You may be staring at a quote screen late at night, after the kids are asleep, wondering whether life insurance for smokers is even worth trying for. Maybe you smoke every day. Maybe you quit recently and had a relapse. Maybe you only have the occasional cigar and you're not sure whether that counts. The common fear is simple: if you use tobacco, coverage will be too expensive or completely out of reach.

That fear is understandable, but it isn't the full story. Smokers can get life insurance. A key challenge is learning how insurers classify tobacco use, how pricing works, and which path gives you the best chance at manageable premiums and solid coverage. If you understand those rules, you can make better decisions without guessing.

Table of Contents

- Your Guide to Getting Life Insurance as a Smoker

- Why Smokers Pay More for Life Insurance

- How Insurers Define a Tobacco User

- The Financial Impact of Smoking on Premiums

- Your Path to Lower Premiums by Quitting

- How to Shop and Apply for Coverage as a Smoker

- Frequently Asked Questions About Smoking and Life Insurance

Your Guide to Getting Life Insurance as a Smoker

If you smoke and you're shopping for coverage, start with one important mindset shift: higher cost doesn't mean no options. Insurers price tobacco use as added risk, but they still issue policies to smokers every day. For young families, newly married couples, and busy professionals, that matters. Some protection in place is usually better than waiting for a perfect moment that may not come.

A clear example helps. A 40-year-old male smoker in good health pays roughly $88 per month for a $500,000, 20-year term life insurance policy, compared to $28 per month for a nonsmoker with the same profile, according to Insurance Geek's underwriting example. That's a meaningful difference. It's also proof that coverage exists, even for smokers.

What most people get wrong

Many shoppers assume life insurance for smokers works like a hard rejection system. It usually doesn't. Insurers tend to ask a different question: how much risk are they taking on, and what premium fits that risk?

That means your job isn't to wonder whether you're allowed to apply. Your job is to apply strategically.

A smart approach usually looks like this:

- Figure out how the insurer will classify your nicotine use. Cigarettes, cigars, vaping, and smokeless tobacco can all matter.

- Decide whether an exam-based or no-exam policy fits your timeline. Speed and price don't always move together.

- Be honest from the first application. Misstating tobacco use can create much bigger problems than a higher quote.

- Revisit your rates later if you quit. Your first policy doesn't have to be your forever policy.

Practical rule: Buy coverage based on your family's needs now, then improve the price later if your health profile improves.

Why this matters for young families

If someone depends on your income, your unpaid caregiving, or your business contribution, life insurance isn't just a line item. It's part of your financial backup plan. Rent or mortgage payments don't pause because a family is grieving. Childcare, debt, and daily bills don't pause either.

That is why the right question isn't, "Can smokers get approved?" It's, "What's the clearest path to coverage I can put in force now?"

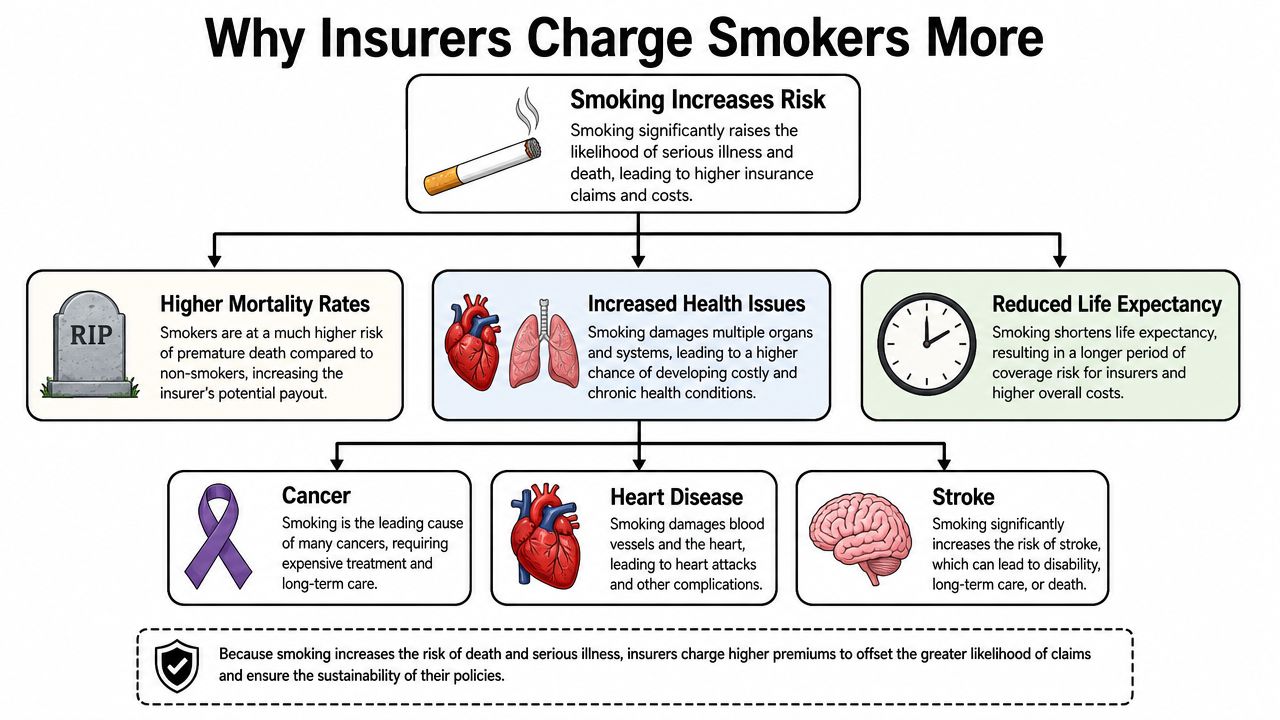

Why Smokers Pay More for Life Insurance

A life insurance policy is a promise to pay your family if you die while the policy is active. The insurer sets your price based on how likely that promise is to be used sooner rather than later. Smoking raises the chance of serious health problems over time, including heart disease, cancer, and lung disease, so smokers usually pay more.

A simple way to view it is this: the insurer is pricing probability, not passing judgment. Public health guidance from the Centers for Disease Control and Prevention on smoking and health effects explains why insurers treat tobacco use as a higher-risk factor.

That higher price can feel personal, especially if you're trying to protect a young family and get coverage in place quickly. But the useful takeaway is practical. If pricing comes from risk classification, then there is a process you can understand, shop around, and sometimes improve later.

If you want the mechanics behind that pricing, this guide to life insurance underwriting explains how insurers review an application.

How underwriters usually think

Underwriters review your full health picture. Tobacco use matters a lot, but it is one input among several. Age, blood pressure, prescriptions, past diagnoses, and family medical history can all affect the final offer.

The result is a rate class, which is the pricing bucket attached to your policy.

Common classes often include:

- Preferred Plus non-smoker: Reserved for applicants with very strong health profiles.

- Preferred non-smoker: Strong overall health with limited concerns.

- Standard non-smoker: Average health, without a tobacco classification.

- Preferred tobacco: Available with some insurers for applicants who are otherwise healthy.

- Standard tobacco: A common category for regular nicotine or tobacco users.

Carrier names vary, but the structure is similar. The insurer is sorting applicants into current risk groups, not assigning a lifelong label.

Why this matters for your options

Two smokers can get very different quotes. A person who uses nicotine but has stable health may be priced more favorably than someone with tobacco use plus diabetes, uncontrolled blood pressure, or a complicated medical history.

That distinction matters because it points to options, not just penalties. You may be able to get coverage now through a traditional policy or a digital no-exam policy, then revisit your rate if your health profile improves. And if you start smoking after your policy is already active, your existing premium usually does not automatically go up unless you apply for new coverage or ask the insurer to change the policy.

So the message here is straightforward. Smokers pay more because insurers see more risk, but coverage is still available, and the pricing rules are more flexible than many applicants expect.

How Insurers Define a Tobacco User

A lot of applicants hear "smoker" and picture a pack of cigarettes. Insurers usually use the term more broadly. In practice, they are asking a simpler question: has your body been getting nicotine or tobacco recently?

That difference matters. Someone who only vapes on weekends, uses nicotine gum, or has a few cigars a year can still be reviewed under tobacco rules. If your application includes lab work, the insurer may compare your answers with the results. If you want a plain-English overview of that process, this life insurance medical exam guide explains what carriers typically review.

What usually counts as tobacco or nicotine use

Carriers set their own underwriting rules, but these products commonly trigger extra scrutiny:

- Cigarettes: Regular use almost always leads to a tobacco classification.

- Cigars: Some insurers make room for rare cigar use, while others treat any recent use as tobacco.

- Vapes and e-cigarettes: Many carriers group nicotine vaping with other tobacco-related use, even if there is no smoke.

- Chewing tobacco or dip: Smokeless products still count.

- Nicotine replacement products: Patches, gum, or lozenges can matter because the insurer is often checking for nicotine exposure, not just smoking itself.

The "social cigar" issue confuses people more than almost anything else. A few insurers may allow non-smoker pricing for very limited cigar use if the rest of the health profile is strong and nicotine testing is clear. Others will not. The safe move is to answer the question exactly as asked and let the carrier decide which rule applies.

Why the nicotine test matters

Many exam-based policies test for cotinine, which is a byproduct of nicotine. That test works like a receipt. If the application says one thing and the lab result suggests another, the insurer may delay the file, change the rate class, or ask more questions.

This is why honesty protects you financially, not just ethically. A clean, accurate application gives you the best chance at keeping the process quick and avoiding problems later.

The look-back window is the real rule

The key question is usually not "Have you ever smoked?" It is "How recently have you used nicotine or tobacco?"

Insurers often use a look-back period to decide whether you qualify for tobacco or non-tobacco pricing. That period varies by company and product. Some want a full year without nicotine before reconsidering your status. Others may want longer, especially for the best non-smoker classes.

That can feel frustrating, but it also gives you a roadmap. Coverage is still available now, including digital and no-exam options with some carriers. Then, after you have been tobacco-free long enough, you can ask whether you qualify for a better rate. And if you start smoking after your policy is already in force, your current premium usually stays the same unless you apply for new coverage or request a change that requires new underwriting.

The better strategy is simple. Apply truthfully, get covered, and revisit your rate later if your habits change.

The Financial Impact of Smoking on Premiums

A higher smoker rate can look manageable when you only see the monthly bill. The full difference shows up when you stretch that cost across 10, 20, or 30 years, the same way a slightly higher car payment feels much bigger once you add up every payment on the loan.

For families buying life insurance, that is the part that matters. You are not just choosing a monthly premium. You are choosing the total cost of protecting your income, mortgage plan, childcare budget, and your family's day-to-day stability.

A side-by-side look

Rate examples often show a wide gap between tobacco and non-tobacco pricing for the same amount of coverage. Here is the comparison cited earlier for a $500,000, 20-year term policy:

| Applicant profile | Monthly premium |

|---|---|

| 30-year-old female non-smoker | $23.25 |

| 30-year-old female smoker | $65.75 |

| 30-year-old male smoker | $80.95 |

| 60-year-old female non-smoker | $194.16 |

| 60-year-old female smoker | $617.51 |

| 60-year-old male non-smoker | $268.04 |

| 60-year-old male smoker | $887.93 |

Two patterns stand out.

First, smoking can raise the premium sharply even at younger ages, when many parents are just trying to lock in affordable coverage while kids are small.

Second, the dollar gap usually gets much larger with age. Insurers are pricing two risks at once: the normal increase that comes with getting older, and the added health risk tied to tobacco use. Those risks stack on top of each other.

Why the total policy cost matters

Here is a simple way to read those numbers. A smoker rate is not just "a bit more per month." It can mean paying thousands more over the full term of the policy.

That matters because life insurance is a long-horizon product. If you buy a 20-year term policy at 30, you may keep that premium until 50. A higher rate today can stay with your budget through daycare years, school years, and the stretch when many families are also saving for emergencies, retirement, and college.

This is also why the conversation should not stop at the penalty. Coverage can still be worth buying now, even if the smoker class costs more. Going uninsured while waiting for a perfect rate can leave a much bigger financial hole than paying a higher premium for a few years.

What families should do with this information

Use smoker pricing as a planning tool, not a reason to give up.

- Get the right amount of coverage first. Protect income replacement, major debts, and your children's basic needs before worrying about getting the lowest possible rate class.

- Compare policy types and underwriting paths. Some applicants may prefer a traditional exam-based policy, while others may want a faster digital or no-exam option that gets coverage in force sooner.

- Build in a future rate check. If you later quit and stay tobacco-free long enough to qualify for review, you may be able to apply for a better class on new coverage.

- Know what happens after approval. If you start smoking after your policy is already active, your current premium usually does not change unless you apply for new insurance or make a policy change that triggers new underwriting.

That last point surprises a lot of people. Life insurance pricing is usually based on the information collected when the policy is issued. So the practical move for many young families is simple: get covered now, then improve the price later if your health habits change.

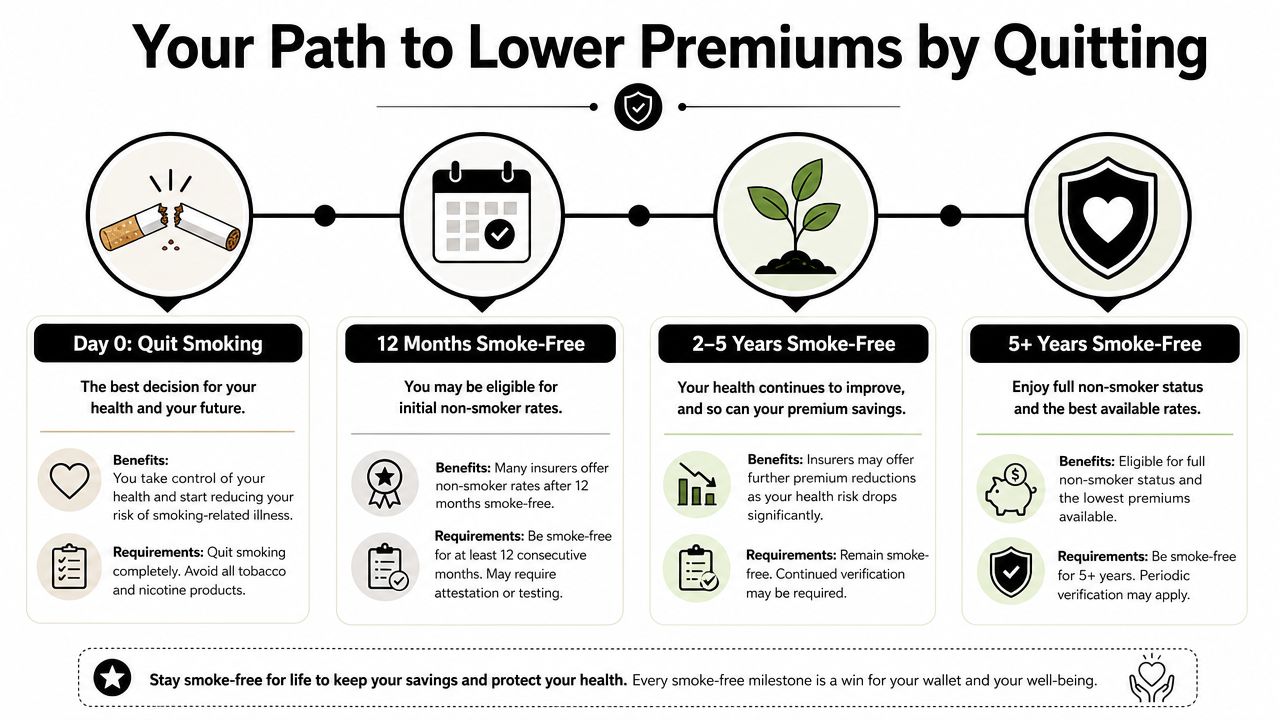

Your Path to Lower Premiums by Quitting

A lot of parents buy coverage while they still smoke, then ask the next practical question. "If I quit, can I ever get a better rate?" In many cases, yes.

Lower pricing usually does not happen the moment you stop. Insurers want a track record, because they price tobacco use based on sustained habits, not good intentions. A single smoke-free week is encouraging. A documented tobacco-free period is what usually matters for underwriting.

What the timeline usually looks like

The process works a lot like refinancing a loan after your credit improves. You do not get the new rate automatically. You first need enough time and evidence to show that the risk has changed.

For many insurers, one tobacco-free year is the first checkpoint for non-smoker consideration, as noted earlier. Some companies may want more time, and some may look closely at nicotine replacement products, vaping, or occasional cigar use. That is why the label "quit" can mean different things in practice.

A simple way to think about the timeline:

- Right now: Put coverage in force if your family needs protection today.

- After a sustained tobacco-free period: Ask whether you qualify for a review.

- After more time without nicotine or tobacco: You may have access to better rate classes, depending on the insurer and your overall health.

If speed matters while you work toward that review, a simplified issue life insurance policy can be one route to consider.

This short video gives a helpful overview of the process and what to expect when rates change after quitting:

How to ask for a better rate

This part trips people up. Your insurer usually will not lower the premium on its own just because time has passed.

You generally need to ask for a review, sometimes called reconsideration or re-rating. The company may request a statement with your quit date, updated health information, or a nicotine test. Some insurers can review the policy you already have. In other cases, a new application may produce a better result.

Use this checklist:

- Call the insurer or your agent: Ask whether your current policy is eligible for reconsideration.

- Confirm the waiting period: Get the company's tobacco-free requirement in writing if possible.

- Gather proof: Be ready to share your quit date and answer questions about any nicotine use.

- Complete any required testing: A new nicotine test or health review may be part of the process.

- Price both paths: Compare improving the current policy with applying for a new one.

A quick example helps. If you bought a policy two years ago as a smoker and quit shortly after approval, you may be in a much better position today than your original premium suggests. But the lower rate usually appears only after you ask the insurer to review your class.

Taking Control of Your Rates

Smoking status is usually a snapshot taken at underwriting. It is not always permanent.

That matters because quitting can change what is available to you later, even if you could not get a low rate at the start. For young families, that creates a practical roadmap. Get covered first. Build a documented smoke-free history. Then revisit your rate with clear evidence and a specific request.

That is a much better position than waiting uninsured for the "perfect" time to apply.

How to Shop and Apply for Coverage as a Smoker

Shopping for life insurance as a smoker works best when you stay honest and compare more than one path. Some applicants focus only on price and miss the approval details. Others focus only on speed and miss better long-term value. A balanced approach usually wins.

Two application routes to consider

The traditional route is fully underwritten life insurance. That may include health questions, medical records, and sometimes an exam. It can take more effort, but it may reward a healthier smoker with a better rate than a fast-track option.

The modern route is no-exam or simplified issue coverage. That can be convenient for busy families who want a digital application and faster decisions. If you're curious how that route works, this overview of simplified issue life insurance explains the basics.

No-exam coverage can still be useful for smokers, especially if speed matters or if you want to avoid scheduling an exam. The tradeoff is that pricing and coverage amounts may differ from fully underwritten policies.

The application rule that matters most

Be accurate about tobacco and nicotine use. This is not optional.

If an insurer asks whether you smoke, vape, chew tobacco, or use nicotine products, answer directly. If you had recent use, disclose it. If you only smoke cigars occasionally, say that clearly instead of forcing yourself into the wrong box.

A careful application usually follows this sequence:

- Gather your details first: Current nicotine use, quit history, medications, and basic health information.

- Compare carrier rules: Some insurers handle occasional cigar use more favorably than others.

- Pick the right underwriting path: Faster isn't always cheaper, and cheaper isn't always faster.

- Review the final offer in context: Look at premium, term length, death benefit, and whether the payment fits your monthly budget.

An honest application may feel expensive at first, but it protects the one thing that matters most. Your family's ability to collect the benefit if they need it.

What to prioritize

If your budget is tight, focus first on reliable coverage you can keep in force. A policy only helps if you can afford to maintain it. Once your health profile improves, you can revisit the decision and shop again.

Frequently Asked Questions About Smoking and Life Insurance

What happens if I start smoking after my policy is active

This is one of the most misunderstood parts of life insurance. If you were honest when you applied and your policy is already in force, your rate doesn't jump later just because your habits change. As Insure.com explains in its smoking and life insurance guide, "Your premium will stay exactly the same if you start smoking after the policy is already in force… Insurance companies do not re-check your tobacco status during the life of the policy."

Should I lie and say I'm a non-smoker to get a better rate

No. If the insurer discovers that the application was inaccurate, that can create serious problems. The better strategy is to buy the right policy with accurate information, then improve your classification later if you quit.

Can smokers still get no-exam coverage

Yes, in many cases they can. The tradeoff is usually about pricing, underwriting flexibility, and available coverage amounts. If speed matters, a no-exam route can still be a practical option.

Do occasional cigars count

They can. Some insurers are stricter than others. Occasional cigar use may be treated more favorably in limited cases, but regular use usually leads to smoker classification.

Is life insurance for smokers worth buying now or should I wait until I quit

If people rely on you financially, waiting can be risky. Coverage in force today may be more valuable than a lower premium you hope to qualify for later.

If you're ready to compare modern options for term coverage, Coveredly offers a digital-first way to explore life insurance that fits real life. For young families, newlyweds, and busy professionals who want simplicity, flexibility, and up to $3mm of term life insurance with no exams for most, it's a practical place to start.