You bought a home, signed a stack of closing papers, and finally got the keys. Then the mail starts. Some letters look urgent. Some look official. Some make it sound like you need to act right away to “protect your mortgage.”

If you're a new homeowner, that's a common moment of confusion. You're trying to figure out utilities, budgets, and where the box with the coffee maker ended up. Then a new question lands in your lap: Do I need mortgage protection insurance, or is this just another sales pitch?

That question matters because mortgage-related insurance isn't some tiny corner of finance. In 2020, 40.7% of all U.S. agency mortgage originations had some form of mortgage insurance, and private mortgage insurance issuance reached $4.7 billion, backing over $511 billion in mortgage loans, according to Urban Institute's mortgage insurance snapshot. So the offers in your mailbox are showing up in a very large market.

What matters most, though, isn't the mail. It's whether the product helps your family or mostly protects your lender. That's where many homeowners get tripped up, especially when people mix up MPI and PMI.

Table of Contents

- Your New Home and the Flood of Insurance Offers

- What Is Mortgage Protection Insurance Exactly

- The Pros and Cons of Mortgage Protection Insurance

- MPI vs Term Life Insurance A Clear Comparison

- How to Evaluate Mortgage Protection Insurance Companies

- A Smarter Alternative Protecting Your Family with Term Life

- Frequently Asked Questions About Mortgage Protection

Your New Home and the Flood of Insurance Offers

A lot of new homeowners have the same experience. You close on Friday, unpack on Saturday, and by the next week your mailbox has “final notice” style letters about mortgage protection. The wording can make it seem tied to your loan closing, almost like one more item your lender forgot to mention.

Usually, that's the first place people get uneasy. The offer feels personal because it mentions your mortgage. It feels important because it talks about losing the home. And it feels time-sensitive because the marketing is designed that way.

Here's the plain-English version. Mortgage protection insurance companies are selling a policy meant to deal with one specific problem: what happens to the mortgage if a covered event, often death and sometimes disability-related events depending on the policy, affects the borrower.

Most confusion starts because the mail looks like loan paperwork, but it's usually an insurance offer, not a mortgage requirement.

That doesn't automatically make it bad. A narrow product can still be useful. But it does mean you should slow down before signing anything.

For many young couples, the primary concern isn't “How do we protect the mortgage?” It's “How do we protect the family if one income disappears?” Those are related questions, but they are not the same question. A policy can solve the first one while doing a poor job on the second.

Why these offers keep showing up

Mortgage-related insurance is common enough that insurers know new borrowers are a large audience. That's why your home purchase often triggers a wave of marketing. New homeowners are financially vulnerable in a very specific way. They've just taken on a major debt, often at the same time they're building savings, planning for kids, or recovering from closing costs.

That's why you'll hear terms like mortgage life insurance, mortgage protection insurance, PMI, and lender protection in the same general conversation. They sound similar. They work differently. Untangling that is the first step to making a smart call.

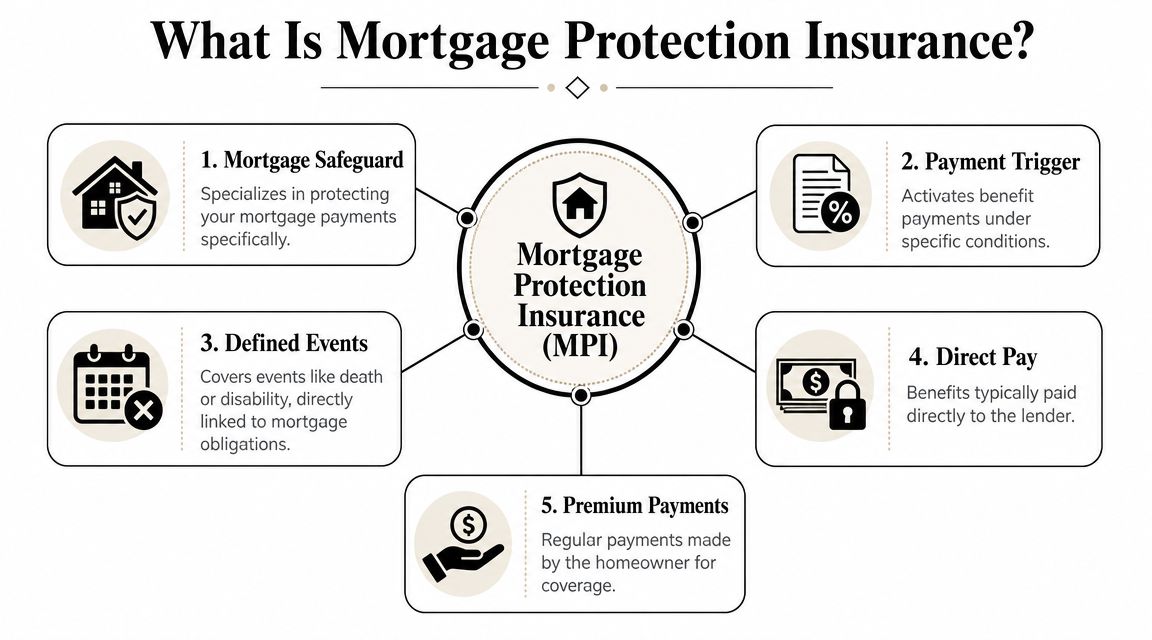

What Is Mortgage Protection Insurance Exactly

Mortgage protection insurance, often shortened to MPI, is best understood as a single-purpose policy. It's designed to handle the mortgage debt itself, not all the other financial consequences that can hit a household after a death.

Think of MPI as a single job policy

Think of MPI like a spare house key that opens only one door. It can be valuable for that one door. But if you need access to everything else in the house, it won't help.

In practice, MPI is typically structured as decreasing-term coverage. The payout is tied to your mortgage balance, so as you pay the loan down over time, the potential benefit falls too. The benefit is also usually paid directly to the lender, not to your spouse or another beneficiary, as explained in Chase's overview of mortgage protection insurance.

That lender-direct structure is important. If your partner dies, the mortgage may be paid off or reduced under the policy terms, but your household doesn't receive flexible cash for groceries, childcare, car payments, or time off work.

MPI is not the same thing as PMI

Many readers find this distinction challenging. MPI and PMI are not interchangeable.

- MPI is a voluntary insurance product meant to address the mortgage balance after a covered event.

- PMI means private mortgage insurance, and it generally protects the lender when a borrower puts down less than 20%.

They share the word “mortgage,” but they solve different problems for different parties.

Practical rule: If the policy's benefit goes straight to the bank, ask yourself whether you're buying protection for your family or protection for the loan.

That's why MPI can feel reassuring while still being limited. It's not fake protection. It's just specialized protection. For some households, that focus is enough. For many young families, it isn't.

The Pros and Cons of Mortgage Protection Insurance

MPI has real strengths. It also has limits that matter a lot once you think beyond the loan itself.

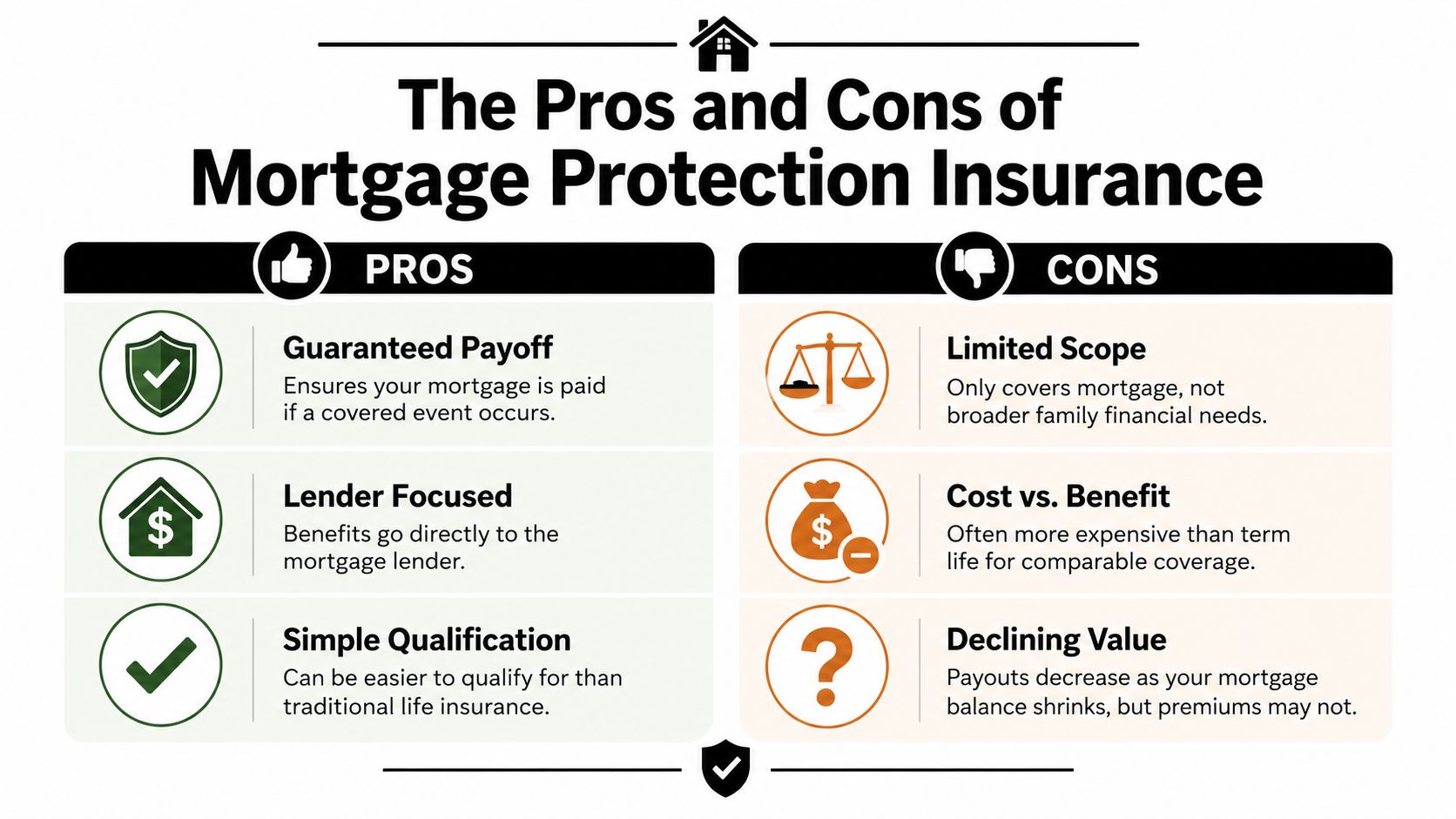

Where MPI can help

The biggest selling point is simple. If the covered event happens, the policy is built to deal with the mortgage. That can bring peace of mind to homeowners who care most about keeping the home in the family.

Some people also like the straightforward design. Instead of asking, “How much life insurance do we need for income replacement, debts, and future goals?” they focus on one fixed obligation. The policy is built around that debt.

There's another reason some shoppers stay interested. Certain mortgage protection insurance companies may appeal to people who want a simpler application path than a traditional fully underwritten life policy.

Where families often feel shortchanged

The weaknesses show up when you think like a household planner instead of a lender.

First, mortgage-related insurance in the housing market is often built around lender risk transfer. It becomes especially relevant when borrowers make smaller down payments. For example, Allstate's explanation of PMI notes that mortgage insurance protects the lender if foreclosure proceeds don't cover the loan, and purchase loans with PMI in 2020 had an average 93.1% loan-to-value ratio. That gives you the broader context. Mortgage insurance products often exist because loans with a high loan-to-value ratio create more lender risk.

That doesn't mean MPI is identical to PMI. It does mean you should pay attention to whose problem the product is primarily solving.

Here are the trade-offs families often miss:

- Limited flexibility: The money usually goes to the lender. Your family can't redirect it to whatever need is most urgent.

- Declining benefit: Your mortgage balance falls over time, so the policy value typically falls with it.

- Value mismatch: A shrinking payout can feel less appealing if premiums don't shrink in step.

- Narrow protection: Paying off a home loan is helpful, but it doesn't replace income or cover all the costs of raising a family.

A simple example helps. Suppose one spouse dies and the mortgage disappears. That sounds like the ideal outcome. But the surviving spouse may still face child care bills, reduced earnings, and ordinary living costs. The house payment might be gone, yet the financial pressure can remain intense.

MPI can be the right fit for someone who wants a targeted solution. It's much less compelling if what you really need is broad family protection.

MPI vs Term Life Insurance A Clear Comparison

This is the decision point most young homeowners care about. You're not just choosing between two policy names. You're choosing who gets the money, how flexible that money is, and whether the coverage still fits your life a few years from now.

The biggest difference is who controls the money

The most important difference is the beneficiary.

With MPI, the benefit is usually aimed at the mortgage and paid to the lender. With term life insurance, you typically choose the beneficiary, such as your spouse. That means your family controls the funds.

That flexibility matters. A surviving partner might decide the best move is to keep making the mortgage payment and use the rest for income support. Or they may pay down a large part of the loan, set aside money for child care, and keep an emergency cushion.

That's why many personal finance discussions miss a critical decision. As Bankrate's discussion of mortgage protection insurance points out, a key underserved angle is the direct cost-benefit comparison between MPI and a more flexible term life policy.

If you want a quick background on how decreasing coverage works, this guide to decreasing term life insurance can help clarify why a shrinking benefit is a very different setup from a level death benefit.

MPI vs Term Life Insurance at a Glance

| Feature | Mortgage Protection Insurance (MPI) | Term Life Insurance |

|---|---|---|

| Beneficiary | Usually the lender | Usually the person or people you choose |

| Payout flexibility | Limited to the mortgage obligation | Flexible. Can be used for the mortgage, income support, debts, or family expenses |

| Benefit structure | Commonly decreases with the mortgage balance | Often level for the term of the policy |

| Family control | Low | High |

| Best fit | Someone focused narrowly on retiring the home loan | Someone who wants broader financial protection for dependents |

If your goal is “make sure the bank gets paid,” MPI fits neatly. If your goal is “make sure my family has options,” term life usually fits better.

A young couple with a mortgage and one toddler is a good example. If one parent dies, the monthly mortgage is only one line in the budget. The surviving parent may need help covering time away from work, transportation, child care, counseling, or just breathing room while life gets reorganized.

That's why term life often wins the practical comparison, even before you get into pricing. It protects the roof, yes. But it also protects the people living under it.

How to Evaluate Mortgage Protection Insurance Companies

If you're still considering MPI, don't shop based on the mailer. Shop based on the company and the contract.

Start with company stability

This is one area where the market structure matters. The U.S. mortgage insurance market is concentrated. As of 2024, there were only six active private mortgage insurers approved to provide coverage for Fannie Mae and Freddie Mac mortgages, and mortgage insurers represented 54% of Fannie Mae's counterparty risk, according to the FHFA Office of Inspector General report.

That doesn't tell you whether a consumer MPI policy is right for you. It does tell you financial strength matters in this space.

When reviewing mortgage protection insurance companies, check:

- Financial strength ratings: Look up the insurer's rating history and what those ratings mean. This overview of life insurance ratings is a useful starting point if rating agencies are new to you.

- Policy design: Ask whether the premium stays level while the benefit declines.

- Portability: If you move, refinance, or pay off the loan early, find out what happens to the coverage.

- Exclusions and waiting periods: Read the situations where a claim may not pay as expected.

Questions to ask before you apply

A good insurance conversation should get more specific than “protect your home.”

Ask these questions in plain language:

Who receives the benefit?

If it's paid directly to the lender, make sure that matches your goal.Does the benefit fall over time?

Many policies are tied to the declining mortgage balance.Does the premium also fall?

This is one of the easiest value checks to make.What happens if we refinance or sell the house?

Life changes. Your policy should be clear about that.Are disability or job-loss features included, optional, or unavailable?

Don't assume every policy works the same way.Can I cancel the policy easily?

You want to know the process before you need it.

A strong insurance purchase should still make sense after the sales conversation ends and you reread the policy on your own.

One more practical filter helps. If the agent keeps steering every question back to the house, bring the conversation back to your family. That shift often reveals whether MPI is the right product or just the easiest one to pitch.

A Smarter Alternative Protecting Your Family with Term Life

For many newly married couples and young parents, term life insurance solves the bigger problem more cleanly. It gives your family money they can use where it's needed most, instead of locking the payout to one debt.

What real flexibility looks like

Take a simple household example. A couple buys a first home. They also have a car payment, student loans, one child in daycare, and one spouse who would struggle to cover everything alone if the other died.

In that situation, a term life policy gives the surviving spouse choices. They could pay off part or all of the mortgage. They could keep making the payment and use the remaining benefit to replace lost income. They could cover child care or build a reserve for the next several years.

That's what family protection looks like in real life. It's not just removing a loan from a spreadsheet. It's preserving breathing room during a terrible season.

If you're comparing options online, this guide on how to compare term life insurance rates can help you organize quotes without turning the process into guesswork. One digital option in this category is Coveredly, which offers online term life insurance designed for shoppers who want a simpler application experience.

A short explainer can make the distinction easier to visualize:

How to shop without getting overwhelmed

If term life sounds like the better fit, keep your decision simple.

- Match the term to the risk: Many homeowners want coverage that lasts through the years when the mortgage is largest and kids are still dependent.

- Protect people first: Start with the income and caregiving gap your family would face.

- Use the mortgage as one input: The home loan matters, but it shouldn't be the only thing driving the decision.

- Review beneficiary setup carefully: The value of term life is that your family controls the money.

The key idea is straightforward. MPI protects a debt. Term life can protect a household.

For a young family, that broader protection is often the better answer.

Frequently Asked Questions About Mortgage Protection

Is mortgage protection insurance required by my lender

Usually, no. Homeowners often confuse MPI with other mortgage-related insurance requirements. If your down payment was small, your loan may involve mortgage insurance tied to the lender's risk, but that is different from voluntarily buying an MPI policy.

Can I cancel an MPI policy if I buy term life later

Often, yes, but the answer depends on the policy contract. Before you enroll, ask the insurer how cancellation works, whether there are any restrictions, and how quickly coverage ends after you request cancellation.

What happens to MPI if I refinance or sell the house

That depends on the policy terms. Some policies are tied closely to the original loan. If you refinance, move, or pay off the mortgage early, the policy may no longer fit the new situation. Ask this question before buying, not after.

Can I have both MPI and term life insurance

Yes. You can own both if you want layered coverage. The better question is whether both are necessary for your budget and goals. Many families find one well-chosen term policy covers the broader need more efficiently.

Is MPI ever a reasonable choice

Yes. It can make sense for someone who wants a mortgage-focused policy and is comfortable with the fact that the benefit is generally directed to the lender. It can also appeal to shoppers who prefer a simpler, narrower product. But it's usually worth comparing that choice against term life before deciding.

What's the simplest way to decide

Ask one question: If something happens to me, do I want to protect the mortgage, or do I want to protect my family's full financial life? If your answer is the second one, term life deserves a close look.

If you want to compare coverage with a family-first lens, Coveredly offers online term life insurance quotes that can help you evaluate whether flexible life coverage makes more sense than a mortgage-only policy.