Your budget looked stable when you bought permanent life insurance. Then life changed.

Maybe one income dropped. Maybe your business had a rough stretch. Maybe daycare, a mortgage, or higher monthly costs pushed a once-manageable premium into the “not right now” category. That’s where many people discover something they never paid much attention to when they first signed the policy paperwork.

Some permanent life insurance policies have built-in fallback features for moments like this. One of them is extended term life insurance.

It’s not a separate policy you shop for on its own. It’s usually a feature inside a permanent policy, such as whole life or universal life, that can keep a death benefit in place after you stop paying premiums. For a family under pressure, that can feel like a lifeline. For someone who doesn’t understand the trade-offs, it can also become an expensive misunderstanding.

People often get confused because the name sounds simple, but the mechanics aren’t. Are you still covered? For how long? Do you lose the cash value? Can you reverse it later? Does it make more sense than other options?

Those are the right questions.

Extended term life insurance is most relevant when money is tight and financial consequences are significant. If someone depends on your income, you need clarity, not policy jargon. The key consideration isn’t just whether this option exists. It’s whether using it helps your family or creates an unforeseen problem later.

Table of Contents

- Introduction When Your Financial Plans Change

- Understanding Extended Term as a Nonforfeiture Option

- How Your Coverage Period Is Calculated

- Weighing the Pros and Cons of Extended Term

- Comparing Extended Term to Your Other Options

- How to Make the Right Coverage Decision

Introduction When Your Financial Plans Change

A common version of this story starts with good intentions.

A couple buys permanent life insurance when their first child is born. They like the idea of lifetime coverage and cash value. The premium fits the budget at the time. A few years later, one parent cuts back work hours, the mortgage payment feels heavier, and every recurring bill gets reviewed.

Life insurance suddenly lands in the “can we lower this?” pile.

That moment creates a hard choice. You want to protect your family, but you also need breathing room in your monthly cash flow. Canceling coverage outright can feel reckless. Keeping a premium you can’t comfortably afford can feel just as risky.

Extended term life insurance comes into the conversation.

It’s one of those insurance features people rarely think about until they need it. If your permanent policy has built cash value, the insurer may let you use that value to keep coverage active for a limited time without paying more premiums. The attraction is obvious. You keep the death benefit protection for a while, even if the original policy is no longer affordable.

You’re not buying something new. You’re changing how the value inside an existing permanent policy gets used.

That distinction matters.

For a parent with children at home or a homeowner still carrying a mortgage, temporary protection can be exactly what keeps the financial plan from unraveling. But extended term life insurance also involves a serious trade. You’re usually turning a long-term policy into time-limited coverage, and that shift can’t always be undone.

People tend to assume all “keeping coverage” options are roughly the same. They aren’t. Some protect lifetime coverage with a smaller death benefit. Some borrow against the policy. Some preserve the full death benefit for a shorter period. And some families avoid this whole decision by choosing straightforward term life from the beginning.

The only good way to evaluate extended term is to understand what it is before you ever need to use it.

Understanding Extended Term as a Nonforfeiture Option

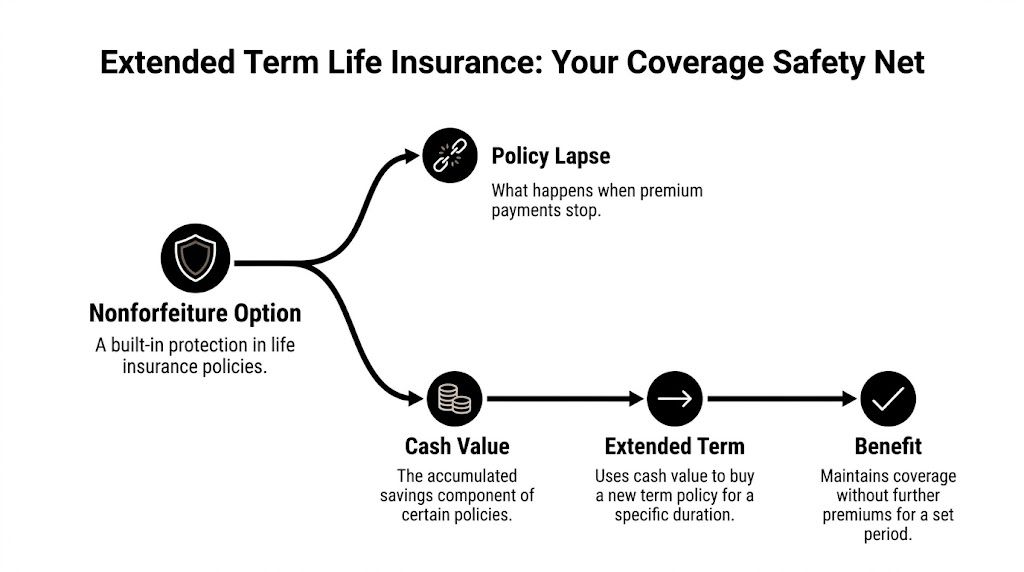

Extended term life insurance is a nonforfeiture option inside certain permanent life insurance policies. In plain English, that means you don’t necessarily lose everything if you stop paying premiums on a policy that has built cash value.

What happens instead is more specific. The insurer takes the policy’s accumulated cash value and uses it as a single prepaid amount to buy term coverage with the same death benefit, and you don’t pay further premiums. That summary aligns with the explanation in The Insurance Pro Blog’s overview of extended term insurance.

What nonforfeiture really means

The word sounds technical because it is. But the idea is simple.

You paid into a permanent policy. Part of those payments built cash value. A nonforfeiture option is the rule that says you may be able to use that accumulated value instead of walking away with nothing when premium payments stop.

With extended term, the cash value doesn’t stay in the policy as an ongoing savings component. It gets redirected. The value is used to keep the death benefit in force for a limited period.

That’s why this is not the same as ordinary term insurance you buy fresh from the market. It’s a rescue feature inside permanent insurance.

If you’ve ever wondered whether there’s such a thing as “cash value term life insurance,” the answer is that term insurance and cash value are usually different concepts. This guide on cash value term life insurance helps clarify that distinction.

A simple way to picture the trade-off

Think of a car you own that has equity in it.

You could sell or trade it in and use that equity to prepay a lease for a while. You’d still have a car to drive, and you might not have monthly payments for a period. But you gave up ownership, future equity growth, and some flexibility.

Extended term life insurance works a lot like that.

You keep coverage for a while. You stop making premium payments. But you’ve changed the nature of what you own.

Here’s the heart of the trade:

- You keep the same death benefit for a period of time.

- You stop paying premiums after the conversion.

- You give up the ongoing permanent policy structure, including future cash value growth.

- You usually can’t treat it like a pause button and return to the original setup later.

Practical rule: Extended term is often helpful when cash flow is the immediate problem and preserving the full death benefit matters more than preserving the policy’s long-term features.

Another point catches many people off guard. Extended term can be the default outcome if a permanent policy lapses after the grace period, depending on the policy terms. That means some policyholders slide into it without making a fully informed decision first.

That’s why this feature deserves attention even if you’re not planning to use it today.

How Your Coverage Period Is Calculated

A policyholder stops paying into a permanent life insurance policy and expects the built-up value to carry the same protection for years. Then the insurer’s illustration arrives, and the coverage period is much shorter than expected.

That surprise happens because extended term is priced, not guessed.

The insurer is taking the value inside your permanent policy and using it to buy a limited amount of term insurance. The question is not, “How much cash value do I have?” Rather, it is, “How much temporary coverage can that amount purchase for someone in my situation?”

Several inputs shape that answer:

Your age at the time of the switch

Age affects the cost of term insurance. In simple terms, the older the insured person is, the more expensive each year of coverage becomes. That usually means the same pool of policy value buys fewer years.How much cash value is available

More available value usually means more buying power. But “more” does not always translate into dramatically more time if the death benefit is large or the insured is older.The size of the death benefit

Keeping a larger face amount in place costs more than keeping a smaller one. If your policy has a high death benefit, the value inside it may be used up faster.Your original underwriting class

The insurer still looks at the policy’s pricing foundation. A policy issued at a more favorable health rating may stretch further than one issued at a less favorable rating.The insurer’s policy assumptions and contract terms

Insurers use the rules built into the policy to calculate the nonforfeiture value and the resulting term period. Two policies with similar cash value can still produce different results.

A grocery budget works as a useful comparison. One family can stretch $200 for a week by buying basics. Another family spends the same $200 quickly because they are buying more items, more expensive items, or both. Extended term works the same way. Your cash value is the budget, and your age, death benefit, and policy terms determine how fast that budget gets spent.

Age often creates the biggest misunderstanding.

A younger policyholder may get a meaningfully longer extended term period from the same amount of value than an older policyholder with the same death benefit. That does not mean the insurer is being inconsistent. It means the cost of providing that term coverage has changed.

That is why estimates from friends, online examples, or even your own older policy statements can mislead you. The actual answer comes from the insurer’s current illustration under your policy’s terms.

A few practical questions help bring the math back to real life:

- Will the extended period last through your highest-responsibility years?

- Does it cover the years your children still rely on your income?

- Will it stay in force long enough to protect a spouse until major debts are reduced?

- If the term ends sooner than expected, what is your backup plan?

Those questions matter because extended term can feel simpler than it really is. You stop paying premiums, but you also step into a countdown with an end date set by policy math.

For many families, that complexity is the clearest lesson. Permanent life insurance can offer fallback options, but those options come with calculations, trade-offs, and timing risk. Starting with a modern term life policy is often easier to match to a specific goal, such as covering a mortgage, replacing income while children are young, or protecting a fixed number of years of financial obligation.

Weighing the Pros and Cons of Extended Term

A common real-life scenario looks like this. A parent bought permanent life insurance years ago, premiums have become harder to manage, and the family still needs protection. Extended term can keep coverage in place for a while, but it changes what kind of policy you have and how long that protection lasts.

That trade-off is the whole decision.

Where extended term helps

The biggest benefit is cash-flow relief without making your family uninsured overnight.

If premiums on a permanent policy no longer fit the budget, extended term may let you keep the full death benefit for a limited time with no new premium payments. For a household under pressure, that can buy time during years when a spouse, children, or a mortgage still depend on your income.

It can also help if your health has changed. Because the option comes from your existing policy, you usually do not have to qualify all over again through new medical underwriting.

That makes extended term most useful in a narrow set of situations. The need for coverage is still real, the budget is strained, and the family mainly needs protection for a remaining stretch of years rather than for life.

A good way to picture it is as using the policy’s stored value to prepay a temporary insurance period. You are not keeping the whole permanent policy intact. You are converting what is left inside it into a clock that runs for a fixed time.

What you give up

The cost of that short-term relief is future flexibility.

Once extended term begins, cash value growth usually stops because the policy is no longer operating as permanent coverage in the same way. The policy also loses the open-ended duration that made it permanent in the first place. When the extended period ends, coverage ends.

That creates a practical risk for families who still need insurance later. Buying new coverage at an older age is often harder and more expensive. If health has worsened, your options may also be narrower. That is one reason families often want to understand what happens when term life insurance expires before choosing any path that converts lifelong coverage into temporary coverage.

There is also a commitment problem. As noted earlier from PHP Agency’s discussion of underserved life insurance markets, extended term is generally irreversible once elected, state rules can affect how it works, and some policies with premium waiver features may preserve protection longer during a disability. Those details matter because a decision made during financial stress can permanently reshape the policy.

That is why extended term often works more like an exit ramp than a pause button.

A balanced view

| Upside | Why it matters |

|---|---|

| Keeps the full death benefit for a limited time | Your family may stay protected during a financially difficult period |

| No further premiums during the extended period | Monthly budget pressure eases |

| Usually no new underwriting | Health changes may not block continued coverage |

| Trade-off | Why it hurts |

|---|---|

| Coverage becomes temporary | Protection may end while your family still needs it |

| Cash value growth stops | A long-term policy feature is lost |

| The choice is often irreversible | You may not be able to return to the original policy structure |

For some households, extended term is the least disruptive way to protect loved ones after permanent premiums become unaffordable. But it is rarely the cleanest long-term solution.

That is the broader lesson. Permanent life insurance can include fallback options, but those options come with rules, calculations, and one-way choices. Starting with a modern term life policy is often simpler because the policy is already built around a defined need and a defined time frame, without asking you to convert a permanent contract later just to make the budget work.

Comparing Extended Term to Your Other Options

When a permanent policy becomes hard to afford, extended term isn’t the only path. That’s why decisions go wrong when people ask only one question: “Can I stop paying and still stay covered?”

The better question is: Which option preserves what I care about most?

How the main alternatives differ

Each alternative solves a different problem.

Extended term insurance preserves the original death benefit for a limited period.

Reduced paid-up insurance usually lowers the death benefit but keeps some permanent coverage in force.

Policy loans may help with short-term cash needs while keeping the policy active, but they introduce debt against the policy.

Buying standalone term is the proactive path many families prefer when they want straightforward, temporary protection without permanent policy complexity.

Here’s a side-by-side comparison.

Comparing Your Policy Options During Financial Strain

| Feature | Extended Term Insurance | Reduced Paid-Up Insurance | Policy Loan | Buying Standalone Term |

|---|---|---|---|---|

| Premiums | No further premiums for the extended period | Typically no further premiums on the reduced policy | Original policy may stay active, but loan obligations matter | New premiums apply |

| Death benefit | Usually keeps the same death benefit for a limited time | Death benefit is reduced | Original death benefit may be affected if loan balance grows | Based on the new policy you buy |

| Coverage duration | Temporary | Permanent, but smaller | Depends on policy performance and loan management | Temporary, based on term selected |

| Cash value | Used up to buy term coverage | Converted into a smaller paid-up permanent benefit | Cash value remains part of the policy structure, but loan reduces net value | No cash value in standard term |

A lot of confusion clears up once you decide which of these matters most:

- Need the full death benefit right now? Extended term may fit.

- Need lifelong coverage, even if it’s smaller? Reduced paid-up may deserve attention.

- Need flexibility and can manage the policy carefully? A loan may be worth discussing.

- Need affordable income protection during working years? Standalone term is often the cleanest solution.

Why many families prefer simple term coverage upfront

For many households, the appeal of term life is that it avoids this decision tree from the start.

The Ohio State summary of 2022 Federal Reserve data found that households with both term and permanent life insurance were 5.58 times more likely to be financially adequate after an earner’s death than uninsured households. The same report notes that term policies made up 39.3% of all new life insurance policies sold in 2022 (Ohio State summary of the Federal Reserve data and policy sales trends).

That doesn’t mean everyone needs both. It does show two things clearly. Families use term insurance heavily, and term often plays the affordable protection role during high-need years.

For younger couples, parents, and professionals, that’s usually their primary objective. They want enough coverage while incomes are being built, children are dependent, and debts are largest. They don’t necessarily want a policy that later forces a complicated nonforfeiture decision.

If you’re thinking about what happens at the end of a temporary policy, this explanation of what happens when term life insurance expires is worth understanding before you buy.

A simple policy isn’t “less serious.” It’s often better matched to a temporary financial risk.

That’s the strongest argument for modern term life from the outset. It’s easier to understand, easier to budget for, and less likely to corner you into a technical fallback option years later.

How to Make the Right Coverage Decision

A good coverage decision should still make sense on an ordinary Tuesday night, when you are looking at your budget, your mortgage, and the people who count on your income.

That is the true test.

If you already own a permanent policy, the question is whether extended term solves a temporary problem without creating a larger one later. If you are still shopping, the question is simpler. Do you need a policy with fallback mechanics built into it, or do you need straightforward protection for a defined stretch of life?

If you already own a permanent policy

Start with current policy information, not your memory of how the policy was sold. Permanent life insurance can change over time, and the nonforfeiture options available today may look different from what you expected years ago.

Ask the insurer for an in-force illustration and written details on each available option. Then ask these questions:

- How long would extended term coverage last if I elect it now?

- Would the death benefit remain level for that full period?

- What happens to the cash value once I make this election?

- Can I reverse the decision later, or is it permanent?

- What other options are available, such as reduced paid-up insurance or a policy loan?

- Are there state-specific rules or policy provisions that affect the result?

Then compare the answer to the job the policy still needs to do.

A simple way to frame it is this. Extended term works like using the policy’s built-up value to prepay a limited period of pure life insurance. That can help if your need is temporary, such as covering the remaining years of a mortgage or getting children closer to financial independence. It is less attractive if your family would still need protection long after that extended period ends.

A frequent error occurs for many policyowners. They focus on the fact that premiums may stop, which feels like relief in the moment. But the larger question is whether the coverage lasts long enough to protect the people you bought insurance for in the first place.

Use a short decision check:

Match the coverage period to the risk

Does the extended coverage line up with the years your family is exposed to a specific obligation, such as a mortgage, tuition support, or a business loan?Be honest about replacement options later

If this extended coverage expires, would your age, health, or budget make new insurance hard to get?Review the alternatives before you elect it

In some cases, another policy feature may solve the problem with less long-term tradeoff.Separate premium stress from insurance need

A policy can feel expensive and still be solving an important family risk. Those are two different questions.

Extended term can be a useful temporary fix. It is not a substitute for a long-term plan.

If you are comparing policy types more broadly, this guide to converting term life to whole life can help clarify how different policy designs fit different goals.

If you’re shopping for coverage now

For many families, this is the cleaner lesson from the whole extended-term discussion. Complexity often enters the picture because the original policy was designed to do many jobs at once.

Young parents, newly married couples, and busy professionals usually have a more specific goal. They want income protection during the years when the financial stakes are highest. That often means the child-raising years, the mortgage years, or the period when one income loss would seriously disrupt the household plan.

Term life is built for that job. You choose a coverage amount. You choose a time period. You protect the years that matter most.

That simplicity matters more than it sounds. A permanent policy with a nonforfeiture option can be helpful, but it also asks you to manage moving parts years later. A modern term policy starts with a clearer agreement. Protection lasts for the period you selected, and you are not relying on future cash value decisions to keep the plan on track.

A useful shopping filter looks like this:

Choose term when the risk has a deadline.

Raising children, paying down a mortgage, and replacing income during peak working years all have a time horizon.Choose affordability that you can keep.

Coverage that fits your budget year after year usually protects your family better than a more complicated design that becomes hard to maintain.Choose clarity your spouse or partner can understand quickly.

If the policy only makes sense after a long explanation about internal features, it may be more complicated than your situation requires.

The best coverage decision is often the one that matches your real-life need with the fewest moving parts.

Extended term has a place inside permanent life insurance. But for many households, its existence points to a broader truth. If your need is temporary, buying straightforward term life from the start is often the more flexible and easier path. It protects the years that matter, keeps the budget easier to manage, and reduces the chance that you will face a technical policy decision later when life is already busy.

If you want life insurance built for real household needs rather than policy mechanics, Coveredly offers a digital, flexible way to shop for term coverage that fits young families, newly married couples, and busy professionals.