You've probably had this moment already. You leave a job, start freelancing or building your own business, and feel proud of the freedom. Then one boring admin task opens a much bigger question: “Wait, what happened to my benefits?”

No employer life insurance. No HR portal. No default coverage running in the background.

If you're self-employed, your income may be less predictable, but your responsibilities usually aren't. Rent or a mortgage still has to be paid. Debt doesn't disappear. If you have a partner, kids, or anyone who depends on your earnings, life insurance becomes less about financial theory and more about keeping your household stable if something happens to you.

This guide is built for that exact decision. Not just what life insurance is, but how to choose life insurance for self-employed workers when income changes month to month, and how to estimate the right amount without pretending your finances are as neat as a salary.

Table of Contents

- Why Life Insurance Is Non-Negotiable for the Self-Employed

- Understanding Your Core Life Insurance Options

- How to Calculate Your Coverage Needs

- The Truth About Taxes and Life Insurance

- Advanced Business Uses for Your Policy

- How to Apply and Get Approved When Self-Employed

- Your Self-Employed Life Insurance Checklist and FAQ

Why Life Insurance Is Non-Negotiable for the Self-Employed

The first year of self-employment often feels like a trade. You give up structure to gain control. But one thing many people don't realize right away is that they also give up the safety net that came with a traditional job.

A salaried employee may have employer benefits cushioning the financial hit if something goes wrong. A freelancer, consultant, contractor, or small business owner usually doesn't. If your income stops, there often isn't a company death benefit stepping in for your family.

That's why life insurance for self-employed workers isn't an extra financial product. It's part of replacing what your employer used to handle for you.

Choice Mutual's life insurance research notes that over 100 million individuals in the United States remain completely without life insurance coverage, and that gap is especially important for self-employed workers who have to fund this protection from their own net income.

The risk looks different when you work for yourself

When you're self-employed, your finances are usually more interconnected than they were at a job.

- Your household may depend on one person's production. If you don't work, invoices may stop.

- Your business may depend on your personal relationships. Clients often hire you, not a larger company.

- Your family may not have backup benefits. There may be no group policy, pension, or employer support to soften the loss.

A designer with retainer clients, a real estate agent living on commissions, and a shop owner paying business overhead all face different versions of the same problem. Their income may bounce around, but people still rely on it.

Practical rule: If someone would struggle financially because your income disappeared, you should at least evaluate coverage now, not “once business settles down.”

Why people put it off

Most self-employed people don't avoid life insurance because they think it's useless. They avoid it because the process feels messy.

They're not sure how much coverage makes sense when income varies. They don't know whether term, whole, or universal life fits their budget. They may also assume they can wait until revenue feels more stable.

That waiting period is exactly where confusion turns into risk. Self-employment doesn't remove the need for life insurance. In many cases, it increases it.

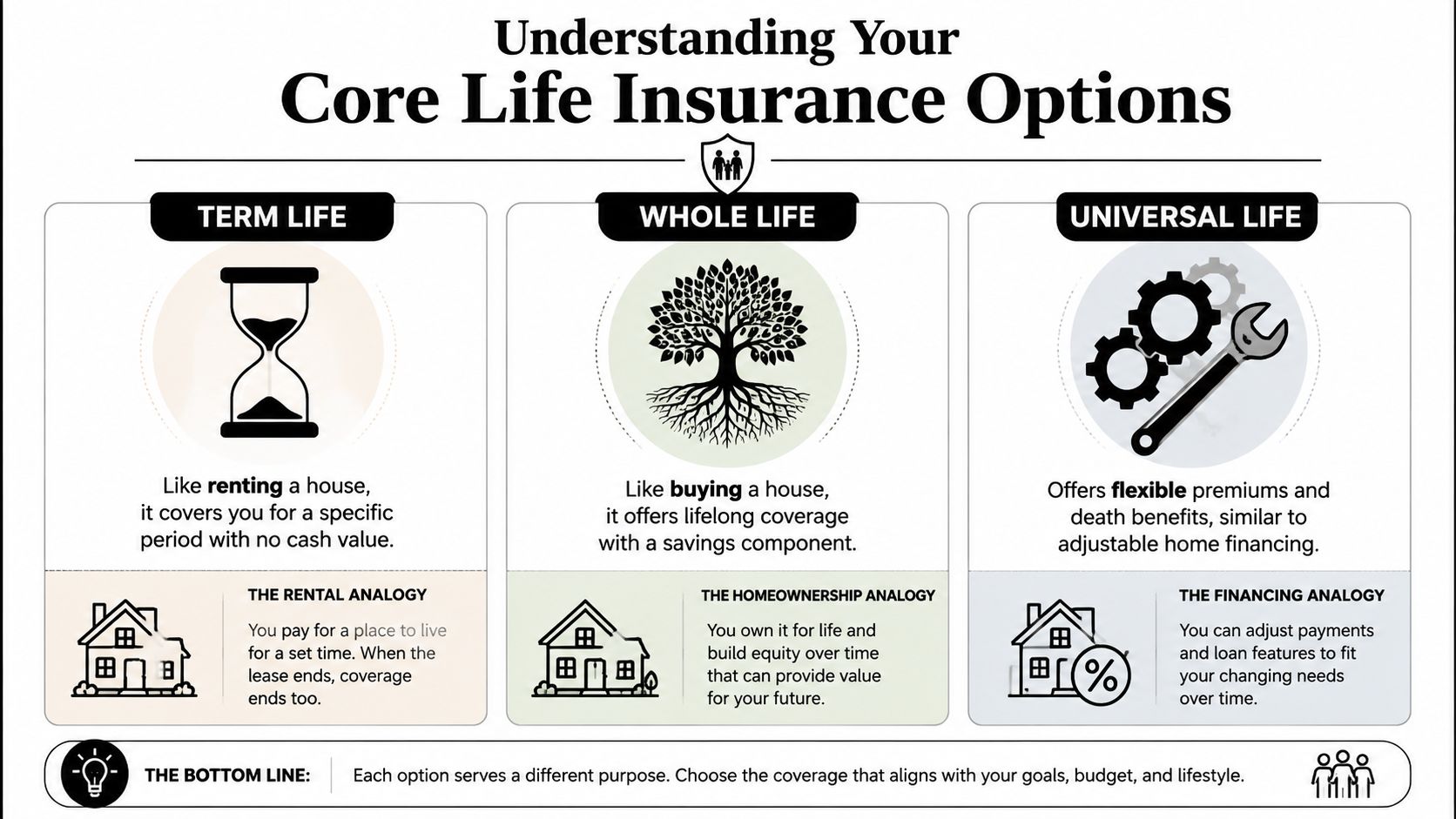

Understanding Your Core Life Insurance Options

The easiest way to understand life insurance is to compare it to housing. Some policies work a bit like renting. Others are closer to buying. That mental model helps when you're sorting through choices without an HR department or benefits advisor.

The simple way to think about policy types

Term life insurance is like renting a house. You're paying for protection during a set period, not building cash value. If you want straightforward coverage for your working years, this is often the cleanest fit.

Whole life insurance is more like buying a house with a long-term savings element built in. It's designed to last your entire life and includes cash value, but that added feature usually makes it more expensive and more complex.

Universal life insurance sits in a more flexible middle ground. It offers adjustable premiums and death benefits in many cases, which sounds appealing, but flexibility can also mean more moving parts to track.

For self-employed people, simplicity matters. When your income isn't identical every month, a policy that's easy to understand and budget for has a real advantage.

The Zebra's life insurance statistics page notes that term life insurance is frequently the most affordable option for self-employed people, with average costs ranging from $40 to $55 per month, and that fixed premium structure helps people manage irregular cash flow.

A side-by-side comparison

| Feature | Term Life | Whole Life | Universal Life |

|---|---|---|---|

| Coverage length | Specific term | Lifelong | Lifelong, with flexible structure |

| Cash value | No | Yes | Yes |

| Cost profile | Usually the most affordable | Typically higher | Often more complex and can vary |

| Simplicity | High | Moderate | Lower for many buyers |

| Fit for variable income | Often strong because premiums are predictable | Can be harder to budget | May appeal to some owners, but needs closer review |

| Main use case | Income replacement during key working years | Long-term coverage with savings component | Flexible long-term planning |

Which one usually fits self-employment best

For many freelancers and founders, term life is the default starting point for a good reason. It does one job clearly: replace income during the years when people rely on you most.

That can line up well with real-life goals, such as:

- Raising children

- Paying down a mortgage

- Covering personal or business debts

- Protecting a spouse while your business is still growing

Whole life and universal life aren't “bad” options. They're just easier to choose when you have a very specific reason for wanting lifelong coverage, cash value, or greater policy flexibility.

Buying coverage you understand is usually better than buying a sophisticated policy you can't explain a year later.

A useful decision filter is this:

- If your main goal is affordable income replacement, term life usually belongs at the top of the list.

- If you want lifelong coverage and are comfortable with a higher ongoing cost, whole life may be worth discussing.

- If you want adjustability and are willing to monitor the policy closely, universal life might fit.

When exploring life insurance for self-employed households, term is where the conversation should start. It matches uneven income, changing expenses, and the need for budget stability.

How to Calculate Your Coverage Needs

The biggest question isn't whether you need life insurance. It's how much. That question gets harder when your income rises and falls, or when your business is still new.

A flat rule of thumb can help you start, but self-employed people usually need a more practical approach than “pick a big number and hope it's right.”

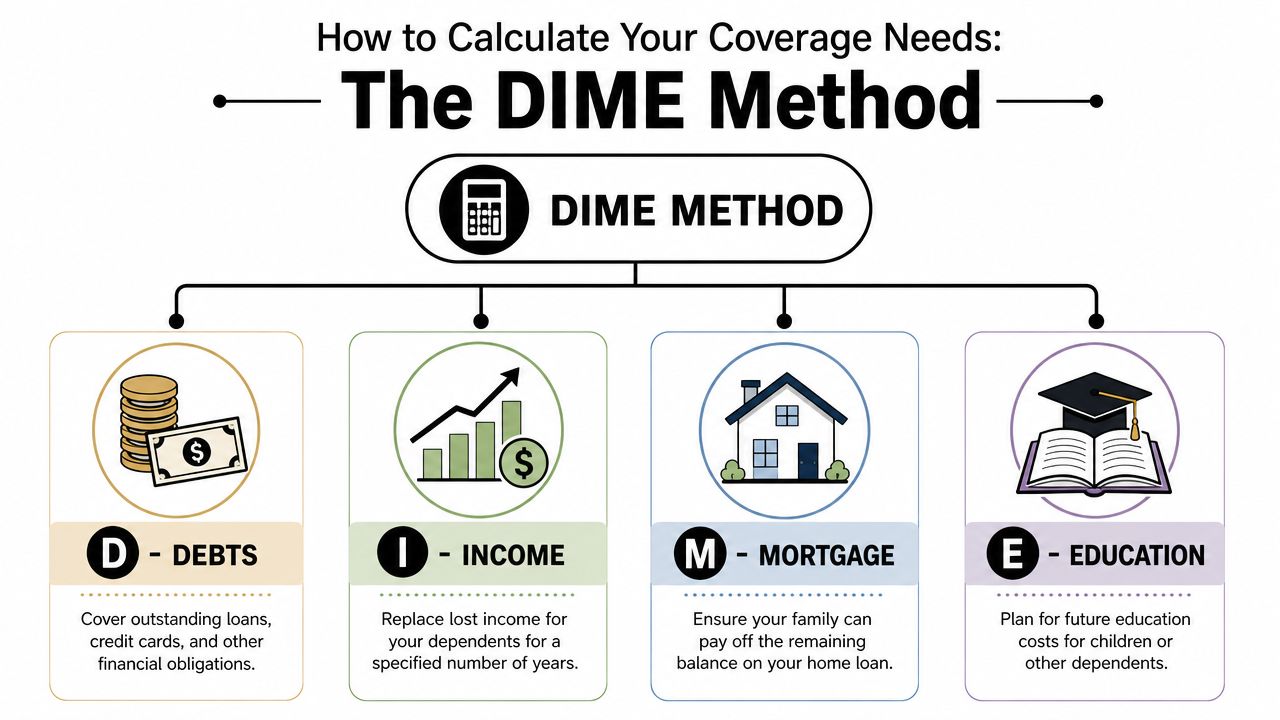

Start with DIME

A common framework is DIME, which stands for Debts, Income, Mortgage, and Education.

Policygenius explains that self-employed individuals can typically apply for life insurance coverage worth 10 to 15 times their annual income, and that benchmark comes from the DIME method.

Here's how to use it in plain English:

Debts

Add obligations your family would still face if you died. Think credit cards, personal loans, private student loans, and business debts that would realistically fall back on your household.Income

Estimate how much income your family would need replaced. This is the heart of the calculation for most freelancers and founders.Mortgage

Include what would be needed to let your family stay in the home without a major financial shock.Education

If you have children or dependents, consider future education costs as part of the cushion.

A good explainer can help if you want a deeper walk-through of the math. This guide on how much life insurance you need is a useful companion when you want to pressure-test your estimate.

Here's a quick visual summary before you start calculating in detail:

How to handle variable income

Freelancers often encounter a dilemma: If one year was strong and the next was uneven, what counts as “annual income”?

You don't need a perfect answer. You need a defensible one.

Use a method that reflects your real earnings pattern:

- Use a multi-year average if your income swings. This smooths out one unusually good or bad year.

- Use a conservative baseline if your business is still stabilizing. Don't build your coverage target around your best month.

- Separate revenue from usable income. Gross business revenue isn't the same as what your household lives on.

- Factor in dependents first. A single freelancer with no dependents may need a different number than a founder supporting a spouse and two children.

A smart coverage estimate should be survivable in your budget and meaningful for your family. If it fails either test, keep refining it.

Build a working number

If rules like 10 to 15 times income feel too abstract, turn the process into three passes.

| Pass | What you're doing | Why it helps |

|---|---|---|

| First pass | Add debts, mortgage needs, and major future obligations | Captures hard liabilities |

| Second pass | Estimate income replacement based on a realistic earning level | Reflects how your family actually lives |

| Third pass | Compare the result against your budget for premiums | Keeps the plan usable |

For newer self-employed workers, precision is hard. That's normal. A strong estimate is usually built from patterns, not certainty.

The goal isn't to predict your career perfectly. It's to choose a coverage amount that gives your family breathing room if your income disappears.

The Truth About Taxes and Life Insurance

A lot of self-employed people assume life insurance works like health insurance at tax time. That's where confusion starts.

The short version is simple: personal life insurance premiums usually aren't tax-deductible if you're self-employed. That surprises people because so many other business-related expenses are deductible.

The rule most freelancers get wrong

If you buy a personal policy to protect your spouse, children, or other loved ones, you generally shouldn't expect to write those premiums off as a self-employment business expense.

That matters because it changes how you budget for coverage. You're paying for personal protection from after-tax income, so affordability matters even more than people expect.

This is one reason term life often rises to the top for freelancers and solo business owners. If the premium isn't deductible, keeping the policy cost manageable becomes part of the decision itself.

When a business policy changes the tax picture

There is an important exception. Western & Southern's guidance on life insurance for self-employed business owners explains that while personal life insurance premiums are generally not tax-deductible for the self-employed, an important exception exists for business-structured policies like key person insurance, where the company is the beneficiary.

That distinction is easy to miss, but it matters.

A business policy can look very different from a personal one:

- Personal policy: Designed to support your family or personal beneficiaries.

- Key person policy: Designed to protect the business if an essential owner or employee dies.

- Buy-sell funding policy: Designed to support an ownership transition between business partners.

If you want a deeper breakdown of the rules, this overview of life insurance tax deduction questions can help clarify where personal and business treatment diverge.

Don't buy a personal policy assuming your accountant will “find a way” to deduct it later. Structure matters from the start.

The practical takeaway is this. Keep your personal protection decision separate from your business tax planning decision. Sometimes one person needs both, but they solve different problems.

Advanced Business Uses for Your Policy

Personal life insurance protects a household. Business life insurance can protect the company itself. If you own a business, that difference matters more than is commonly understood.

A founder's death can create two losses at once. The family loses income, and the business loses leadership, relationships, or operating capacity.

Protecting the business, not just the family

Think of business-focused coverage as a continuity tool. It can create cash at exactly the moment a business may be under the most strain.

That cash can help with:

- Operating expenses while the company regroups

- Recruiting or replacement costs if a key leader dies

- Loan concerns if lenders tied confidence to a specific owner

- Ownership transition problems between surviving partners and the deceased owner's family

This is especially relevant if clients hire your company because of one specific person's expertise or reputation.

Three situations where business owners use coverage differently

Key person protection

A key person policy is meant to help the business survive the loss of someone it depends on heavily. That could be a founder, lead salesperson, technical specialist, or rainmaker whose absence would immediately hurt revenue or operations.

The business is typically the beneficiary. If that person dies, the company receives funds it can use to stabilize itself.

A simple example: a marketing agency may rely on one partner who brings in most major clients. If that partner dies, the business may need time and money to keep staff, reassure customers, and rebuild the sales pipeline.

Buy-sell agreements

When two or more people own a company together, death can create a messy ownership question. The surviving partner may want to keep the company running, while the deceased owner's family may need liquidity.

Life insurance can fund a buy-sell arrangement so ownership transfers according to a plan rather than a crisis. Without that structure, surviving partners and family members can end up negotiating under stress.

Good business planning isn't just about growth. It's about making hard moments less chaotic for the people left behind.

Loan and debt support

Some small businesses take on debt to launch, hire, or expand. If an owner dies, those obligations don't automatically become easy to manage.

Coverage can help the business deal with debt pressure, preserve credibility with lenders, and avoid a forced sale of assets. This won't matter in the same way for every freelancer, but for businesses with employees, partners, or financing, it can be a major part of risk management.

The key is deciding what problem you're solving. Personal policies are for loved ones. Business policies are for continuity, ownership, and obligations tied to the company itself.

How to Apply and Get Approved When Self-Employed

Applying for life insurance when you're self-employed can feel awkward because the paperwork doesn't look like a normal employee file. You may not have pay stubs. Your income may vary. Some of your earnings may come from multiple clients or business channels.

That doesn't make you uninsurable. It just means insurers often verify your finances differently.

What insurers usually want to see

For self-employed applicants, income documentation is a big part of the process. Instead of an employer confirming salary, insurers often look at your tax records and other financial documents to understand your earnings history.

Fidelity Life notes that a primary challenge for new self-employed workers is estimating net income for applications, and insurers may recommend using a multi-year earnings history or validated industry averages to establish a reliable figure for underwriting.

That usually means it helps to gather:

- Recent tax returns

- Business income records

- Documentation showing how long you've been operating

- Details on major debts or obligations

- Basic personal health information

If you want a clearer sense of what underwriters evaluate, this primer on underwriting life insurance can make the process less mysterious.

How to make the process smoother

Self-employed applicants usually do best when they present a stable, understandable financial picture.

A few practical moves help:

Use net income thoughtfully

If your income has changed a lot, be ready to explain which number best represents your normal earnings.Organize your documents before applying

Underwriting gets slower when records are scattered across tax software, bookkeeping tools, and email attachments.Be consistent across forms

If one document shows one income figure and another tells a different story, expect follow-up questions.Apply while your health is strong

Many people wait for their business to feel “finished” before buying coverage. Health doesn't always wait for your revenue milestones.

Some policies also offer efficient digital application processes, and some applicants may qualify for no-exam options depending on the insurer and the coverage requested. That can remove a lot of friction for busy founders and freelancers who don't want a long, medical-heavy process.

The best mindset is to treat your application like a business file. Clear records, realistic income numbers, and consistency make the whole process easier.

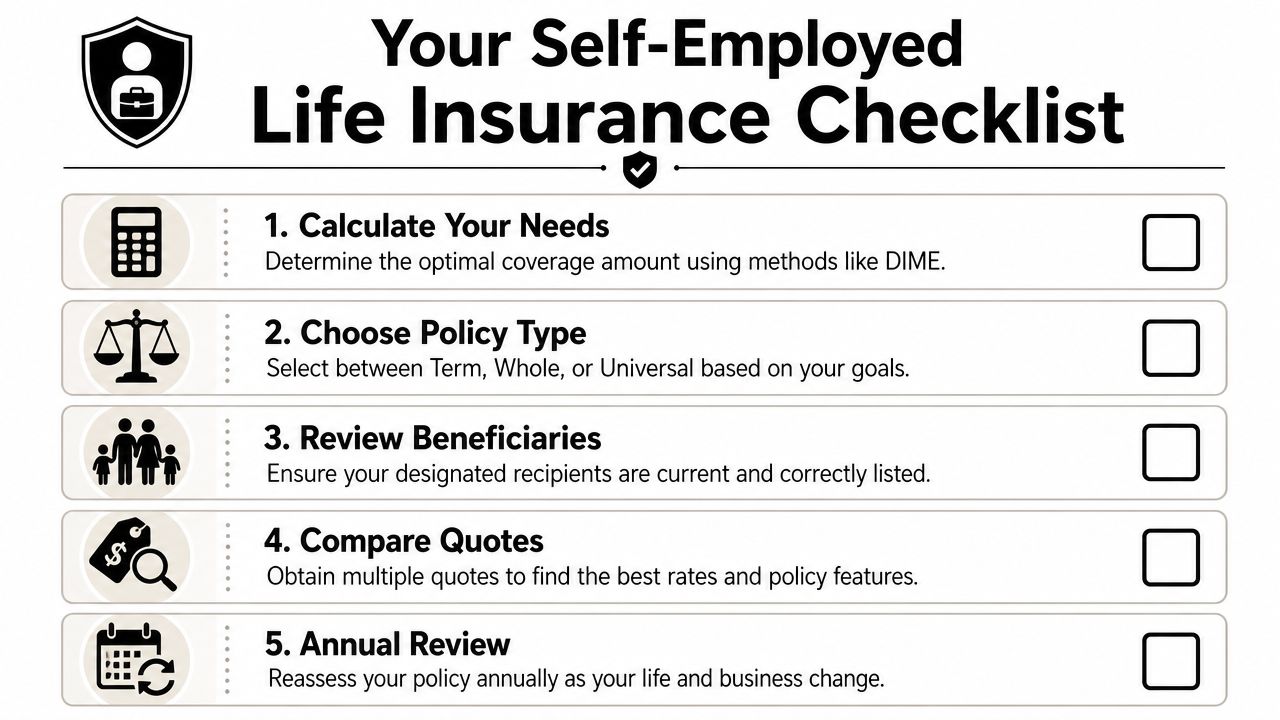

Your Self-Employed Life Insurance Checklist and FAQ

The hardest part of life insurance for self-employed people usually isn't the product. It's decision fatigue. There are a lot of moving parts, and nobody is standing next to you in HR telling you what box to check.

A simple checklist helps cut through that.

A practical checklist

- Calculate your needs first. Use DIME as a starting point and adjust for the reality of your business income.

- Choose the policy type that matches your budget and goal. For many people, term is the clearest fit when the main job is income replacement.

- Check whether you need personal coverage, business coverage, or both. A founder with dependents and a business partner may need two separate solutions.

- Gather your financial documents early. Tax returns and clean income records make applications easier.

- Review your beneficiaries. Life changes. So should your paperwork.

- Compare quotes carefully. Price matters, but so does policy clarity and how confident you feel about keeping it long term.

- Revisit your coverage each year. A new child, a mortgage, a business loan, or a jump in income can all change the right amount.

FAQ

Can I get life insurance if my business is new

Yes, you often can. The main challenge is usually documenting income clearly and choosing a realistic coverage amount.

What if my income changes a lot from year to year

That's common. Many self-employed people use a multi-year view or a conservative baseline instead of relying on one unusually good year.

Is term life usually the best option for freelancers

Often, yes. It's commonly the simplest and most budget-friendly way to cover the years when others depend on your income.

Should I buy coverage for my family or my business

That depends on your situation. If loved ones rely on your earnings, personal coverage matters. If the company would also suffer financially from your loss, business coverage may matter too.

Do I need to review my policy after I buy it

Absolutely. Self-employment changes fast. Coverage that made sense when you were a solo contractor may be too small or poorly structured once you have a spouse, kids, employees, or debt.

If you want a simpler way to buy life insurance online, Coveredly offers a digital-first experience built for modern life. You can explore flexible term coverage, including up to $3mm of term life insurance with no exams for most, and find an option that fits your family, budget, and business stage.