s a massive advantage you can’t get any other way.

- You're Thinking About Your Legacy: You want to leave a guaranteed inheritance for your loved ones or ensure there's money available to cover estate taxes.

The Real Cost of Waiting: A Scenario

Let's look at Sarah, a 40-year-old professional. At age 30, she bought a 20-year, $750,000 term policy to protect her growing family. She's now considering making it permanent.

If Sarah converts today, her new premium will be based on the rates for a healthy 40-year-old. But what if she puts it off? If she waits another five years and converts at 45, her new premium will be significantly higher—even if her health stays exactly the same. That difference could easily be hundreds of dollars more per year, adding up to thousands over the life of the policy.

This highlights a core truth about converting term to whole life: waiting rarely makes it cheaper. The younger you are when you convert, the lower your lifetime premiums will be for your new whole life policy.

Flipping the Odds in Your Favor

As a young family who secured affordable term life insurance through a platform like Coveredly, you’ve already made a smart financial decision. But it's crucial to remember what term insurance is designed for. Most policies expire without a payout. In fact, industry data shows that as many as 92% of term policies never pay a claim because people outlive the term or can't requalify for new coverage later.

Converting to whole life flips these odds by guaranteeing lifetime coverage, locking in the good health you had when you first applied.

For example, a 25-year term policy for $750,000 bought at age 30 for $20/month might convert at age 40 to a whole life policy for roughly twice that premium. But the new policy starts building cash value immediately—often reaching 10-15% of the face value within just 10 years.

You can discover more insights on the benefits of switching your insurance on TruStage.com.

Weighing the Financial Pros and Cons of Conversion

So, you're thinking about converting your term policy. It's a big decision, and it really comes down to a trade-off: paying more now for permanent benefits that last a lifetime.

It's a strategic move, but is it the right one for your budget and your family's future? Let's get into the real-world numbers and weigh the pros and cons of term life conversion.

The Upside: Guaranteed Lifetime Value

The biggest win here is locking in permanent coverage. Your term policy has an expiration date, but a converted whole life policy guarantees a death benefit for your loved ones, no matter when you pass away—as long as you keep paying the premiums.

That alone brings incredible peace of mind. It turns your life insurance from a temporary safety net into a permanent part of your legacy, ensuring money is there for final expenses, an inheritance, or even a gift to charity.

Another massive pro is locking in your insurability. This is huge. If your health has taken a turn since you first bought your term policy, converting allows you to get permanent coverage based on the health rating you got years ago. No new medical exam needed.

The Downside: The Premium Increase

Let's be real: the biggest hurdle is the price tag. Whole life insurance premiums are significantly higher than term premiums for the same death benefit. This isn't just a random price hike; you're paying for two powerful features your term policy doesn't have:

- Lifelong Coverage: The policy is priced to cover you for the rest of your life, not just for 10, 20, or 30 years.

- Cash Value Accumulation: A piece of your premium goes into a savings-like account that grows over time, tax-deferred.

That higher monthly premium is the main thing you need to square with your budget. The benefits are powerful, but only if you can comfortably afford them for the long haul. To dig deeper into the numbers, check out our guide on how much whole life insurance costs.

Building a Flexible Financial Asset

Beyond just the death benefit, the cash value is what makes whole life so appealing to many. Think of it as a forced savings plan that grows on a tax-deferred basis, creating a pool of money that becomes a flexible financial tool you can use while you're still living.

You can borrow against this cash value for almost any reason—a down payment on a vacation home, a kid’s college bills, or to supplement your income in retirement. Policy loans do have interest and will lower your death benefit if you don't pay them back, but they offer a source of cash without a credit check.

The cash value component transforms your insurance from a pure expense into a versatile asset. It's protection for your family if you're gone and a source of funds for you if you live a long life.

Think about a professional in their 40s whose 10-year term policy is about to expire. They’ve built a successful business, but renewing their term coverage means a new medical exam, which is a gamble if their health has changed. This is where conversion is a game-changer. Data from Farm Bureau Financial Services shows a whole life policy starts building cash value right after conversion. A $500,000 policy could build over $100,000 in cash value in just 20 years. This is a stark contrast to term insurance, where industry data suggests only one in ten policies are ever converted before they lapse. You can discover more about the reasons to convert to whole life insurance on FBFS.com.

A Clear Look at the Numbers

To make this all a bit more tangible, let's look at a hypothetical 40-year-old converting a $500,000 term policy. Their original term premium might have been just $40 per month. After converting, their new whole life premium could jump to around $450 per month.

That’s a big leap, no doubt. But here’s how the value starts to build on the other side of the equation.

Sample Cost & Cash Value Projection After Conversion

The table below shows how the new premium contributes to a growing asset—the cash value—while keeping the death benefit secure.

| Age | Annual Premium | Guaranteed Cash Value | Total Death Benefit |

|---|---|---|---|

| 50 (Year 10) | $5,400 | $48,000 | $500,000 |

| 60 (Year 20) | $5,400 | $110,000 | $500,000 |

| 70 (Year 30) | $5,400 | $185,000 | $500,000 |

Note: These are illustrative figures. Actual premiums and cash value growth will vary based on the insurer, policy, and your age/health class.

As you can see, while the annual cost is higher, a large chunk of that premium is being redirected into an asset that you own and control. Over time, the cash value becomes a significant financial resource, all while the $500,000 death benefit remains guaranteed for your family.

Exploring Smart Alternatives to a Full Conversion

Converting your entire term policy to whole life isn't your only move. For many young families and professionals, taking that big of a financial leap all at once can feel daunting. The good news is this isn't an all-or-nothing decision.

You have more flexibility than you might think. By thinking creatively, you can build a long-term strategy that balances permanent protection with your budget, without forcing you into a one-size-fits-all box. Let's look at a few alternatives to term conversion.

The Power of a Partial Conversion

One of the most effective strategies I recommend is a partial conversion. It’s exactly what it sounds like: you convert just a portion of your term policy’s death benefit to whole life and leave the rest as affordable term coverage. It’s a powerful hybrid solution.

Imagine you have a $1 million 20-year term policy. Instead of converting the whole thing, you could convert just $250,000 to a permanent whole life policy, keeping the remaining $750,000 as term. This approach gives you the best of both worlds.

- You get a permanent policy to cover final expenses, leave a small legacy, or start building cash value.

- You keep a large amount of affordable term coverage for the years you need it most—while the mortgage is high and the kids are still at home.

This makes the move to permanent insurance much more manageable from a cost perspective. You lock in lifelong coverage without committing to the much higher premium of a full $1 million whole life policy.

Buying a New Whole Life Policy

Here’s another path: keep your existing term policy as is and simply buy a completely new, separate whole life policy. This might sound a little counterintuitive, but it can be a fantastic move if you're still in excellent health.

If you can pass a new medical exam and lock in a preferred health rating, you might find the premiums for a brand-new whole life policy are surprisingly competitive. This route also gives you the freedom to shop around with different insurers, whereas a conversion locks you into the options offered by your current provider.

The catch, of course, is that medical exam. If your health has declined since you first bought your term policy, this strategy probably won't work in your favor. In that case, your conversion privilege is a golden ticket.

For those with a clean bill of health, shopping for a new whole life policy provides maximum flexibility and choice. But for anyone whose health has changed, the conversion privilege in your term policy is an invaluable asset you don't want to waste.

Stacking Policies with a Laddering Strategy

While not a direct alternative to conversion, "laddering" is a related strategy for managing coverage and costs over time. A laddering approach involves buying multiple term policies with different term lengths to match your declining financial obligations.

For instance, a young professional might buy:

- A 30-year term policy to cover their mortgage.

- A 20-year term policy to protect their family until the kids are financially independent.

- A 10-year term policy to cover shorter-term business or personal debts.

As each smaller policy expires, your total coverage and premium costs drop. This is a highly efficient way to handle temporary needs, but it doesn't solve the problem of needing lifelong coverage. However, it can be combined with a conversion—you could ladder your term policies and then convert one of them to whole life down the road.

You might also be interested in a unique hybrid option; learn more about cash value term life insurance in our dedicated guide.

Your Conversion Questions Answered

Even after getting the facts straight, you probably have a few practical questions still rolling around in your mind. That's completely normal. Converting a policy is a big decision, and the details matter.

Let's tackle the most common questions we hear from people just like you who are weighing their options.

Can I Still Convert If My Health Has Gotten Worse?

Yes. And honestly, this is the single most powerful reason to have a conversion rider in the first place.

When you convert your policy, you’re using a right that was built into the original term contract you signed years ago. This means you get to keep the same health rating you qualified for back then—even if you’ve since developed a chronic illness, had a major health scare, or just aren't as healthy as you used to be. You won’t need to go through another medical exam. For anyone whose health has changed, this feature is priceless.

Do I Have to Convert My Entire Death Benefit?

No, and you probably shouldn't if budget is a concern. Most insurance companies offer partial conversions, which is a brilliant way to balance cost with the need for permanent coverage.

Let’s say you have a $1,000,000 term policy. You could choose to convert just $250,000 of it into whole life insurance and leave the other $750,000 as a term policy. This strategy gives you a permanent death benefit for final expenses or a small legacy, while you keep the larger, more affordable coverage for the years you need it most.

A partial term conversion is often the ideal solution. It allows you to secure a foundation of lifelong coverage without committing to the higher premium of a full conversion, giving you flexibility that fits your budget.

What Happens to the Premiums I Already Paid?

This is a great question, and we get it all the time. The simple answer is that those premiums paid for the protection you received during the term. They don't get credited or rolled into your new whole life policy.

Think of it like renting an apartment. All the rent you paid over the years gave you a place to live, but that money doesn't go toward a down payment when you finally decide to buy a house. Your term premiums bought you valuable peace of mind, and your new whole life premiums will now start building your policy's cash value from day one.

Are There Any Hidden Fees for Converting?

Generally, no. You shouldn't expect to see a line item for a "conversion fee" from the insurance company. The main financial change is simply the new, higher premium for the whole life policy you're moving into.

That premium increase isn't a fee—it reflects the completely different structure of the new policy, which includes lifelong coverage and a cash value savings component. It's always smart to ask your provider to be sure, but the process is usually straightforward without extra charges.

Will My New Premium Ever Increase?

Once you lock it in, your premium for the new whole life policy is guaranteed to stay the same for the rest of your life. This is a core feature of traditional whole life insurance.

Unlike your term policy, which would get much more expensive if you tried to renew it after the term ends, your new whole life rate is set based on your age at conversion and never changes. That predictability is a huge plus for anyone planning their finances for the long haul.

Ready to see what a conversion could look like for you? At Coveredly, we make life insurance digital, affordable, and flexible. Explore your options and get the protection that fits your life by visiting Coveredly.com.