You're probably here because life got more serious, fast.

Maybe you just bought a house. Maybe you got married. Maybe there's a baby on the way, or you're thinking about one. Suddenly the question isn't abstract anymore. It's simple and urgent: if something happens to you in the next couple of decades, does your family have enough money to stay in the home, keep paying bills, and avoid financial chaos?

That's exactly where a 20-year term life insurance policy fits. It lines up with real responsibilities that usually have an end date. A mortgage. Raising kids. Replacing income during your highest-expense years. It's not meant to do everything forever. It's meant to protect the years that matter most.

If you're still sorting out the basics, start with this plain-English guide on what a term life insurance policy is. Then come back to the bigger decision: whether 20 years is the right fit for your life.

Table of Contents

- Introduction

- What Is a 20-Year Term Life Insurance Policy

- How Much Does a 20-Year Term Policy Cost

- Who Should Consider a 20-Year Term Policy

- 20-Year Term vs Other Life Insurance Options

- Key Policy Features and How to Apply Today

- Frequently Asked Questions About 20-Year Term Life

Introduction

A couple in their early 30s closes on their first home. The monthly payment is real now. They're talking about kids, daycare, and whether one of them could afford everything alone if the other died unexpectedly.

That's not fear talking. That's financial planning.

A life insurance 20 year term policy is built for this exact window of life. It protects the stretch where your income matters most because other people depend on it. You're not trying to create a forever insurance strategy on day one. You're trying to cover the years when your family is most exposed.

Practical rule: Match the policy term to the years your financial obligations are highest. For many people, that number lands right around 20.

I recommend 20-year term most often for people who need coverage tied to a mortgage, child-raising years, or a business obligation with a defined timeline. It's focused. It's understandable. And for many households, it's the cleanest answer to a very practical problem.

That's its true appeal. You're not buying complexity. You're buying time for your family if your income disappears.

What Is a 20-Year Term Life Insurance Policy

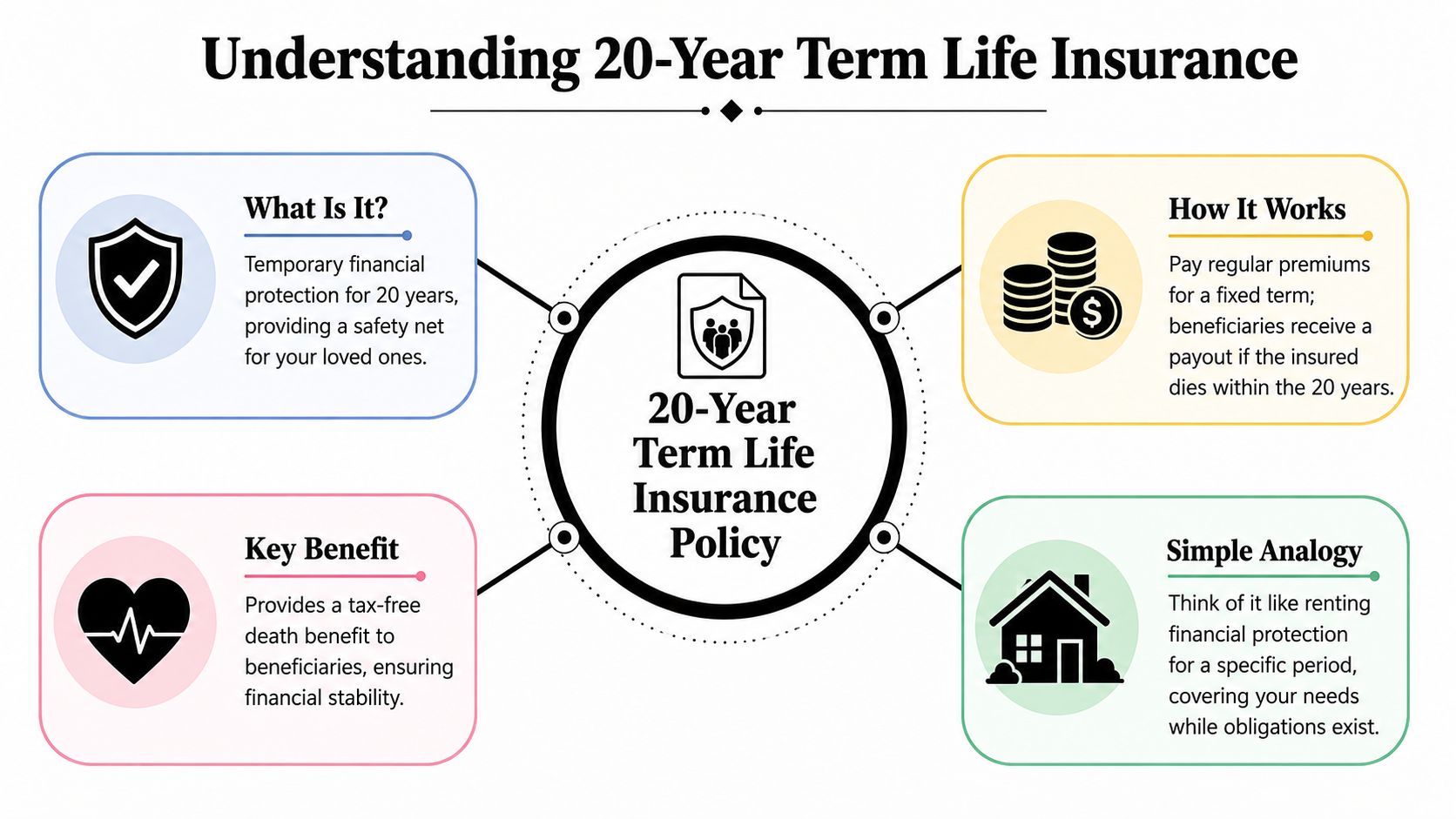

A 20-year term life insurance policy covers you for exactly 20 years. If you die while the policy is active, your beneficiaries receive the death benefit. If you outlive the term, coverage ends unless your policy lets you renew or convert it.

That structure is the whole appeal.

A 20-year term fits the years when your financial obligations are heaviest and most predictable. For a lot of families, that means the stretch when a mortgage is still large, children are still at home, and one income disappearing would create a real problem fast.

The parts that matter

Here's what you should pay attention to before anything else:

- Level premiums. With many 20-year policies, your payment stays the same for the full term. That makes budgeting easier and removes surprises.

- A locked-in death benefit. If you die during the 20 years, your beneficiaries get the coverage amount you chose.

- A clear expiration date. This is temporary coverage for a specific phase of life. It is not built to last forever.

That last point matters more than people think. Buying 20-year term is often a deliberate match to a goal, not a compromise. If you want protection until the kids are through school or the house is mostly paid off, a longer and more expensive policy may solve the wrong problem.

Why people choose this over permanent insurance

Term life usually costs less because it is focused on insurance protection. It typically does not build cash value, which is one of the defining traits of level term life insurance coverage.

My advice is simple. If your priority is replacing income, covering a mortgage, or giving your family time to adjust financially, start with term. Do not pay for cash value features unless you already know why you need them.

Buy coverage for the risk you actually have.

What this policy is really designed to do

A 20-year term policy works best when your biggest obligations have a timeline. That could be 20 years left on a mortgage, 18 years until a newborn becomes financially independent, or a period when your household relies heavily on your income.

This is why 20 years is such a common recommendation. It lines up with real life milestones instead of abstract insurance theory.

And if you apply through a no-exam process, the core coverage still works the same way. The policy can still include standard terms such as the suicide clause and contestability period. Those details matter, especially for buyers who want fast approval and assume no-exam means fewer policy rules. It usually does not. The application is simpler. The contract still deserves a careful read.

How Much Does a 20-Year Term Policy Cost

A 20-year term policy is usually affordable when you buy it at the right stage of life. That is the key point. If you are covering a mortgage, replacing income while your kids are still at home, or locking in protection before health changes, the best price usually comes from acting early.

Price moves for clear reasons. Age pushes premiums up. Smoking can make a cheap policy expensive fast. Health history, coverage amount, and whether you choose a fully underwritten or no-exam application also affect what you pay.

Here is the practical way to look at it. A 20-year term often sits in the middle of the price range. It usually costs more than a 10-year policy because the insurer is covering a longer risk period. It usually costs less than a 30-year policy because the coverage ends sooner. For many families, that middle ground fits the job. You are insuring the years when the house payment is heavy, the kids are dependent, and your income matters most.

What actually drives your quote

Insurers price 20-year term policies based on a short list of factors:

- Age. Younger applicants usually pay less.

- Smoking status. Tobacco use can raise rates sharply.

- Health history. Chronic conditions, prescriptions, and past diagnoses matter.

- Coverage amount. More coverage means a higher premium.

- Application type. No-exam policies can be convenient, but pricing depends on the insurer's underwriting model and your health profile.

That last point gets overlooked. No-exam does not mean no underwriting. It usually means the insurer uses medical databases, prescription history, motor vehicle records, and health questions instead of sending a nurse for labs. Sometimes that leads to a competitive offer. Sometimes a fully underwritten policy comes in cheaper if you are healthy. Compare both before you decide.

If you want a fuller pricing breakdown by age, term length, and health profile, this guide on how much term life insurance costs is a good next step.

Buy when your need is clear and your health is still on your side.

My recommendation is simple. If your family depends on your income and your biggest financial obligations have a 20-year timeline, get quotes now. Waiting rarely helps on price, and it can shrink your options if your health changes.

Who Should Consider a 20-Year Term Policy

You buy a house at 33. Your first child is 2. You have 19 years until that mortgage is gone and about the same stretch until your kid is likely off your payroll. That is the sweet spot for a 20-year term policy.

A 20-year term works best for people with obligations that have a clear end date. I recommend it most often for parents, homeowners, and couples building a life around two incomes. You are not trying to insure every possible future. You are covering the years when someone else would be financially exposed if you died too soon.

That distinction matters. It keeps the decision practical.

Young families

If you have young kids, this is usually the first option I would quote.

The reason is simple. Your family depends on your income most during the child-raising years. Those are also the years when expenses stack up fast. Mortgage or rent, childcare, groceries, activities, and the basic cost of keeping the household running. A 20-year term lines up well with that season of life and gives the surviving parent room to keep the plan intact.

I like 20-year term for parents who want one clear result. If one parent dies, the other parent gets time. Time to keep the house. Time to adjust work. Time to avoid making panicked financial decisions while raising kids alone.

Newly married couples

Marriage changes your risk immediately, even before kids enter the picture.

If you share housing costs, debt, or long-term plans, one death can leave the other spouse carrying bills that were built for two incomes. That is why I push back when newly married couples say they will "wait until later" for life insurance. Later usually costs more, and your need may already be here.

A 20-year term is a strong fit when you are building together. It can cover the years when you are most likely to take on a mortgage, grow your savings, and depend on each other financially.

If one income disappearing would force the other person to sell the house, move, or drain savings, buy the coverage.

Later in the decision process, it can help to watch a plain-English overview like this:

Homeowners with a 15- to 30-year mortgage

This group is one of the clearest matches for a 20-year term.

If your biggest obligation is a mortgage, the policy should roughly match the years when that payment would be hardest for your family to absorb without you. You do not need to overcomplicate it. If your loan, your income plan, and your family timeline all point to the next two decades, 20 years is often the right answer.

I see this a lot with buyers in their 30s and early 40s. They want enough coverage to protect the house and give their family income replacement, but they do not want to pay for a longer term they may not need.

Business professionals

Business owners and key employees often have a separate reason to buy coverage. A loan, a partnership agreement, or the simple fact that the business depends heavily on one person.

A 20-year term can fit well here because many business obligations have a known timeline. You may need coverage while a company loan is outstanding, while a buy-sell plan is in place, or while your family still depends on income coming from the business. In those cases, term insurance does the job without locking you into permanent coverage before the business is more stable.

People who want a faster no-exam option

Some buyers should consider a 20-year term because they need coverage in force soon and want to avoid the scheduling hassle of a medical exam.

That can work well, but be clear-eyed about how no-exam underwriting works. The insurer still checks your prescription history, medical records, driving record, and application answers. You are skipping bloodwork and a nurse visit, not the review itself. If your history is clean and your need is straightforward, a no-exam 20-year term can be a smart shortcut.

One point people ask about all the time is the suicide clause. No-exam policies usually have the same two-year suicide exclusion you will see on many fully underwritten policies. If the insured dies by suicide during that exclusion period, the insurer typically does not pay the full death benefit. After that period, the clause usually no longer applies. Read the policy. Do not rely on assumptions or a quick sales summary.

If your goal is to cover a mortgage, protect kids through school, or replace income during your family's highest-risk years, a 20-year term is often the cleanest choice.

20-Year Term vs Other Life Insurance Options

The right comparison is simple. Match the policy length to the job you need it to do.

If you're covering a 30-year mortgage but expect to refinance, pay it down faster, or build enough savings over the next two decades, a 20-year term often lands in the sweet spot. If you're raising kids who will likely be financially independent within 20 years, the same logic applies. You want coverage for the years your family is most exposed, not for years when the need may be much smaller.

Compared with 10-year and 30-year term

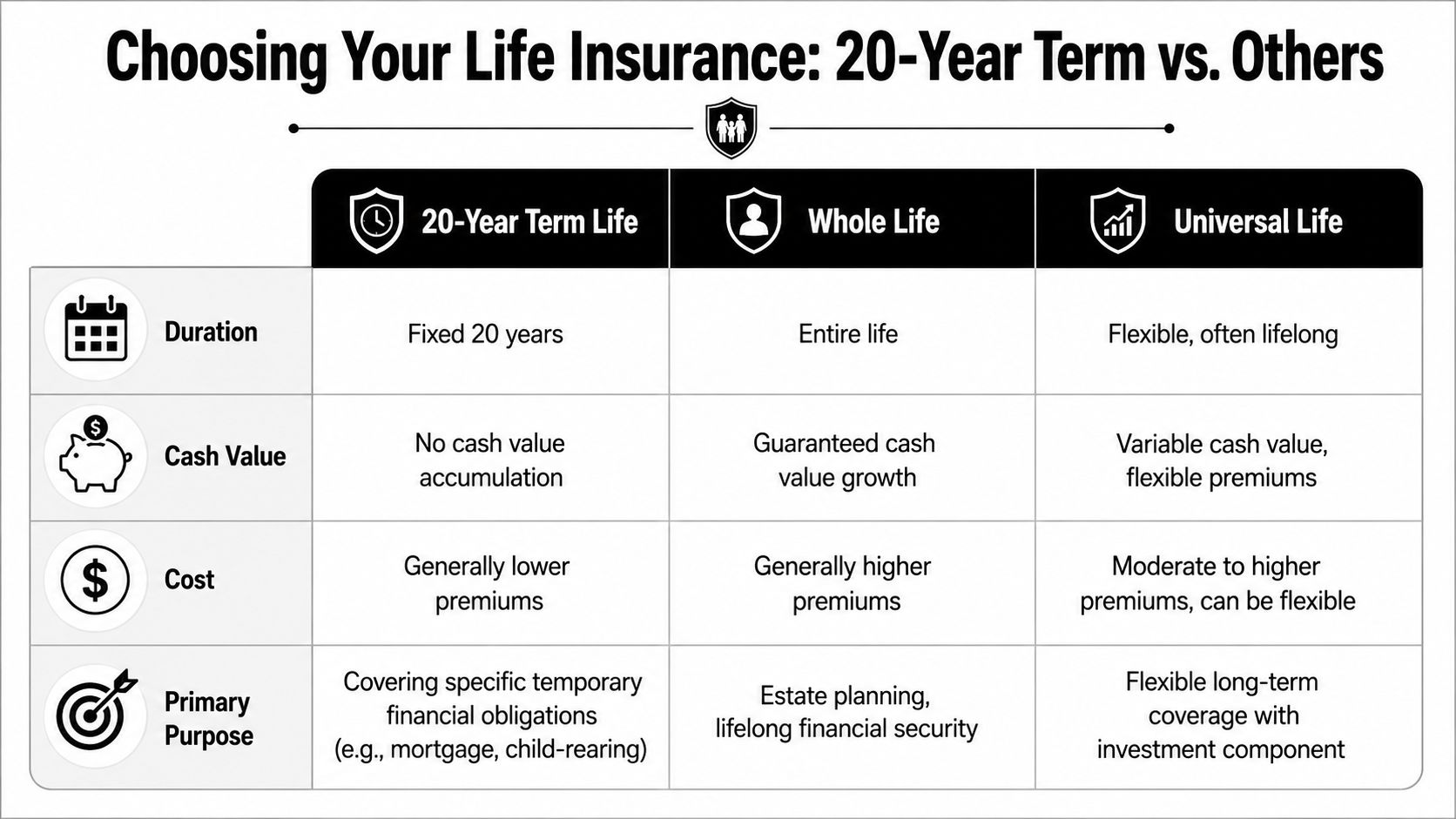

A 10-year term works best for short obligations. A 30-year term works best if you're buying young and want to lock in coverage for a much longer runway. A 20-year term is the practical middle ground for many families.

Here's the cleanest way to look at it:

| Option | Best fit | Main trade-off |

|---|---|---|

| 10-year term | Temporary needs, short debts, or a coverage bridge | Lower cost, but a higher chance you outlive the policy while you still need protection |

| 20-year term | Mortgage years, child-raising years, and peak income-replacement needs | Good balance between price and useful coverage length |

| 30-year term | Very long family timelines or younger buyers locking in coverage early | Higher cost for protection you may not need the whole time |

My advice: don't buy extra years just because longer sounds safer. Buy the term that matches your actual risk window.

A lot of buyers overshoot here. They pick 30 years, pay more, and never had a 30-year problem to solve in the first place.

Compared with permanent life insurance

Permanent life insurance, including whole life and universal life, is built for a different purpose. It can stay in force for life and may include cash value. That sounds appealing, but it also makes the decision more expensive and more complex.

A 20-year term policy keeps the job clear. Protect income. Cover major family obligations. Keep costs under control while your need for insurance is highest.

Choose 20-year term if you want:

- Coverage tied to a specific milestone, such as paying down a mortgage or getting children through school

- A policy that is easier to understand, without mixing protection and long-term cash features

- Lower premiums than permanent insurance usually requires

- A clean exit point, because the need for coverage often drops once debts shrink and assets grow

Choose permanent insurance if you know you need lifelong coverage for estate planning, long-term dependents, or another specific reason. Otherwise, term is usually the better buy.

That's my opinion, and for many working families, it's the right one. Simple protection beats an expensive policy you don't fully need.

Key Policy Features and How to Apply Today

Once you know a 20-year term fits, the next step is choosing a policy that won't create surprises later.

The base policy matters, but the fine print matters too.

Features worth looking for

A few features are worth extra attention when you compare quotes:

- Conversion option. This can let you switch from term to permanent coverage later without starting from scratch on insurability. That matters if your health changes.

- Accelerated death benefit rider. This may allow access to part of the death benefit under qualifying circumstances while you're still living.

- Renewability terms. Some policies let you continue coverage after the term ends, though the cost may change sharply.

I'd focus on clarity over bells and whistles. If you don't understand a rider, ask what problem it solves and when it would realistically matter to your family.

No-exam underwriting and the suicide clause

Many people get confused, especially with no-exam policies.

Almost all 20-year term policies include a 2-year suicide clause, and independent research cited by CoverMe's explanation of 20-year term life insurance says that clause applies regardless of exam status. It does not automatically void the policy. Instead, if death occurs from suicide within that exclusion period, the insurer generally refunds all premiums paid with zero interest.

That point matters because people often assume no-exam coverage changes the clause. It doesn't.

What can change is underwriting risk. No-exam applications can face tighter scrutiny around misrepresentation. If an applicant leaves out or misstates health details, that can create problems during the early contestable period.

Be completely accurate on a no-exam application. The convenience is real, but honesty matters more than speed.

How to apply without overcomplicating it

The application process is usually simpler than people expect if you gather your basics first.

- Choose the protection goal. Are you covering a mortgage, replacing income, or backing a business obligation?

- Pick the term. If your major obligations line up with the next couple of decades, 20 years is often the practical choice.

- Compare underwriting paths. Some buyers prefer traditional underwriting. Others want a no-exam option if they qualify.

- Review policy features carefully. Don't skip conversion terms, exclusions, and beneficiary details.

One digital option is Coveredly, which offers online term life insurance and states that it provides up to $3 million of term life insurance with no exams for most. That may appeal to buyers who want a more simplified process, but you should still read the policy details carefully before you apply.

Frequently Asked Questions About 20-Year Term Life

What happens when my 20-year term ends

In most cases, the coverage ends if the term expires and you're still alive. Some policies may offer renewal or conversion options, but the original 20-year protection period is the main contract you're buying.

That's why timing matters. You want the term to line up with your financial responsibilities, not end years too early.

Can I cancel my policy early if my needs change

Yes, in general you can stop paying premiums and end the policy. But if you cancel, the coverage ends. Since term life usually doesn't build cash value, there typically isn't money waiting for you when you walk away.

Only cancel once you're sure the protection is no longer needed or has been replaced.

Can I have more than one life insurance policy

Yes, many people do. You might layer policies to match different obligations, or carry one personally while another supports a business need. The key is making sure the total coverage amount makes sense and that every application is accurate.

Is no-exam life insurance less reliable than fully underwritten coverage

Not necessarily. The policy can still be legitimate, enforceable coverage. The bigger issue is application accuracy. No-exam doesn't mean no underwriting. It usually means underwriting happens with different tools and less direct medical testing.

If you answer clearly and truthfully, no-exam can be a reasonable path for many buyers.

If you want to price a life insurance 20 year term policy without dragging this out for weeks, Coveredly is one place to start. You can review online term life options, check whether a no-exam path fits your situation, and get a quote based on your timeline and coverage needs.