TL;DR: Personal life insurance premiums usually aren’t tax-deductible. A commonly overlooked exception is that the bigger tax benefit is often on the back end: life insurance death benefits are generally income tax-free, employer-paid group term life up to $50,000 per employee can be deductible to the business, and older divorce agreements finalized on or before December 31, 2018 may follow different rules.

A lot of financial advice trains people to ask one question first: “Can I deduct it?” That’s a useful habit, but it leads many smart professionals to undersell life insurance.

With life insurance, the better question isn’t just whether there’s a tax write-off. It’s whether the tax treatment helps your family or business when the money matters most. In many cases, that answer is yes, even though the premium itself isn’t deductible.

If you’re comparing term life, reviewing employer benefits, or sorting out business coverage, tax rules can feel more confusing than they should. A good starting point is understanding how life insurance works and how to choose coverage. After that, the tax side gets easier to place in context.

Table of Contents

- The Big Question About Your Life Insurance and Taxes

- The Core Rule Why Premiums Are Not Tax Deductible

- The Real Tax Advantages Beyond a Deduction

- Business Scenarios Where Premiums Can Be Deductible

- How Smart Tax Planning Uses Life Insurance

- Answering Your Top Questions on Life Insurance Taxes

The Big Question About Your Life Insurance and Taxes

Many individuals expect life insurance to work like a retirement account contribution, mortgage interest, or a business expense. Pay money in, get a deduction back. That expectation sounds reasonable, but it’s usually wrong.

For personal coverage, the clean answer is no. If you buy a policy to protect your spouse, kids, or anyone who depends on your income, the premium usually doesn’t lower your taxable income.

That sounds disappointing at first, especially for young families watching every dollar and business owners trained to look for legitimate write-offs. But stopping at “no deduction” misses the feature that makes life insurance valuable in the tax code.

What trips people up

The confusion comes from mixing up premium deductibility with tax treatment of benefits. Those are not the same thing.

A premium is what you pay. A death benefit is what your beneficiary receives. The tax code treats those two cash flows differently, and that distinction matters much more than most online summaries admit.

Many people look for a tax break at purchase and miss the tax advantage at payout.

That’s why the life insurance tax deduction question needs a more careful answer than a simple yes or no. A policy can fail the deduction test and still deliver strong tax advantages for your household or business planning.

What this means for a busy professional

If you’re newly married, raising kids, or running a company, the practical issue isn’t whether premiums feel deductible. It’s whether the policy creates efficient protection.

In real life, that means asking:

- Who needs the money: A spouse, children, business partner, or employees?

- When would they need it: During income loss, debt payoff, business transition, or estate planning?

- How will taxes affect the payout: At the income tax level, business level, or possibly the estate level?

Those are better planning questions than “Can I write this off?”

The better frame

Think of life insurance less like a deductible expense and more like a tax-advantaged protection tool. That framing helps you make smarter decisions about term life, workplace benefits, and business coverage structures.

The Core Rule Why Premiums Are Not Tax Deductible

The IRS generally treats personal life insurance premiums as personal expenses, which is why they usually aren’t deductible. That treatment has been in place since the Revenue Act of 1913 and applies broadly across personal policy types, as summarized in the American Council of Life Insurers federal taxation guidebook.

Why the IRS treats premiums as personal expenses

The simplest way to understand the rule is to compare life insurance to other personal bills. You pay for car insurance, homeowners insurance, and your car loan out of after-tax dollars. Personal life insurance generally falls into that same bucket.

The IRS doesn’t see a personal policy as a business cost or an investment contribution that deserves an immediate deduction. It sees it as a private family expense. That’s the core reason the deduction usually isn’t available.

A useful analogy is this: paying a life insurance premium is like paying to install a strong lock on your front door. It protects your household, but the cost of that protection usually isn’t deductible just because it’s prudent.

Which policies this rule covers

Readers often hope for a loophole. There usually isn’t one.

The non-deductible rule generally applies to the main personal policy categories:

- Term life insurance: Temporary coverage for a set period.

- Whole life insurance: Permanent coverage with cash value.

- Universal life insurance: Flexible premium permanent coverage.

- Variable universal life insurance: Permanent coverage with investment-linked cash value.

The presence of cash value doesn’t convert the premium into a deductible expense. That’s a common misunderstanding.

Practical rule: If you’re paying for a personal policy to protect your family, start from the assumption that the premium is not deductible.

Why this rule has lasted so long

The tax code has long separated personal consumption from deductible spending. Some costs qualify because lawmakers want to encourage a specific activity or because the expense directly supports income production. Personal life insurance generally doesn’t fit either category in the way the tax code defines them.

That doesn’t mean life insurance lacks tax value. It means the tax value shows up in a different place.

Here’s a quick comparison that helps:

| Expense or benefit | Usually deductible for an individual | Main tax value |

|---|---|---|

| Personal life insurance premium | No | Tax advantages often come later |

| Mortgage interest | Sometimes | Potential itemized deduction |

| Traditional retirement contribution | Sometimes | Potential upfront deduction |

| Personal auto payment | No | Personal use, no deduction |

That distinction is the backbone of the life insurance tax deduction conversation. If you start with the IRS category correctly, the rest of the rules make more sense.

The Real Tax Advantages Beyond a Deduction

The biggest mistake people make is treating “not deductible” as “not tax-advantaged.” Those are very different outcomes.

Life insurance often delivers its strongest tax value after the policy is in force, not when the premium is paid. For many families, that matters more.

The tax break most families actually use

The hallmark benefit is the income-tax-free death benefit. Under long-standing federal tax treatment, life insurance proceeds are generally excluded from a beneficiary’s gross income. The IRS explains that life insurance proceeds paid because of the insured person’s death generally aren’t includable in income, while any interest paid later is taxable, in the IRS FAQ on life insurance proceeds.

That means if a beneficiary receives policy proceeds after the insured dies, the benefit itself is generally not taxed as income. This is the feature many people care about most, even if they’ve never described it that way.

What surprises people is how many Americans don’t know this rule. A 2023 Assurance IQ study found 30% believe death benefits are taxable and 36% are unsure, as cited in that same IRS-linked source context above. That confusion explains why the life insurance tax deduction question gets so much attention. People focus on the missing deduction and overlook the much larger tax advantage.

If your goal is protecting your family’s income, tax-free money to beneficiaries can matter more than a deduction on the premium.

How cash value changes the picture

Permanent life insurance introduces another layer: tax-deferred cash value growth. In plain English, that means the policy’s internal value can grow without annual taxation on that growth while it remains inside the policy.

That’s different from a regular taxable brokerage account, where gains, dividends, or interest may create tax consequences along the way. With cash value life insurance, the timing of taxation works differently.

Some policies also allow access to cash value through policy loans that can be structured without immediate tax consequences. That doesn’t mean every withdrawal is automatically tax-free, and it doesn’t mean every policy should be used this way. It means the tax treatment can be more flexible than many people expect.

For readers who prefer a quick visual explanation, this short overview helps clarify the difference between paying premiums and receiving benefits:

Why this matters more than a write-off

A deduction reduces taxable income today. A tax-free death benefit can protect your family when income stops tomorrow. Those are not equal benefits.

For a young couple with a mortgage and children, the core purpose of life insurance is replacing income and preserving choices. If the surviving spouse receives proceeds that generally aren’t taxed as income, that can help cover mortgage payments, child care, college savings, and everyday bills without adding an income tax burden to a crisis.

For a business professional, the same principle matters differently. The proceeds can support continuity, buy time, and give the people left behind more flexibility about what to do next.

Here’s the practical comparison:

- A deduction helps the payer now: Useful, but often limited.

- Tax-free death benefits help the beneficiary later: Often more valuable when protection is the primary objective.

- Tax-deferred cash value can add planning flexibility: Relevant mainly for permanent policies and more advanced use cases.

The right takeaway isn’t “I can’t deduct it, so it’s a bad deal.” The better takeaway is “the tax break is built into the policy outcome, not the premium payment.”

Business Scenarios Where Premiums Can Be Deductible

Business owners face a different set of rules. The life insurance tax deduction answer can change when coverage is tied to employees, compensation, or charitable planning.

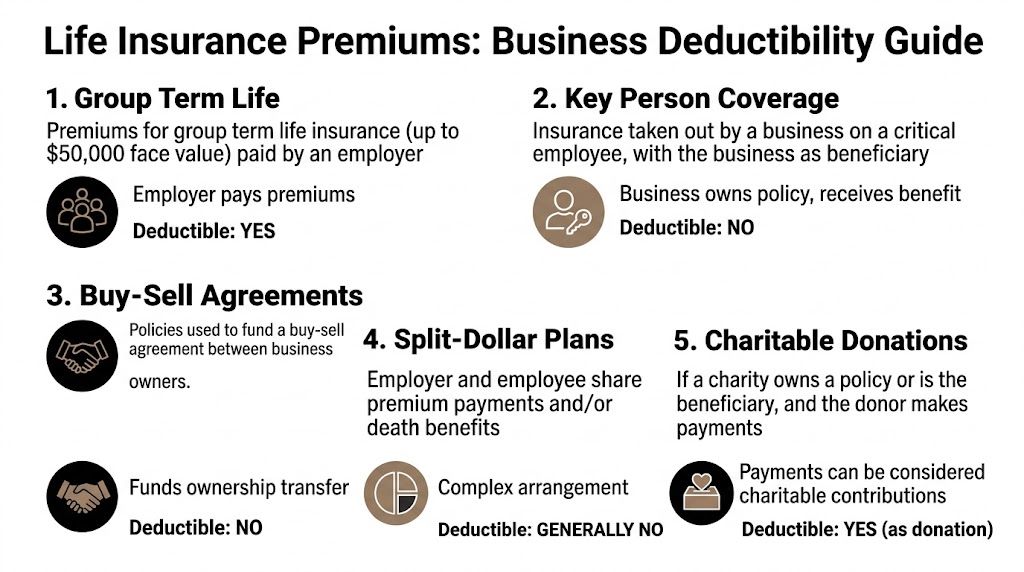

The cleanest and most common business exception is group-term life insurance. Other business-related policies often sound deductible but usually aren’t, especially when the business is the beneficiary.

If you’re evaluating benefits for a growing company, this overview of life insurance for small business owners can help put the tax rules into a larger planning context.

Group term life for employees

Under IRC Section 79, employers can generally deduct premiums for group-term life insurance up to $50,000 of coverage per employee as a business expense, according to the IRS guidance on group-term life insurance.

For the employee, that same amount can generally be excluded from gross income. This is why group term life is such a common workplace benefit. It’s relatively simple, useful, and tax-efficient within the stated limit.

The rule changes when coverage goes above that threshold. The excess coverage can create imputed income for the employee, calculated under the IRS Premium Table.

Here’s the example provided in the verified data:

| Coverage setup | Tax result |

|---|---|

| Up to $50,000 of employer-provided group-term coverage | Employer can generally deduct premiums, employee generally has no tax consequences |

| $100,000 of coverage for a 40-year-old non-smoker | The $50,000 excess can create taxable imputed income using the IRS monthly rate of $0.05 per $1,000, resulting in $300 annual imputed income |

That example matters because it shows how the tax rule works in practice, not just in theory.

Key person insurance and why the rule changes

Key person coverage is where many business owners get tripped up. A company buys a policy on an essential employee, founder, or executive because losing that person could hurt revenue, operations, lender relationships, or customer trust.

Even though the policy serves a business purpose, premiums are generally not deductible when the business is the direct or indirect beneficiary. The tax logic is straightforward: if the business stands to receive the benefit, the IRS usually doesn’t allow the premium write-off.

This is the same pattern you saw in personal coverage, but for a different reason. Personal premiums are non-deductible because they’re personal expenses. Key person premiums are usually non-deductible because the business could collect the tax-advantaged benefit.

A useful rule of thumb for business owners is this: when your company is set to receive the death benefit, don’t assume the premium is deductible.

That doesn’t make key person insurance a poor decision. It just means the value is risk management and liquidity, not a current deduction.

Buy-sell funding and other common business setups

Buy-sell agreements often use life insurance to fund an ownership transfer after an owner’s death. It’s a practical tool because it can create cash at exactly the moment the surviving owners or the deceased owner’s family need it.

But the premium usually isn’t deductible just because the agreement is business-related. The policy may be essential to the deal, and still not create a deduction.

The same caution applies to more complex arrangements. Business owners often hear terms like split-dollar plans, executive bonus arrangements, and loan-related life insurance. These structures can be legitimate, but the tax treatment depends on ownership, beneficiary design, compensation treatment, and plan details.

Here’s a scan-friendly summary:

- Group term life for employees: Often the clearest deduction opportunity within the IRS limit.

- Key person insurance: Generally not deductible when the business benefits from the policy.

- Buy-sell agreement funding: Useful for succession planning, but premiums are generally not deductible.

- Charitable situations: In some setups, payments tied to a charity-owned policy may be treated differently, often under charitable contribution rules rather than standard life insurance deduction rules.

- Complex compensation arrangements: These need legal and tax review before anyone assumes deductibility.

For small companies, the practical move is to separate two questions. First, “Does this coverage solve a real business risk?” Second, “Who owns the policy and who receives the benefit?” The tax answer often turns on that second question.

How Smart Tax Planning Uses Life Insurance

Tax-smart planning with life insurance starts when you stop chasing the wrong outcome. The premium deduction usually isn’t the prize. The useful question is how the policy supports your broader plan without creating avoidable tax friction.

That looks different for a family than it does for an owner-operator or partner in a firm.

Strategies for young families

For young families, the best use of life insurance is usually simple: protect income, preserve the home, and buy the surviving spouse time to make clear decisions.

A family doesn’t need a complex tax strategy for life insurance to be smart. They need the right amount of coverage, the right beneficiary setup, and a clear understanding of what the money is meant to do.

Consider a practical household checklist:

- Income replacement: Cover the years when one paycheck disappearing would change everything.

- Debt protection: Make sure a mortgage or major loan doesn’t force a sale at the worst possible time.

- Child-related costs: Think through child care, schooling, and the cost of buying time for the surviving parent.

- Estate coordination: Review beneficiary choices alongside wills and trusts, especially if you’re already doing broader planning.

If you’re thinking about beneficiaries and transfer issues, this guide on whether life insurance is part of an estate is a useful next read.

One tax point matters here. Even if your estate is well below the federal estate tax threshold, life insurance can still be tax-efficient because the death benefit is generally treated differently from ordinary taxable income. That can help a family hold onto more flexibility during a hard transition.

Strategies for business professionals

Business professionals use life insurance differently. The planning goal is often continuity rather than simple household replacement.

A business owner might use coverage to support obligations such as:

| Business need | How life insurance can help |

|---|---|

| Employee benefits | Group term life can improve compensation packages and support retention |

| Partner succession | Policies can provide liquidity for a planned ownership transfer |

| Family-business continuity | Insurance can reduce pressure to sell assets quickly |

| Personal guarantee concerns | Coverage can protect the owner’s family from business-linked financial strain |

These uses aren’t all about tax deductions. Often they’re about making sure a death doesn’t force terrible decisions in the business.

Good life insurance planning helps people avoid a fire sale. That may be more valuable than any premium write-off.

A simple decision lens

If you’re trying to make a clean decision without getting lost in tax jargon, use this three-part lens:

Start with the purpose

If the policy is for family protection, don’t expect a deduction. Focus on coverage quality, beneficiary design, and affordability.Check who owns and benefits from the policy

In business planning, this often determines whether premiums might be deductible, taxable to someone, or neither.Coordinate with the rest of your plan

Life insurance works best when it matches your legal documents, business agreements, and benefit design.

Many people overcomplicate life insurance tax deduction questions because they treat life insurance as a tax product first. It isn’t. It’s a protection product with important tax features.

That distinction keeps your planning honest.

Answering Your Top Questions on Life Insurance Taxes

The broad rules are simple. The edge cases are where people get stuck. These are the questions that usually deserve a second look before you sign paperwork or claim anything on a return.

Are life insurance premiums deductible in a divorce settlement

Sometimes, but the date of the divorce agreement matters.

For divorce agreements finalized before January 1, 2019, life insurance premiums paid by one spouse to secure alimony obligations could be treated as deductible alimony if the arrangement met the applicable rules. The key date and rule change are summarized in Northwestern Mutual’s explanation of life insurance deductibility and TCJA changes.

For agreements finalized after that date, the Tax Cuts and Jobs Act of 2017 eliminated that deduction for later agreements. In those newer cases, the premium is generally treated like a non-deductible personal expense.

The confusion here usually comes from old advice still circulating online. Someone may read a forum post or older article and assume the deduction still exists for everyone. It doesn’t.

A careful takeaway:

- Older agreements may follow the old alimony rules

- Newer agreements generally do not

- The policy owner and beneficiary setup can still matter

- This is one of the situations where document review matters more than general tax tips

When does cash value become taxable

Cash value life insurance often gets described too casually. People hear “tax-deferred” and assume “never taxed.” That’s not the same thing.

Tax-deferred growth means the policy’s internal buildup generally isn’t taxed year by year while it stays inside the contract. That’s the main advantage. But taxation can enter the picture depending on how money comes out or how the policy ends.

A useful way to think about it:

- Growth inside the policy: Generally tax-deferred

- Policy loans: Often can avoid immediate tax consequences if structured properly

- Full surrender or certain distributions: May create taxable consequences depending on the policy and amount withdrawn

The exact tax result depends on policy basis, loan status, and whether the policy remains in force. That’s why “cash value is tax-free” is too broad to rely on.

Tax-deferred does not mean tax-proof.

If you own permanent life insurance and plan to use the cash value, ask for an in-force illustration and have your tax advisor review the withdrawal or loan strategy before acting.

How do state taxes affect life insurance

Federal income tax rules get most of the attention, but state-level issues can matter too.

The main gap in many life insurance tax deduction articles is that they focus only on federal income tax and ignore state estate taxes, inheritance taxes, and state-specific rules that may affect how life insurance fits into your broader plan. Those state rules can vary significantly by jurisdiction.

For many readers, that won’t change the day-to-day treatment of a personal premium. But it can change planning decisions around ownership, trusts, beneficiary choices, and estate exposure.

This matters most if you:

- Live in a state with its own estate or inheritance tax

- Own property or businesses in multiple states

- Have a larger estate or more complex family structure

- Use trusts as part of your planning

A national article can explain the federal baseline. It can’t replace state-specific legal advice.

Can life insurance fit into retirement planning

Yes, but the answer depends on how you’re using the policy.

One underexplained area in public guidance is the interaction between life insurance and retirement planning. The issue usually isn’t that premiums become directly deductible. It’s that some workplace and qualified plan contexts can change how the premium is funded, how annual taxable value is reported, and how death benefits coordinate with inherited retirement assets.

For a young professional or newly married couple, the planning question is usually priority. Should you first max retirement accounts, buy term life, use a permanent policy, or mix the strategies?

In most cases, the answer depends on your goals:

| Goal | Typical life insurance role |

|---|---|

| Protect a spouse or children | Core protection tool |

| Build retirement savings | Usually not the first account to prioritize on tax grounds alone |

| Estate coordination | Can be useful depending on ownership and beneficiary structure |

| Employee benefits planning | Often relevant through workplace coverage |

If your main concern is replacing income, life insurance and retirement accounts solve different problems. One protects against dying too soon. The other funds living a long life. Good planning uses both for their intended purpose.

What should you do before claiming any deduction

Treat life insurance deductions as an exception, not a default.

Before claiming anything, verify:

- Who owns the policy

- Who pays the premium

- Who receives the death benefit

- Whether the policy is personal, employer-provided, or tied to a legal obligation

- Whether a rule changed based on the date of an agreement

That checklist catches many mistakes before they turn into filing errors.

If you’re a business owner, also confirm whether the coverage is part of a formal employee benefit arrangement or whether it benefits the company directly. Those details often control the tax answer.

For families, the better move is usually not hunting for a deduction that doesn’t exist. It’s making sure the policy amount, term length, ownership, and beneficiaries line up with your actual financial life.

If you want a simpler way to shop for coverage that fits modern family and business needs, Coveredly offers online life insurance with up to $3mm of term life insurance and no exams for most. It’s a practical option for busy professionals who want flexible coverage without turning the process into another full-time project.