You're often handed an Evidence of Insurability form at a busy moment. You started a new job, got married, had a child, or decided the basic life insurance from work isn't enough. Then HR or the insurance carrier asks for health details, signatures, and maybe more paperwork than you expected.

That can feel unsettling fast. Many people assume they're just checking a box, when the evidence of insurability EOI form is the insurer's way of deciding whether to approve extra coverage beyond the automatic amount.

The good news is that this process is manageable when you know what the form is really asking, what mistakes matter, and where the hidden risks are.

Table of Contents

- Understanding the Evidence of Insurability Form

- What Is Evidence of Insurability and Why It Matters

- When Insurers Typically Require an EOI Form

- A Walkthrough of the EOI Form Questions

- Common Pitfalls That Can Delay or Deny Your Coverage

- The Underwriting Process After You Submit

- The Coveredly Approach to Getting Life Insurance

Understanding the Evidence of Insurability Form

If you've never seen one before, an Evidence of Insurability form can look more serious than a normal benefits election. That's because it usually appears when you want more coverage than your plan gives automatically, or when you're making a change outside the standard enrollment window.

At its core, the form is a health questionnaire tied to underwriting. The insurer wants to know whether the person asking for added coverage fits its rules for that amount of risk. That means questions about your health, medical history, medications, and everyday habits may all show up on the form.

This process is common. In 2024, over 2.7 million Evidence of Insurability applications were received across the U.S. group insurance market, according to Gen Re's U.S. group insurance EOI survey.

Why this form feels more intimidating than it is

The idea of life insurance doesn't typically cause confusion. Instead, timing, terminology, and consequences are often the confusing elements.

You might wonder:

- Is this just a formality? Sometimes it isn't.

- Do I already have the full coverage? Not always.

- Do I need to mention symptoms that aren't diagnosed yet? Often, careful disclosure matters.

- Will I need an exam? It depends on the insurer and the amount requested.

Practical rule: Treat the EOI form like part of the insurance application, not like routine HR paperwork.

That mindset helps. It nudges you to slow down, gather accurate information, and answer with care instead of rushing through it between meetings or after bedtime.

What usually happens next

Once you submit the form, the insurer reviews what you provided and decides whether to approve the additional coverage, modify the offer, or decline it. Some people move through this without much friction. Others hit delays because a doctor's contact information is incomplete, a signature is missing, or a health answer raises follow-up questions.

The form may feel intrusive, but it's still manageable. When you know why each question is there, the process becomes much less mysterious.

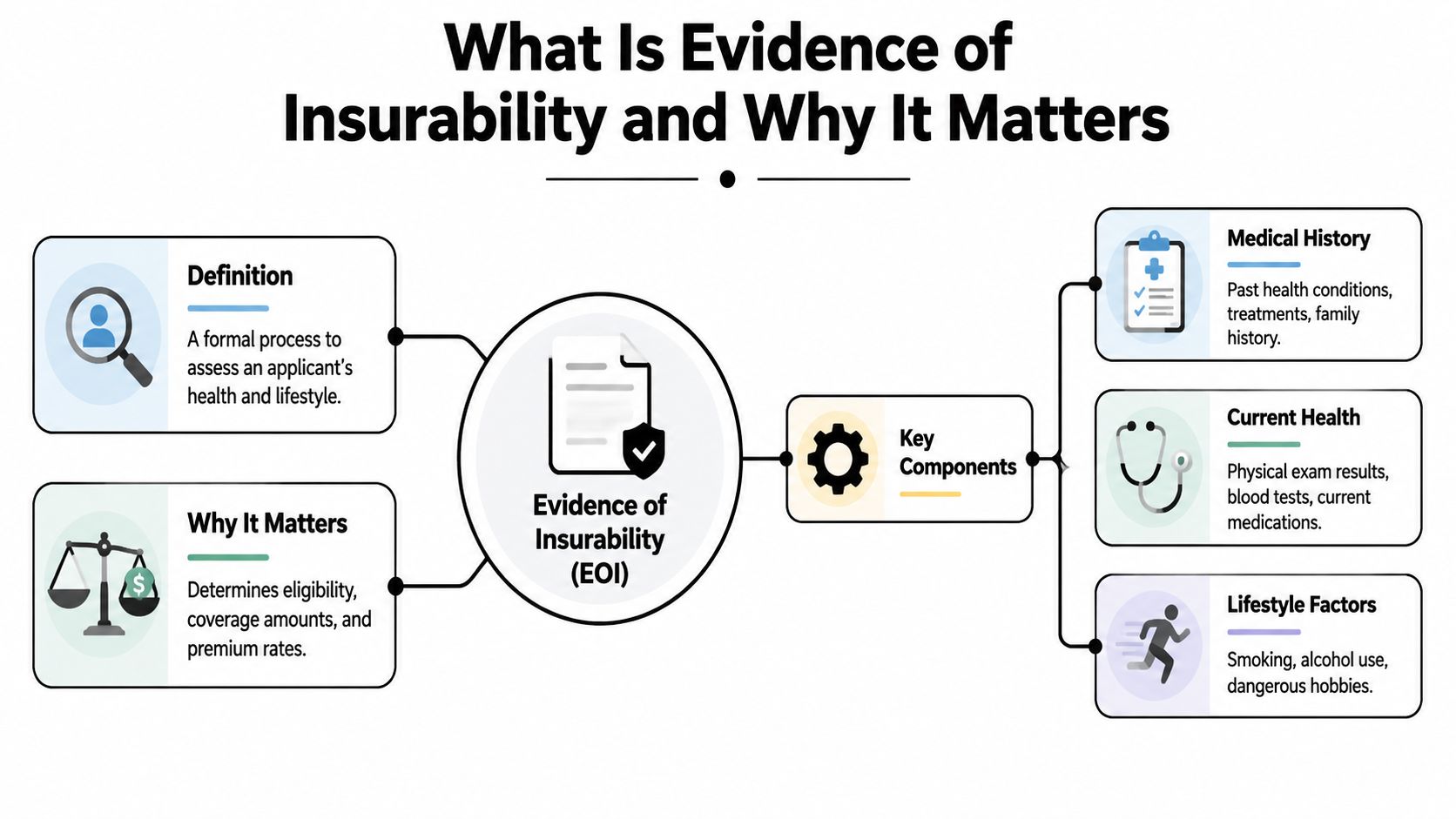

What Is Evidence of Insurability and Why It Matters

A plain English definition

Evidence of insurability means showing an insurer enough health and lifestyle information for it to decide whether to approve the coverage you want. It's more than a single sheet of paper. It's a review process.

A simple way to think about it is a loan application. If you borrow a small amount, the bank may ask for less documentation. If you ask for much more, the bank wants a closer look. Insurance works in a similar way. When you request more life or health-related coverage than your employer provides automatically, the insurer often wants more information before saying yes.

The evidence of insurability EOI form is the tool that starts that review. The form can ask about medical conditions, medications, surgeries, family history, tobacco or alcohol use, and higher-risk activities. In some cases, insurers may also request medical records, bloodwork, lab tests, or a physical exam.

Why insurers ask for more information

The insurer is trying to measure risk. That's the business reason behind the form.

A standard employer plan often includes a Guaranteed Issue amount. That's the portion available without health questions. Once you go beyond that level, the insurer may need a closer look at whether your current health supports the larger amount of coverage.

That's one reason this process matters so much in real life. The bigger your requested benefit, the more important it is to understand that the insurer is not merely processing paperwork. It is making an underwriting decision.

Here are the main things the insurer is evaluating:

| Area | What the insurer looks for |

|---|---|

| Personal details | Age, date of birth, height, weight, requested coverage |

| Medical history | Prior diagnoses, surgeries, medications, family history |

| Current health | Ongoing treatment, records from doctors, possible follow-up requirements |

| Lifestyle factors | Tobacco use, alcohol use, hazardous activities, some job-related risks |

That's why the form matters beyond HR administration. It affects eligibility, coverage amount, and possibly premiums.

When people understand the insurer's logic, the questions feel less random and more answerable.

A lot of guides stop at the definition. The more useful point is this: the form isn't there to trap you, but it does expect accuracy. If you treat it casually, the insurer may treat your answers as incomplete, inconsistent, or risky.

When Insurers Typically Require an EOI Form

The most common time this form appears is when someone wants more life insurance than the plan allows automatically. That often happens during onboarding, annual benefits enrollment, or after a life change that makes basic coverage feel too small.

The most common trigger

The clearest trigger is requesting coverage above your employer's Guaranteed Issue amount. Western & Southern explains that the EOI process is triggered when an applicant requests life insurance beyond the employer's GI amount, and that verification typically spans 30 business days while the insurer validates medical data through its overview of evidence of insurability.

If you're also trying to understand how medical review can fit into life insurance generally, this guide to a life insurance medical exam helps explain the broader context.

A practical example makes this easier to see. Suppose your employer gives you a basic amount automatically, but you elect a larger voluntary benefit for your spouse or children's protection. That extra amount may trigger an EOI review because it goes beyond the guaranteed threshold.

Other times the form shows up

The form can also appear when timing becomes the issue rather than the amount.

Common situations include:

- Late enrollment: You skipped coverage when you were first eligible and want to add it later.

- Coverage increases: You decide during open enrollment that you want a larger benefit than before.

- Certain status changes: Marriage or other qualifying events can open a change window, but not every increase is automatic.

- Dependent coverage requests: Coverage for a spouse may trigger separate review depending on the plan.

Some forms are even structured differently depending on who is being covered. In the group insurance market, employee-only coverage generally uses one set of form sections, while dependent coverage uses another. Children typically don't need EOI documentation in many cases, but plan rules still matter.

Why people get caught off guard

The confusing part isn't usually the trigger itself. It's the assumption that if payroll starts deducting for the higher amount, approval must already be done.

That assumption can create problems later.

If your coverage request is above Guaranteed Issue, stop and confirm whether the added amount is pending underwriting or already approved.

It's a small question, but it can save a lot of confusion. Many people never ask it because the enrollment process feels automatic.

A Walkthrough of the EOI Form Questions

A typical evidence of insurability EOI form is easier to handle when you read it in chunks instead of as one long document. Think of it as a series of mini-decisions. The insurer wants to confirm who you are, what coverage you want, how your health history looks, and whether anything requires follow-up.

The basic information section

Most forms begin with straightforward identification details. That usually includes your age, date of birth, height, weight, and the amount of coverage you're requesting. Ethos notes that the form requires personal data like age and weight alongside medical history, and for new employees the submission window is 31 days from the date of employment, with an extra 15 days just for the EOI form, with forms signed and submitted through approved methods such as fax or mail according to its explanation of the EOI process.

This part feels easy, but accuracy matters. Don't guess on dates, current medications, or coverage amounts if you can verify them from your benefits portal or enrollment paperwork.

A good way to approach this section is to gather a few things first:

- Your benefits election details: Confirm the exact amount you requested.

- Your doctor's contact information: Use current information, not an old provider you haven't seen in years.

- Your medication list: Include names and dosages if the form requests them.

- Your dates: Employment date, procedure dates, and diagnosis dates should be as accurate as possible.

The medical history section

Many applicants slow down at this point, and they should. The medical history section often asks about pre-existing conditions, surgeries, medications, treatments, and family history.

If you've been diagnosed with something, disclose it clearly. If you had a surgery, include the date or approximate timeframe if the form allows that. If you take prescriptions, list them carefully. Insurers may compare your answers with medical records they later request.

A common mental trap is answering only what feels “serious.” That's not always the right standard. If the form asks whether you've been treated, tested, or advised to follow up for a condition, answer what was asked.

A helpful habit: Read each medical question twice. First for the plain meaning, then for the exact wording.

Here's a simple example. If the form asks whether you've had consultations, tests, or treatment related to a condition, an applicant who says “I don't have a diagnosis” may still need to disclose recent medical evaluation if it fits the question.

Lifestyle and physician details

Lifestyle questions can feel awkward because they mix health and personal behavior. Many forms ask about tobacco use, alcohol use, dangerous hobbies, and sometimes risky work activities. The point isn't moral judgment. The insurer is looking for risk indicators.

Hazardous activities can include things like skydiving, depending on the form. If your hobby is unusual, don't assume the insurer won't care. If the question is broad, answer broadly and let the insurer decide what matters.

The final stretch often includes physician information and an authorization section. There, you let the insurer obtain records from your healthcare providers.

A few closing checks can prevent avoidable delays:

- Review every blank field. Empty boxes often trigger follow-up.

- Confirm the signature and date. Unsigned forms can stall quickly.

- Use the required submission method. If the carrier says fax, mail, or a secure portal, follow that method exactly.

- Keep a copy. Save the completed form and any confirmation page or transmission record.

This part isn't glamorous, but it's where careful applicants separate themselves from rushed ones.

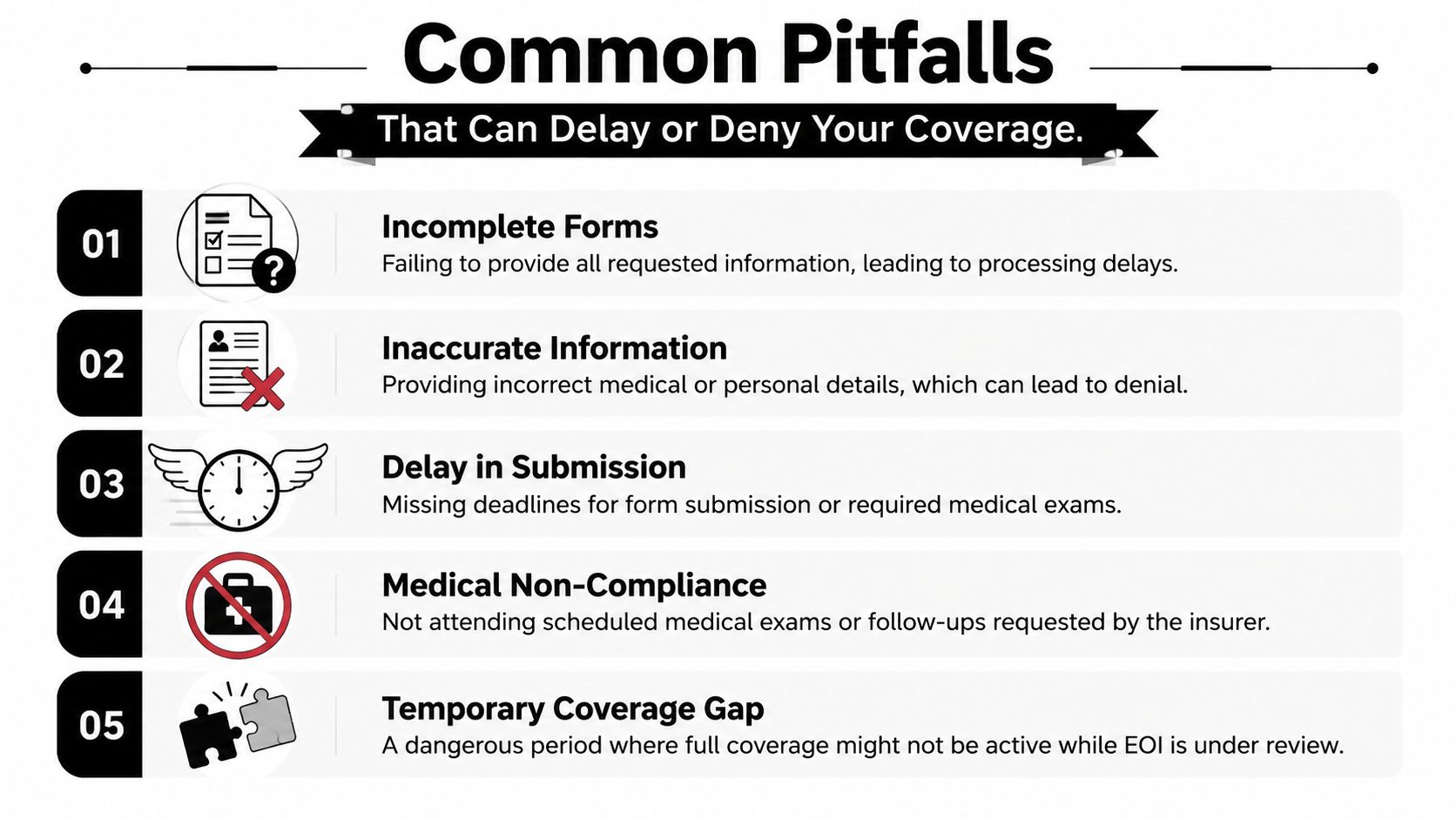

Common Pitfalls That Can Delay or Deny Your Coverage

Many people make the same mistake at the start. They treat the EOI as an administrative chore instead of an underwriting event. That one misunderstanding leads to several others.

The temporary coverage gap

One of the least understood risks is the temporary coverage gap between what you requested and what is active.

MetLife notes that applicants may remain enrolled only up to the Guaranteed Issue amount while the EOI is pending, and that this process takes about 30 business days, creating a potential coverage cliff if the request is denied, as described in MetLife's EOI guidance.

That matters more than it sounds.

If you elected a higher amount because your family depends on it, you may assume the full amount started immediately. In some plans, that isn't true. You may only have the lower automatic amount until the insurer formally approves the extra coverage.

Many applicants think “enrolled” means “fully approved.” In EOI situations, those are not always the same thing.

That's the hidden pitfall many guides skip. It's especially important for newly married couples, young parents, and business professionals with larger financial obligations.

The symptom reporting problem

Another area that causes real confusion is how to answer questions about symptoms that don't yet have a formal diagnosis.

People often think, “If my doctor hasn't named it, I don't need to mention it.” But many forms don't ask only about diagnosed conditions. They may ask about symptoms, consultations, follow-up testing, or pending evaluations. If you've had persistent fatigue, chest discomfort, unexplained weight changes, or another ongoing concern that led to medical attention, read the wording carefully.

The safest approach is not to self-edit the question. Answer what the form asks, even if the medical picture still feels unresolved.

Small mistakes that create big delays

Some problems are dramatic. Others are ordinary and still costly.

Here's where delays often start:

- Missing signatures: A completed form that isn't signed can sit in limbo.

- Old doctor information: If the insurer can't identify your current provider, records requests can stall.

- Incomplete medication details: Partial answers invite follow-up.

- Skipped lifestyle questions: If the form asks about tobacco, alcohol, or hazardous activities, blank spaces can stop processing.

- Wrong submission method: Some carriers accept secure portals, while others still require fax or mail.

A county benefits instruction page also notes that complete contact information and a fully completed form help avoid hold-ups, while missing sections can delay or block review.

Here's a quick checklist worth using before you submit:

| Checkpoint | Why it matters |

|---|---|

| Signature and date | Confirms the form is valid for review |

| Current doctor details | Helps the insurer verify records efficiently |

| Full medication list | Reduces follow-up questions |

| Clear answers on symptoms and history | Prevents inconsistency problems later |

| Copy of submission | Gives you proof if paperwork goes missing |

The broad lesson is simple. Most EOI trouble doesn't begin with a dramatic medical issue. It begins with assumptions, omissions, and rushed answers.

The Underwriting Process After You Submit

Submitting the form starts the quiet part of the process. This is when underwriters review your answers, compare them against what the insurer needs to know, and decide whether the additional coverage should move forward.

What underwriters do with your form

Underwriters are risk reviewers. They don't just scan for yes-or-no answers. They look for consistency, completeness, and anything that needs confirmation.

That may include:

- Reviewing your health questionnaire

- Checking physician information

- Requesting medical records

- Asking for additional exams or lab work in some cases

- Confirming the amount of coverage requested

A county benefits resource states that 90% of EOI applications are processed within 4 to 6 weeks when the applicant provides complete contact information for their primary health practitioner and there are no unresolved discrepancies, according to its EOI form instructions-form-instructions).

If you want a broader explanation of how insurers assess risk after an application is filed, this overview of underwriting for life insurance is useful background.

The underwriter's job is not to punish honest applicants. It's to decide whether the requested risk fits the insurer's rules.

Possible outcomes

The final decision usually lands in one of three buckets.

First, the insurer may approve the coverage as requested. That's the cleanest result.

Second, it may approve with changes. That could mean a different premium or a different approved amount, depending on the policy and underwriting outcome.

Third, it may decline the additional coverage. If that happens, the basic guaranteed amount under the employer plan may still remain in place, depending on the plan design.

Waiting is often the hardest part. The best way to make the process smoother is to submit a complete, signed, accurate form and respond quickly if the insurer asks for follow-up information.

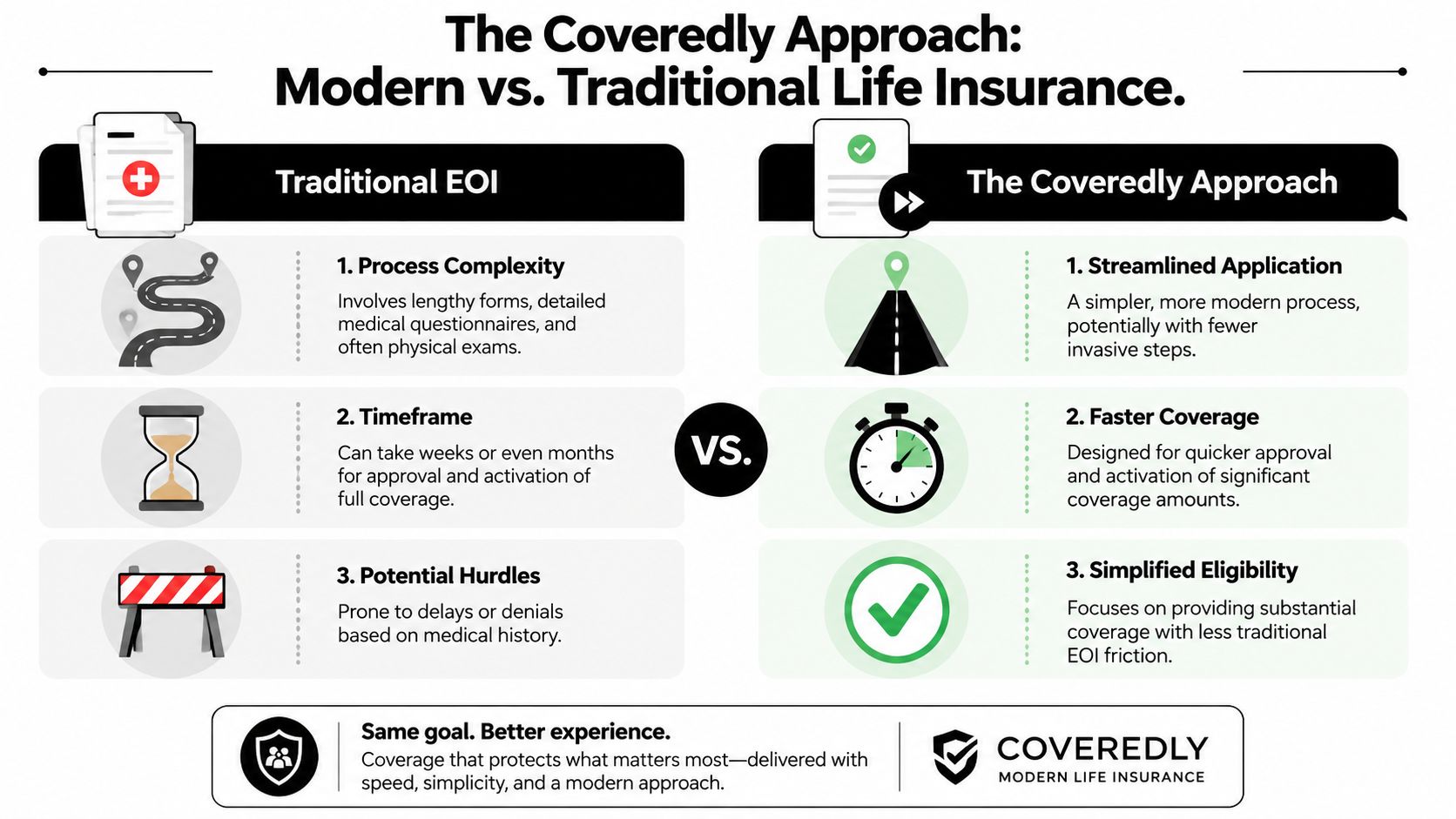

The Coveredly Approach to Getting Life Insurance

Traditional EOI-based coverage can work, but it often asks people to go through forms, deadlines, medical disclosures, and a waiting period that may last weeks. That's a lot to carry when you're already juggling work, family, and financial planning.

Some applicants want a simpler path. That's where a modern digital application model stands out. Coveredly offers online life insurance with up to $3 million of term life insurance with no exams for most, built for people who want speed and less paperwork.

Instead of the traditional employer-benefits route, some people choose a policy that isn't tied to a workplace EOI workflow at all. That can be especially appealing if you want control over your own coverage rather than waiting on an employer plan's rules, enrollment windows, or underwriting sequence.

A simpler application can also make it easier to compare options while your needs are changing. Newly married couples, growing families, and business professionals often care less about insurance jargon and more about one thing: getting meaningful coverage in place without unnecessary friction.

If you're exploring alternatives to the paper-heavy process, it's worth understanding how simplified issue life insurance differs from traditional employer-plan underwriting.

If you'd rather skip much of the traditional Evidence of Insurability process, Coveredly offers a faster online way to apply for life insurance, with up to $3 million of term coverage and no exams for most applicants. It's designed to be digital, flexible, and easier to fit into real life.