You may be reading this after a late-night search, with a child asleep in the next room, a mortgage in your name, or a new spouse who depends on your income. You want life insurance, but a bigger question is sitting underneath it: Can I get covered if I'm living with HIV, and who will find out if I apply?

That fear is common. For years, hiv life insurance felt either unavailable or practically out of reach. Many people assumed the answer would be an automatic no, or that applying would create privacy risks at work. The good news is that the market looks very different now. Coverage is often possible, especially when HIV is well managed, and the privacy side can be handled more carefully than many people realize.

This guide is for professionals, parents, and partners who want plain-English answers. You'll see how insurers look at HIV today, which policy types make sense, what underwriting really involves, how pricing works, and how to protect your confidentiality while protecting your family.

Table of Contents

- Your Guide to Life Insurance with HIV

- How Insurers View HIV Today

- Decoding Your Life Insurance Options

- The Underwriting Process Step by Step

- Understanding Prices and Improving Your Rate

- Privacy for Professionals and Family Protection

- Frequently Asked Questions

Your Guide to Life Insurance with HIV

A common situation looks like this. Someone has done the hard work. They take ART consistently, keep up with specialist visits, and have built a stable life. Then real adult responsibilities arrive. A baby. A home loan. A business partnership. Suddenly, life insurance stops being abstract.

The first reaction is often emotional, not financial. People living with HIV frequently assume they'll be declined, quoted something impossible, or pushed into a tiny policy that won't really protect anyone. That assumption made sense in an earlier era. It doesn't reflect the full picture anymore.

Today, hiv life insurance is less about the label on your chart and more about the story your medical records tell. Insurers still look carefully at HIV. They haven't become casual about it. But many now evaluate whether the condition is stable, documented, and well managed over time.

The practical question usually isn't just “Can I get covered?” It's “Which path gives me enough coverage, at a workable price, without creating unnecessary stress or disclosure?”

That distinction matters. You may have more than one route to coverage. One route might offer better value. Another might offer faster approval. A third might be useful if privacy at work is part of your concern.

For families, the point of life insurance is simple. It replaces stability when a person can't. It can help cover rent or a mortgage, child-related expenses, debts, or the financial gap created when income disappears. For professionals, it can also protect business plans, co-signed obligations, or future goals that depend on your earning power.

You don't need to know every insurance term before applying. You do need to understand a few key ideas. Once those are clear, the process becomes much less intimidating.

How Insurers View HIV Today

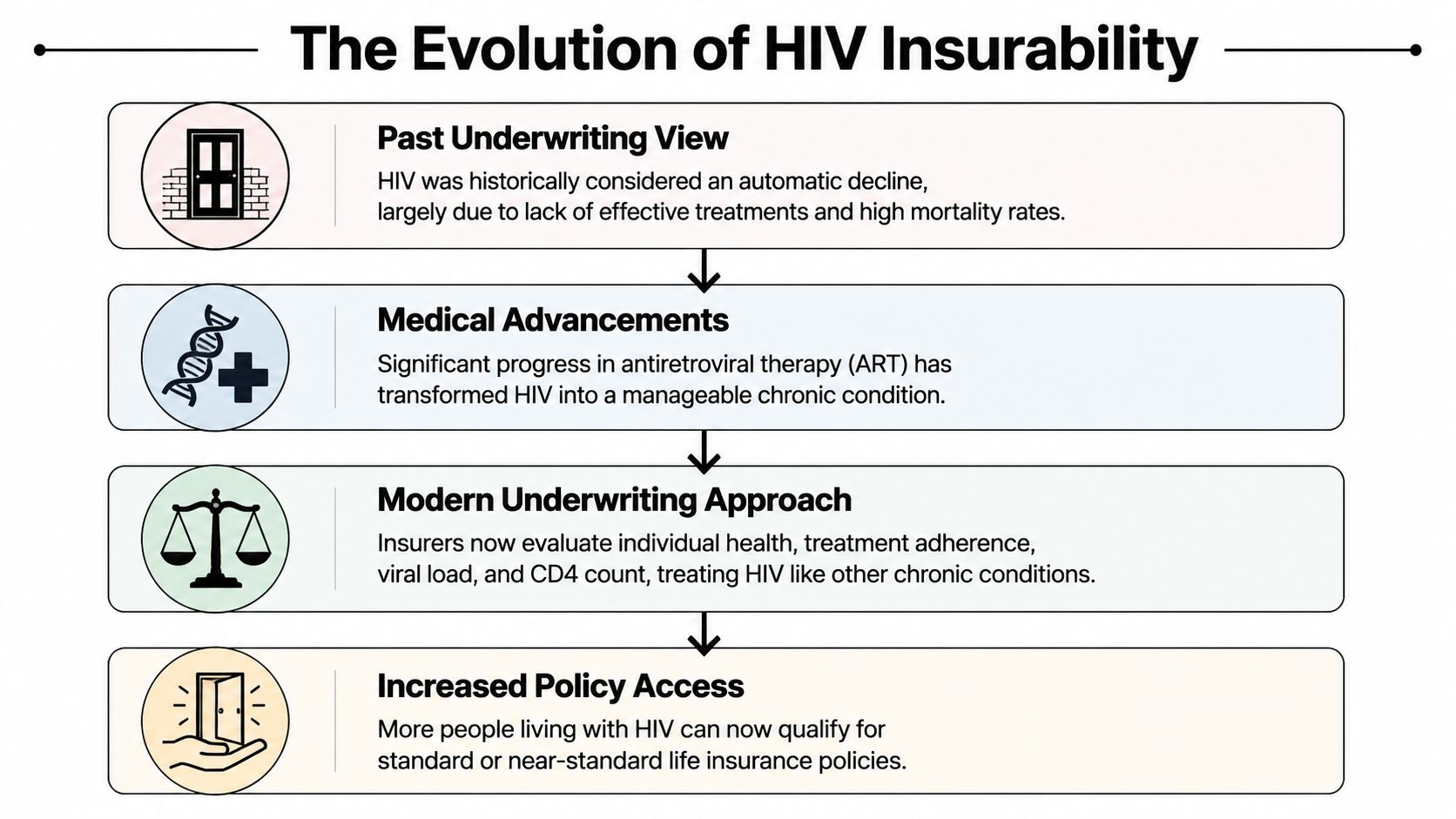

From automatic declines to measured underwriting

Insurers used to treat HIV as a near-certain decline in many cases. That history still shapes how people talk about hiv life insurance today. But the underwriting model has changed in meaningful ways.

A major market signal comes from Swiss Re's Life Guide. Through 2025, 370 companies across 76 countries used the platform to underwrite individuals living with HIV, as noted by Insuranceopedia's review of life insurance for HIV-positive applicants. That doesn't mean every insurer will approve every applicant. It does mean HIV is no longer confined to niche insurance conversations.

A useful way to think about it is how insurers look at other chronic conditions. With something like diabetes, the diagnosis matters, but control matters more. Underwriters ask whether the person is managing the condition, following treatment, and avoiding serious complications. HIV underwriting increasingly works the same way.

That's why many modern applications focus on stability, not just status.

The health markers underwriters care about

Most insurers want to see a pattern they can trust. The details vary by carrier, but market guidance commonly points to several core factors:

- Viral load control: An undetectable or controlled viral load helps show treatment is working.

- CD4 count strength: A stable, healthy CD4 picture gives underwriters more confidence in overall immune status.

- Consistent ART use: Many market guides say eligibility often depends on sustained antiretroviral therapy, often for at least 1 to 2 years, along with adherence and specialist follow-up, as summarized in Abrams' guide to life insurance with HIV.

- Age and co-morbidities: Underwriters also look at the broader health picture, not HIV in isolation.

Here's the plain-language version. Underwriters are trying to answer one question: How predictable is this applicant's future health risk? Stable treatment and consistent records reduce uncertainty.

Practical rule: Your lab trends and treatment history matter more than a single sentence saying you have HIV.

That's why two people with the same diagnosis can get very different outcomes. One applicant may qualify for mainstream coverage because their records show long-term control and regular follow-up. Another may be offered fewer options because the records show recent treatment changes, interruptions in care, or other medical complications.

If you've been assuming that HIV automatically blocks life insurance, that's the old model talking. The current model is stricter than average underwriting, but it's much more individualized.

Decoding Your Life Insurance Options

The right hiv life insurance policy depends on two things at once. First, how comfortable an insurer is with your medical profile. Second, how much coverage you need.

Fully underwritten term life

This is usually the best-value option for applicants who can qualify. It involves the deepest review of your health history, but that extra scrutiny can work in your favor if your HIV is well controlled.

Guardian says qualified HIV-positive applicants may be eligible for term coverage from $100,000 up to $10,000,000 and whole life coverage starting at $25,000 and going up to $10,000,000, as discussed in this mortality and market-access review. That's a strong sign that some carriers now offer substantial face amounts to qualified applicants.

Fully underwritten term life is often best for:

- Parents with larger protection needs: If you need meaningful income replacement, this is usually the first place to look.

- Professionals with debts or long-term obligations: Mortgages, private school plans, and business commitments often require more than a minimal policy.

- Applicants with well-documented stability: Strong records can open the door to better pricing than no-medical alternatives.

Simplified issue life insurance

Simplified issue sits in the middle. You answer health questions, but the process is lighter than full underwriting. This can help if you want an easier application or if your profile may not fit the most competitive fully underwritten programs.

If you want a clearer sense of how this category works, simplified issue life insurance options can help explain the tradeoff between fewer underwriting hurdles and potentially higher cost.

This option often fits people who:

- need coverage sooner,

- want to avoid a more extensive review process,

- or may not qualify for the strongest fully underwritten offers.

A short visual can make these differences easier to grasp.

Guaranteed issue life insurance

Guaranteed issue is the fallback route when other underwriting paths don't work. It generally has the least medical friction, but it usually comes with lower face amounts and a higher per-dollar cost.

This kind of policy can still be valuable. It may help cover final expenses or provide at least some protection when a traditional approval isn't available. It's not usually the first choice for someone trying to protect a young family in a major way, but it can be much better than having no coverage at all.

A quick way to compare them

| Policy type | Best fit | Underwriting depth | Typical value |

|---|---|---|---|

| Fully underwritten term | Stable HIV, larger coverage needs | Highest | Usually the strongest value if approved |

| Simplified issue | Moderate underwriting concerns, wants a faster path | Medium | Easier access, often less competitive pricing |

| Guaranteed issue | Declined elsewhere or needs minimal-question access | Lowest | Broadest access, usually the highest cost for the coverage |

One path isn't morally better than another. It's just about matching the product to your current health profile, budget, and coverage goal.

The Underwriting Process Step by Step

A common fear starts before any lab result is reviewed. A lawyer, physician, executive, or teacher may be less worried about the application itself than about who might see it. That concern is understandable. Individual life insurance underwriting is private, but it is also more detailed, and knowing the steps ahead of time makes the process feel far less mysterious.

What happens after you apply

Underwriting works a bit like assembling a timeline from several folders. The insurer is trying to answer a practical question: does the medical record show stable treatment, regular follow-up, and a clear picture of current health?

A typical process looks like this:

Initial application

You provide basic personal information, the amount of coverage you want, and your health history. Accuracy matters because inconsistencies often trigger follow-up questions. For professionals with privacy concerns, this is also the point to ask your agent exactly how information is collected, who can access it, and whether communications will go to your personal email, work email, or home address.Medical records request

The insurer may order an Attending Physician Statement and records from your doctors. They usually review treatment dates, medication history, viral load trends, CD4 results, and notes about follow-up care. They may also look for other health conditions that affect overall risk.Possible exam or phone interview

Some policies require a brief paramedical exam or a health interview. Some do not. If an exam is needed, you can often schedule it at home or another private location, which matters if you do not want medical paperwork or examiner calls showing up at work.Underwriter review

An underwriter reviews the full file, not just a diagnosis label. This part is closer to reading a long story than checking a single box. Stable records, consistent medication use, and regular specialist care usually make the story easier to follow.Decision

The insurer may approve the policy, approve it at a higher rate, ask for more records, or decline. A request for more information is common. It does not automatically signal a bad outcome.

For a broader explanation of how insurers assess applications, this guide to life insurance underwriting factors and steps can help.

A clear file helps because it reduces uncertainty, not because it needs to show perfect health.

Where privacy questions usually come up

This is the part many articles skip.

With an individual policy, your medical information is reviewed by the insurer, any companies helping process the application, and your authorized medical providers. Your employer does not receive your full underwriting file. If you work in a profession where reputation and confidentiality matter, that distinction can bring real relief.

With a group policy through work, the application is often less detailed, especially for guaranteed issue amounts. That can mean less medical disclosure up front. But if you apply for supplemental coverage above the no-questions limit, you may need to complete evidence of insurability forms, and people often worry about paperwork flowing through workplace systems. The employer typically does not see your detailed diagnosis records, but the concern feels personal because the coverage is tied to your job.

A simple rule helps here. Individual underwriting usually asks more medical questions, but keeps the process more clearly separated from your workplace. Group coverage may feel easier at first, but privacy can feel less direct because the policy sits inside an employee benefit structure.

What to gather before underwriting starts

Preparation helps for two reasons. It shortens delays, and it gives you more control over what the underwriter sees first.

Try to gather:

- Diagnosis timeline: Your diagnosis date and major treatment milestones

- Medication list: Your current ART regimen and how long you have taken it

- Recent lab results: Viral load and CD4 history that shows patterns over time

- Doctor contact details: Your infectious disease specialist and primary care physician

- Other medical history: Any coexisting conditions, hospitalizations, or specialist follow-up

- Preferred contact method: The safest phone number, mailing address, and email for insurer communication

Scattered records create problems even for applicants with stable health. A missing specialist note can slow a case more than an unfavorable fact that is already documented and explained.

If privacy matters strongly in your household or profession, tell your agent early. Ask them not to leave voicemail details, not to mail documents to an office, and not to copy anyone you have not authorized. Small requests like these can make the process feel much safer.

Start requesting your own records before you apply if your care has been split across different clinics or health systems.

That step gives you a preview of what the insurer is likely to review, and it replaces some of the fear of the unknown with a checklist you can control.

Understanding Prices and Improving Your Rate

Price is where many applicants feel the most tension. You may be asking two questions at once: What will this cost, and who will need to know why it costs that amount?

The cost question usually comes down to how an insurer classifies risk. With hiv life insurance, carriers often use table ratings or another form of premium increase. A simple comparison helps here. It works a lot like mortgage pricing. Two people may apply for the same loan, but the borrower with a stronger file usually gets better terms. In life insurance, a stronger file means clearer evidence that your health is stable and well managed.

That also explains why rates can vary so much from one insurer to another. One company may look at the same medical facts and feel comfortable. Another may price more cautiously, ask for more records, or decline the case. The difference is not just your diagnosis. It is how much uncertainty the underwriter sees in the full picture.

A better rate usually comes from making your file easier to understand.

Insurers tend to respond well to applicants who can show a consistent pattern over time, not just one good lab result right before applying. If your records show steady treatment, regular follow-up, and no major gaps, the underwriter has fewer unanswered questions. Fewer unanswered questions can mean a better offer.

Several factors often help:

- Stable treatment history: A longer record of adherence to ART can support a stronger application.

- Recent, consistent lab trends: Underwriters usually prefer patterns over time instead of isolated results.

- Regular specialist care: Ongoing follow-up shows the condition is being monitored carefully.

- Non-smoking status: Tobacco use can raise premiums on its own.

- Control of other health issues: Blood pressure, cholesterol, diabetes, and hepatitis coinfection can affect pricing.

- Applying through the right carrier: Some insurers are more experienced with HIV cases than others.

If you are a physician, attorney, executive, or anyone in a role where privacy feels especially sensitive, rate shopping should be handled carefully. Every formal application creates a record. Asking an experienced broker to start with informal inquiries can help you compare likely outcomes before you decide where to submit full medical details. That does not remove underwriting, but it can reduce unnecessary disclosure and avoid applications with carriers that were unlikely to offer good terms in the first place.

Timing matters too. If your treatment has changed recently, or your records do not yet show a stable pattern, waiting may improve the result. Many applicants benefit from pausing a few months, gathering updated labs, and applying with a cleaner file instead of rushing into a price that reflects uncertainty more than actual day to day health.

It also helps to look beyond the base premium. Some policies include features that matter for family protection later, such as an accelerated death benefit rider for early access to benefits. A slightly higher premium can still be reasonable if the policy better fits the actual financial risks your family would face.

The first offer is not always the last word. If your health history becomes more established, you may be able to revisit coverage later and ask whether a better rate is possible. That approach gives you a practical path: secure protection now if you need it, then improve the file and reassess when the timing is better.

Privacy for Professionals and Family Protection

For many readers, the hardest part of hiv life insurance isn't the underwriting. It's the fear of disclosure. You may be less worried about answering medical questions than about who sees the answers.

Group coverage through work

Employer group life insurance can be helpful because enrollment is often easier than buying an individual policy. In some cases, a medical questionnaire isn't required. That can make group coverage one of the few simple routes to at least some protection.

But group plans can raise understandable privacy questions. Aidsmap notes that when a medical questionnaire is required, applicants can often ask to submit it directly to the insurer in confidence rather than through the employer, as explained in Aidsmap's guide to life insurance for people living with HIV.

That's an important safeguard. Still, group coverage has practical limits. It may not be portable if you change jobs. Coverage amounts may be modest. And the plan structure is controlled by the employer, not by you.

Individual coverage and control

An individual policy usually gives you more control over both privacy and long-term planning. You deal directly with the insurer or broker. Your coverage can stay with you if you leave a job. And the policy can be designed for your family's needs rather than the benefits menu at work.

For parents and professionals, that portability matters. If your income supports children, a partner, or a business, losing coverage when changing employers can create a real gap.

Some people also want features that can support family planning if health changes later. An accelerated benefit rider is one example of a policy feature worth understanding when reviewing options.

Privacy isn't only about who knows today. It's also about how much control you keep if your career changes next year.

How to think about privacy and portability

A simple comparison helps.

| Consideration | Group life through employer | Individual policy |

|---|---|---|

| Enrollment ease | Often easier | Usually more involved |

| Privacy handling | May involve employer plan processes, though confidential submission may be possible | Generally handled directly with insurer or broker |

| Portability | Often tied to your job | Usually stays with you |

| Customization | Limited by plan design | More tailored to your needs |

If confidentiality is your top concern, don't assume all roads lead through your employer. If convenience is your top concern, don't dismiss group coverage either. The best answer may be to use both, with clear eyes about what each one does well.

Frequently Asked Questions

Some questions stick around even after you understand the basics. These are usually the ones that carry the most anxiety.

Common Questions on HIV Life Insurance

The broader market has shifted from exclusion toward risk-tiering. Fully underwritten term life is often the best value for qualified applicants, while simplified and guaranteed issue products can still create access for others. Reinsurers such as Munich Re and Swiss Re have formalized guidelines that treat well-managed HIV as a chronic condition when evidence supports stable treatment response, as summarized in Wysh's overview of life insurance for people living with HIV.

| Question | Answer |

|---|---|

| Do I have to tell my employer I'm applying for life insurance with HIV? | Not if you're applying for an individual policy. If you're using employer group life and a questionnaire is required, ask whether you can submit health information directly to the insurer or broker in confidence. |

| Is fully underwritten coverage worth trying first? | Usually, yes, if your HIV is stable and well documented. It often offers the best value and the broadest coverage for qualified applicants. |

| What if I'm declined? | A decline on one application doesn't end the process. Another carrier may view your profile differently, or a simplified issue or guaranteed issue policy may still provide access. |

| What happens if my health changes after the policy is issued? | In general, life insurance is based on the underwriting done at issue. After the policy is active, the key obligation is usually to keep paying premiums and follow the contract terms. Review your policy carefully for any specific conditions or exclusions. |

One more point matters emotionally as much as financially. You don't need a perfect medical story to deserve protection. You need a realistic strategy. For some people that will be a fully underwritten term policy. For others, it will be a smaller or more expensive policy that still gives their family something solid to rely on.

If you've been delaying this because the process felt loaded with stigma, uncertainty, or privacy risk, that hesitation is understandable. It also doesn't have to be permanent.

If you want a simpler way to explore life insurance online, Coveredly offers digital options designed for modern families and professionals. It's built to make coverage more flexible, easier to understand, and less intimidating to start.