You're probably asking a simple question: is life insurance an asset, or just an expense you hope nobody ever uses?

The honest answer is both less confusing and more nuanced than most articles make it sound. Some life insurance policies do build a measurable asset you can list on a balance sheet. Others don't build cash value at all, yet still protect the assets that matter most to a young family, like your income, home equity, emergency fund, and retirement savings.

That distinction matters because life insurance is not a tiny corner of household finance. A Federal Reserve Bank of St. Louis analysis of the U.S. life insurance industry says the sector's asset backing is now large enough to equal a little less than five months of aggregate U.S. personal income, and the same analysis estimates that because about 51% of Americans have life insurance, the average coverage would amount to roughly ten months of income as benefits if paid out across insured households.

If you're a young professional, newly married, raising kids, or building a business, the primary question usually isn't just whether a policy counts as an asset on paper. It's whether it helps your financial life in the way you need help right now.

Table of Contents

- The Billion-Dollar Question Is Life Insurance an Asset

- Term vs Permanent Life Insurance Explained

- How Permanent Life Insurance Becomes a Balance Sheet Asset

- Using Your Policy's Cash Value as a Financial Tool

- Why Term Life Insurance Is a Protective Asset

- Advanced Strategies for Tax and Estate Planning

- Choosing the Right Strategy for Your Financial Goals

The Billion-Dollar Question Is Life Insurance an Asset

Individuals often become confused because they use the word asset in two different ways.

In strict financial terms, an asset is something you own that has current economic value. By that definition, some life insurance qualifies and some doesn't. In practical planning terms, though, people also use “asset” to mean something that protects their financial life from falling apart. That broader meaning is where a lot of the confusion starts.

The short answer

If you own term life insurance, the policy usually isn't a balance sheet asset during your lifetime because it typically doesn't build cash value.

If you own permanent life insurance, the policy may be an asset because it can accumulate cash value you can access while you're alive.

That's the narrow answer. It's accurate, but it's incomplete.

Why this question matters so much

Young families often focus on the wrong thing. They ask whether a policy has cash value before they ask whether their loved ones could stay in the house, keep saving for college, or avoid draining retirement accounts if income disappeared tomorrow.

Key idea: The balance sheet answer and the real-life planning answer are not always the same answer.

A permanent policy can create an asset. A term policy can protect the rest of your assets. Both can matter. They just solve different problems.

A smarter way to think about it

Use two filters:

| Question | What it means |

|---|---|

| Does this policy have present value I can access? | That's the technical asset question. |

| Does this policy protect my income and existing net worth? | That's the practical planning question. |

If you keep those two ideas separate, the whole topic gets easier. You stop comparing every policy as if they all do the same job.

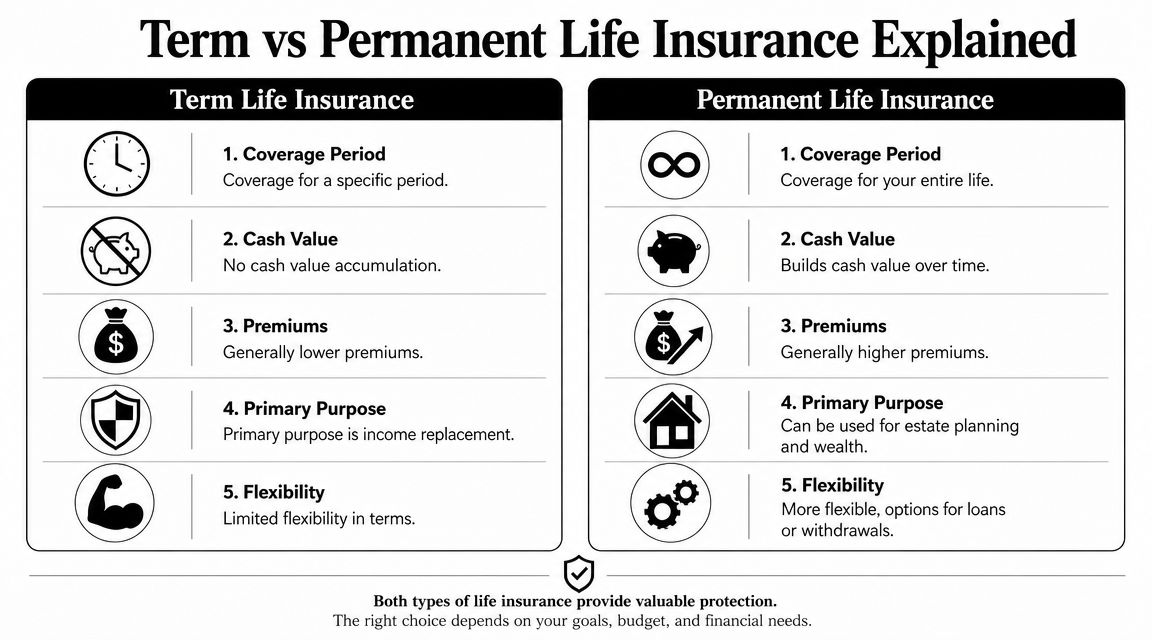

Term vs Permanent Life Insurance Explained

Term and permanent life insurance look similar from far away. You pay premiums. The insurer promises a death benefit. Your beneficiary receives money if you die while the policy is in force.

The big difference is what happens during your lifetime.

Think of it as renting versus owning

Term life insurance is a lot like renting. You pay for protection for a set period. If nothing happens during that term, the coverage ends and there's no built-up value to take with you.

Permanent life insurance is more like owning. It provides lifelong coverage if the policy stays funded as required, and part of the structure can build cash value over time.

If you want a deeper side-by-side breakdown, this guide on term vs whole life insurance is a useful companion.

What term life usually does best

Term life is built for one main job: income replacement.

That makes it a natural fit when your biggest financial risk is straightforward. You've got a mortgage, a partner who relies on your paycheck, kids who still need support, or a business that depends on your work. In that situation, affordable protection often matters more than building value inside the policy.

A typical buyer chooses term because they want coverage that is simple, focused, and easier to fit into a working-family budget.

Here's a quick explainer if you want to see the concepts visually:

What permanent life usually does best

Permanent life is designed to do two jobs at once:

- Provide lifelong coverage if maintained properly

- Build cash value that may be available later through withdrawals, loans, or surrender

That second feature is why people ask whether life insurance is an asset. With permanent coverage, the answer can be yes. But it's yes because of the cash value, not because of the death benefit itself.

Term is mainly protection for a period of time. Permanent insurance combines protection with a long-duration savings feature.

Why people confuse the two

A lot of marketing blurs the line. People hear “life insurance” and assume all policies work the same way. They don't.

One policy is mostly a shield. The other is part shield, part financial tool. Once you understand that split, the rest of the asset discussion falls into place.

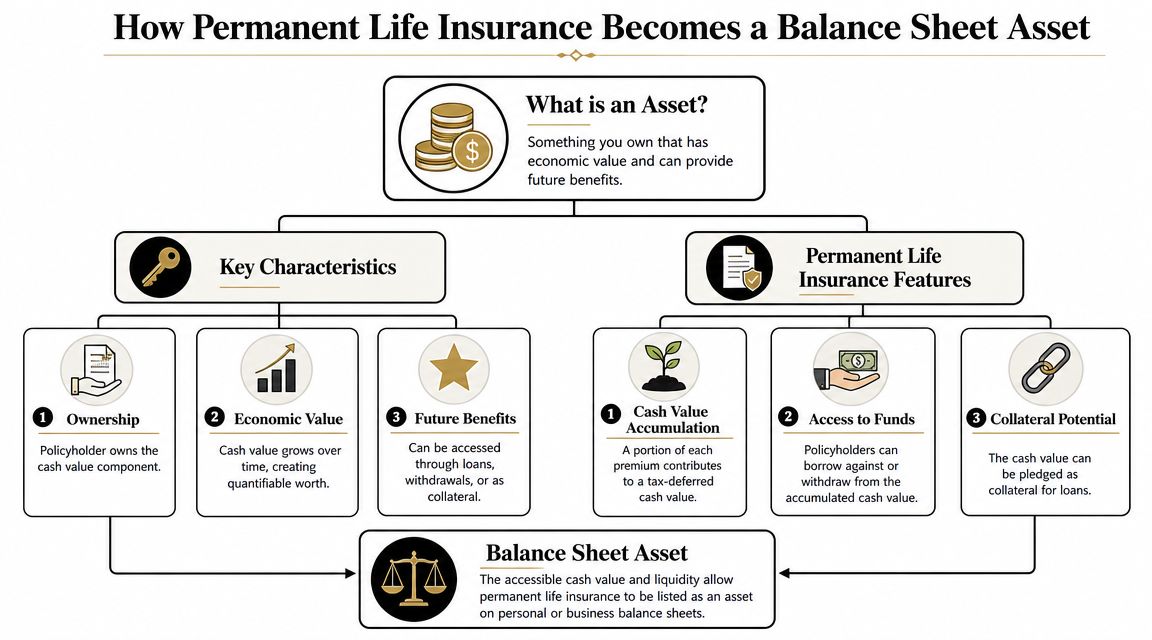

How Permanent Life Insurance Becomes a Balance Sheet Asset

When financial planners talk about life insurance as an asset, they're usually talking about permanent life insurance with cash value.

That cash value is the piece that may show up on a personal net worth statement. Not the death benefit. Not the headline number on the policy illustration. The current value you control.

What counts as the asset

The cleanest technical definition comes from the Financial Planning Association. In its discussion of life insurance value, it explains that a policy's economic value is the net surrender value, not the face amount, and that term insurance generally has no cash value and therefore no realizable asset value while in force, whereas permanent policies accumulate tax-deferred cash value that can be accessed. It also notes that internal charges and surrender penalties can materially reduce early-year value, which can make the policy behave like an illiquid asset. You can read that analysis in the Financial Planning Association journal article on analyzing the value of life insurance as an investment.

That's a mouthful, so here it is in plain English: the asset is what the policy is worth to you today if you accessed or surrendered it, after accounting for the policy's economics.

How cash value gets built

Permanent policies such as whole life and universal life use part of your premium to support the insurance costs and other policy charges. Another portion contributes to the policy's cash value.

Over time, that value may grow on a tax-deferred basis inside the contract. That's one reason some people treat permanent life insurance as a long-term financial asset.

The insurance industry is able to support that structure because it invests premiums over long periods. The Insurance Information Institute reports that in 2020, life/annuity and property/casualty insurers held $9.7 trillion in cash and invested assets, including $4.7 trillion in life insurance and annuity cash and invested assets alone. It also notes that in 2024 life insurers excluding separate accounts held 67.4% of assets in bonds, 2.4% in corporate stocks, and 14.0% in mortgage loans on real estate, while life insurance contracts are typically in force for 10 years or longer. That helps explain why permanent policies can build cash value over time, as described in the Insurance Information Institute facts and statistics on life insurance.

For readers trying to estimate the mechanics, a cash value life insurance calculator can help you see the moving parts.

How it appears on your balance sheet

A simple personal balance sheet might list:

- Checking and savings

- Retirement accounts

- Brokerage investments

- Home equity

- Cash value of permanent life insurance

That last line item is usually based on the policy's available value, not the future death benefit.

Practical rule: If you can't access it today and it has no current surrender value, it usually shouldn't be treated as a present asset on your balance sheet.

Where people overestimate value

Many buyers see a large death benefit and assume the whole number is their asset. It isn't.

The death benefit is primarily a benefit for your beneficiaries after your death. Your current asset, if one exists, is the policy's accessible value during your lifetime. That difference is small in wording but huge in planning.

Using Your Policy's Cash Value as a Financial Tool

Once a permanent policy has built meaningful cash value, you may be able to use it in several ways. At this point, the policy starts acting less like pure insurance and more like a financial instrument.

That sounds appealing, but access isn't free of trade-offs.

Three common ways people use cash value

Policy loans

You borrow against the policy rather than withdrawing from it directly. This can offer flexibility, and it often appeals to people who want access without selling investments.Withdrawals or partial surrenders

You remove some of the accumulated value from the policy. That may reduce what remains available later.Collateral for outside borrowing

In some situations, the policy's value can support lending arrangements with a bank or another lender.

Each method can be useful. Each also changes the policy.

What the trade-offs look like in real life

The simplest way to think about policy access is this: you're pulling value out of a structure that was designed to do more than one job. If you take from one side, the other side can weaken.

The New York Life explainer on whether life insurance is an asset puts the key caution plainly: cash value access can reduce the death benefit, trigger surrender charges, and create tax consequences, and policy performance has become more sensitive to interest rates and insurer assumptions, which makes it important to compare cash value efficiency with more transparent liquid assets such as savings or T-bills. That discussion appears in New York Life's article on life insurance as an asset.

A good comparison test

Before using policy cash value, compare it with alternatives:

- Emergency savings might give you cleaner liquidity.

- T-bills may be easier to understand and track.

- Retirement accounts can have their own trade-offs, but they're often more transparent.

- Brokerage assets may offer clearer pricing and easier access.

That doesn't mean cash value is bad. It means you should ask whether it's the most efficient source of funds for the goal in front of you.

Borrowing from a policy can feel painless at first because there's no sale ticket and no market statement flashing red. The costs are still real. They're just less visible.

Questions to ask before you tap the cash value

- Will this reduce the protection my family was counting on?

- Could a surrender charge make the timing unattractive?

- Will this create taxes I wasn't expecting?

- Am I using this because it's best, or because it feels easier than reviewing other accounts?

Cash value is a tool. It isn't a magic wallet. Used carefully, it can help. Used casually, it can shrink the policy's core purpose.

Why Term Life Insurance Is a Protective Asset

If you stop at the technical definition, term life looks easy to dismiss. No cash value. No surrender value. No line item on your balance sheet.

But that's too narrow for most real households.

Your biggest asset may be your future income

For many young professionals, the most valuable thing they “own” isn't sitting in a bank account. It's the stream of earnings they expect to generate over the next several decades.

That future income pays the mortgage, funds daycare, grows retirement accounts, supports a spouse, and keeps long-term plans on track. If that income disappears, families often don't lose just one paycheck. They lose the engine that supported every other asset.

That's why the narrow question, “Does term life build cash value?” can miss the point.

What term insurance protects

Fidelity Life makes this distinction well. It notes that most articles focus only on whether a policy builds cash value, when for many households the better question is whether it protects the assets they already have. It also explains that term insurance can be highly valuable as an income-protection asset for young families and business owners because it preserves human capital and prevents the forced liquidation of other assets. You can see that framing in Fidelity Life's discussion of using life insurance as an asset.

That protective role is huge. A term policy can help a surviving partner avoid:

- Selling the house under pressure

- Draining retirement accounts early

- Using college savings for living expenses

- Taking on expensive debt just to stay afloat

- Selling part of a business at the wrong time

Why this matters more than cash value for many families

If you're early in your career, your balance sheet may still be modest. You might not have a large taxable estate. You may not need a policy designed for advanced liquidity planning.

You may need enough coverage so the people you love can keep their footing if your income disappears.

That's why term life often makes more sense than chasing a smaller asset inside a more expensive policy. It protects the whole household system.

A term policy may not be an asset you can spend. It can be the reason you don't have to spend down everything else.

A useful mental model

Think of permanent life as a potential stored-value asset.

Think of term life as a shock absorber for your financial life.

Both have value. But if your budget is limited and your family depends on your earnings, the shock absorber often deserves attention first.

Advanced Strategies for Tax and Estate Planning

There's another context where life insurance clearly functions as an asset. High-net-worth planning.

In that setting, the goal usually isn't to squeeze the highest possible investment return out of the policy. The goal is often balance-sheet efficiency, liquidity, and smoother transfer of wealth.

Where permanent insurance can fit

Ash Brokerage's discussion of life insurance as a purpose-built asset explains that for high-net-worth planning, life insurance's advantage is balance-sheet efficiency. It notes that the death benefit is generally paid income-tax-free, and cash value growth is tax-deferred, which allows insurance to create liquidity at death to fund taxes or equalize inheritances without forcing the sale of other assets during a market downturn. That perspective appears in Ash Brokerage's article on life insurance as a purpose-built asset.

That matters most when someone owns assets that are valuable but hard to divide or sell cleanly, such as a closely held business, real estate, or concentrated holdings.

Common advanced use cases

Estate liquidity

A family may need cash at death without wanting to sell property or business interests immediately.

Inheritance equalization

One heir receives an illiquid asset, while another receives cash funded through life insurance.

Tax-aware wealth transfer

The policy can support a transfer plan built around tax treatment and family control.

For readers exploring whether a policy belongs in an estate plan, this overview of whether life insurance is part of an estate adds helpful context.

Why structure matters

Details become critical; ownership, beneficiaries, trust design, and policy funding all affect results.

A permanent policy can be powerful in advanced planning, but only when the policy design matches the planning goal. If the structure is sloppy, costs can eat into the benefit and the strategy loses much of its appeal.

Estate planning with life insurance isn't mainly about calling the policy an asset. It's about making sure heirs receive cash when other holdings are hard to sell, hard to divide, or poorly timed for liquidation.

For most young families, this section is background knowledge, not an immediate to-do list. But it explains why advisors often discuss life insurance very differently with business owners, larger estates, and multi-generational wealth plans.

Choosing the Right Strategy for Your Financial Goals

The best policy isn't the one with the fanciest features. It's the one that matches the problem you need to solve.

For most young families and business professionals, that starts with a plain question: if you died this year, what would happen to the people and plans depending on your income?

A practical decision filter

If your main priorities are protecting a spouse, covering a mortgage, replacing income, or buying time for your family to recover financially, term life is often the clearer first move.

If you've already handled core protection needs, have room in your budget, and have a specific long-term reason to value cash accumulation, permanent life may deserve a closer look.

Questions that help clarify the answer

Do people rely on my income right now?

If yes, prioritize protection.Do I need current access to policy value, or do I just need coverage?

Don't pay for cash value features you may not use.Can my budget support higher premiums for the long haul?

Permanent insurance works best when it's intentionally funded and maintained.Am I comparing life insurance to other places I could keep liquid money?

Cash value should be weighed against simpler assets too.

A simple way to decide

| If this sounds like you | The likely priority |

|---|---|

| Young family, mortgage, tight budget | Get enough term coverage first |

| Established saver, protection already handled | Evaluate whether permanent coverage fits a specific goal |

| Business owner or estate-planning need | Consider advanced review with legal and financial guidance |

The cleanest answer to is life insurance an asset is this: permanent life insurance can be an asset because of its cash value, while term life insurance is usually better understood as a protective asset because it defends your income and existing net worth.

That distinction helps you buy coverage for the right reason, not just the most marketable feature.

If you want life insurance that fits a busy modern life, Coveredly offers a digital, flexible way to explore term coverage built for young families, newly married couples, and professionals who want straightforward protection without unnecessary friction.