You're probably here because life is getting more real, in a good way. Maybe you're buying a home, combining bank accounts, getting married, expecting a baby, or realizing that if one of you vanished from the monthly budget, the other would be carrying a lot more than grief.

That's where term life insurance for couples starts to make sense. Not as a gloomy topic, but as a practical tool. It's one way to protect the life you're building together before a crisis forces those decisions onto you.

The hard part isn't usually deciding that coverage matters. It's figuring out which setup makes sense, how much coverage to buy, and what happens later if life changes. Health can change. Jobs can change. Relationships can change. A policy that looks simple today can feel very different years from now.

Table of Contents

- Securing Your Future Together

- Why Your Partnership Needs a Financial Safety Net

- The Core Decision Joint vs Two Individual Policies

- How Much Life Insurance Coverage Do Couples Need

- Navigating the Application and Underwriting Process

- Real-Life Scenarios for Modern Couples

- Frequently Asked Questions About Couples Life Insurance

Securing Your Future Together

A lot of couples first think about life insurance when they sign up for something else with a long timeline. A mortgage. A childcare plan. A bigger apartment. A move to one income for a while. Those milestones feel exciting, but they also create a simple question: if one person died during the years when the household depends on both partners, what would the survivor need to keep going?

Term life insurance is often the cleanest answer for that stage of life. It provides financial protection for a defined period, usually between 10 and 30 years, and it's significantly more affordable than permanent life insurance because its job is straightforward: it pays a death benefit if the insured dies during the active term, as explained by Guardian's overview of joint and term life insurance.

What term life insurance actually does

It's akin to putting guardrails around your biggest shared obligations.

If one of you dies during the term, the money can help the surviving partner stay in the home, keep paying bills, cover childcare, or protect long-term plans that were built around two people contributing in some way. It's not there to build cash value. It's there to protect your household during the years when the financial stakes are highest.

Practical rule: Buy coverage for the years when someone else would be financially exposed if you died.

That's why term life insurance for couples often fits young families, newly married couples, and professionals with loans or shared housing costs. You're not trying to solve every future financial question forever. You're trying to cover the stretch of life where a loss would hit the hardest.

Why this feels confusing at first

Couples usually get stuck on three things:

- Policy structure: Should you buy one joint policy or two individual policies?

- Coverage amount: How much is enough without overbuying?

- Future flexibility: What happens if health, jobs, or the relationship itself changes?

Those questions matter more than the initial quote on a screen. The cheapest-looking option today isn't always the one that protects you best later.

Why Your Partnership Needs a Financial Safety Net

Life insurance becomes easier to understand when you stop thinking about it as a product and start thinking about the bills and responsibilities that would remain if one partner died.

For many couples, the first financial shock would be lost income. If one person pays most of the mortgage, covers childcare, funds savings, or keeps the household stable, the surviving partner may need time and money to adjust. That's why a key underwriting guideline is simple: if one spouse relies on the other's income to maintain their lifestyle, the working spouse should have term life insurance, according to New York Life's guidance for couples.

What the death benefit is really protecting

A policy payout can help with real obligations, not abstract ones.

- Housing costs: A surviving partner may need help keeping up with the mortgage or rent.

- Shared debt: Car loans, private loans, or other obligations don't disappear just because one borrower dies.

- Children's needs: Childcare, schooling, and day-to-day expenses can continue for years.

- Breathing room: The surviving partner may need time off work, flexibility to move, or a financial cushion while making major decisions.

That breathing room matters more than people expect. Grief is hard enough without having to decide, in the same month, whether to sell the house or drain savings.

A strong policy doesn't just replace income. It buys time, options, and stability for the person left behind.

When couples underestimate the need

Young couples often assume they can wait because they're healthy or because they don't have children yet. But a couple can already be financially intertwined long before kids enter the picture.

Consider a few common situations:

| Shared situation | Why coverage matters |

|---|---|

| One partner earns more | The surviving partner may struggle to maintain the same standard of living |

| Both names are on the mortgage | The home may become unaffordable on one income |

| One partner paused work | The household may depend heavily on the working spouse |

| You share debts or support family | The survivor may inherit financial pressure at the worst possible time |

The emotional side is practical too

It's easy to think, “We'd figure it out.” Most couples would. But figuring it out under stress often means rushed decisions. Selling investments too soon. Moving unexpectedly. Taking on extra debt. Pulling children out of routines that were working.

That's why I frame term life insurance for couples as part of a family protection plan, not a paperwork exercise. The point isn't fear. The point is making sure love and responsibility are backed by a financial plan.

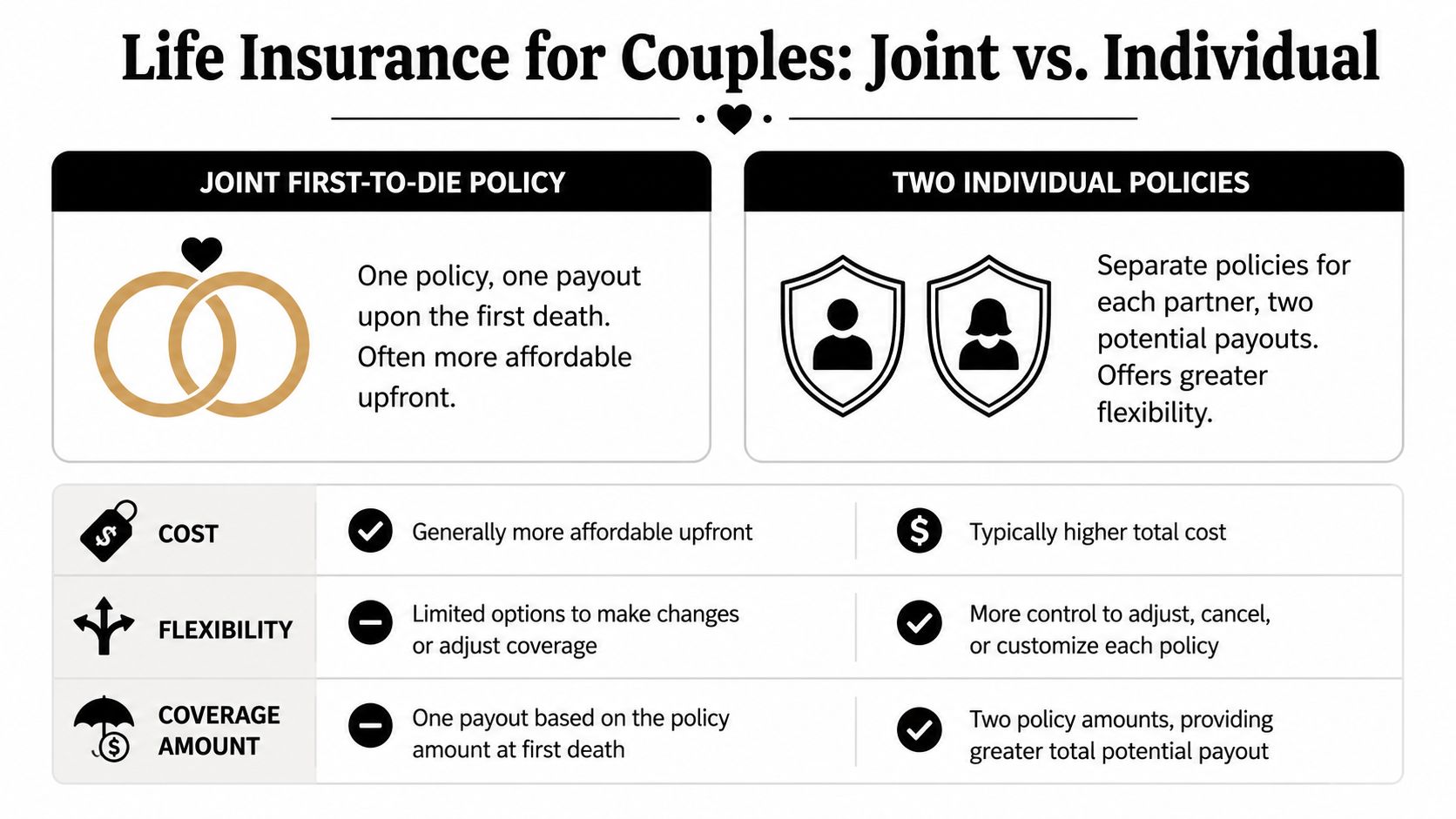

The Core Decision Joint vs Two Individual Policies

A lot of couples start here because the structure you choose affects more than the monthly premium. It affects how much control you keep later if life goes off script.

You usually have two paths. A joint first-to-die policy puts both partners on one contract and pays one death benefit after the first death. Two individual policies means each partner has their own coverage, their own beneficiary setup, and their own options.

Joint Policy vs. Two Individual Policies at a Glance

| Feature | Joint First-to-Die Policy | Two Individual Policies |

|---|---|---|

| Coverage structure | One policy covering both partners | One policy per partner |

| Payout | One death benefit after the first death | Each policy can pay its own death benefit |

| Upfront cost | May be lower initially | Often better tailored to each person |

| Pricing basis | Combined or blended risk | Each person's own age, health, and gender |

| Flexibility | Limited if needs change separately | High flexibility for each partner |

| Best fit | Narrow situations where simplicity matters most | Most couples who want long-term control |

One quick point that trips people up: first-to-die and second-to-die are not the same thing. First-to-die is designed to protect the surviving partner after one spouse dies. Second-to-die usually pays after both insured people have died, so it is more often used in estate planning than income protection.

Why two separate policies fit more real-life situations

For many couples, separate coverage is easier to price fairly and easier to manage over time. If one partner is younger, healthier, or needs a different amount of coverage, individual policies let the insurer evaluate each person on their own profile. Policygenius explains this well in its guide to life insurance for spouses.

A simple way to picture it is this: a joint policy bundles two people into one decision. Two individual policies keep each person's coverage in their own lane.

That difference matters most when life changes.

- If one partner develops a health condition later, the other partner's policy is unaffected.

- If one partner needs more coverage, they may be able to buy more without changing the other person's policy.

- If your term needs differ, one partner can choose 20 years while the other chooses 30.

- If divorce happens, separate policies are usually far easier to sort out than one shared contract.

This long-term flexibility is the dividing line. A joint policy can feel neat and simple on day one. Two individual policies are often easier to live with in year five, year ten, or during a major life change.

Joint coverage still has a place. Some couples prefer one policy to track, one premium to pay, and one death benefit aimed at protecting the surviving spouse after the first loss. But simplicity at purchase is not the same as flexibility later. If your finances, health, or relationship status changes, one shared policy can give you fewer good options.

If you're wondering whether more than one policy is allowed, this guide on having two life insurance policies shows how separate coverage can work in practice.

A quick explainer can make this easier to visualize:

How Much Life Insurance Coverage Do Couples Need

After choosing structure, the next question is the one almost everyone asks: How much coverage do we need?

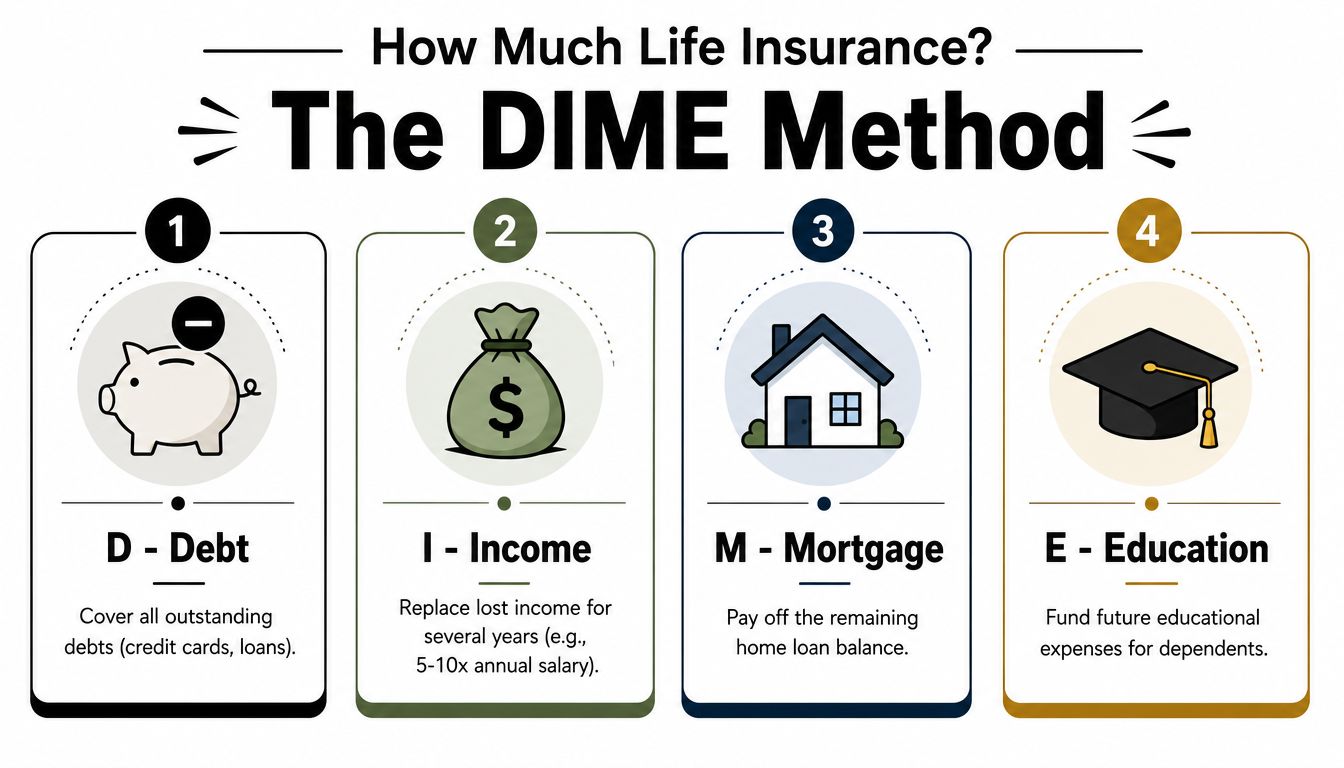

You don't need a perfect formula to get close. You need a method that forces you to look at the financial obligations a surviving partner would inherit. One of the easiest ways to do that is the DIME method: Debt, Income, Mortgage, and Education.

A simple way to estimate coverage

Start by writing down four buckets:

- Debt: Credit cards, personal loans, auto loans, and any other balances you'd want cleared.

- Income: How long would the surviving partner need support to replace lost earnings?

- Mortgage: Would you want the home paid off, or at least significantly easier to keep?

- Education: If you have children, what future schooling costs do you want to protect?

This framework helps because it turns a vague question into several smaller ones. Instead of asking, “How much life insurance should I buy?” you ask, “What would my partner need if I were gone next year?”

Don't choose a number because it sounds big or small. Choose it because it connects to actual obligations.

If you want a second opinion while you estimate, this guide on how much life insurance you need can help you pressure-test your math.

Two examples that show how this changes by life stage

Example one: a young family with one primary income

One spouse earns most of the household income. The couple has a mortgage, one child, and monthly bills that are hard to cover on the lower income alone.

Their thinking might look like this:

- Add debts they'd want erased quickly.

- Estimate several years of income replacement so the surviving spouse isn't forced into immediate major changes.

- Include enough for the mortgage so the family can stay in the home.

- Add future education needs for the child.

This household usually needs more coverage on the primary earner, but not necessarily the same amount on both spouses. The stay-at-home or lower-earning spouse may still need meaningful coverage because replacing childcare, household labor, and scheduling support can be expensive even if it doesn't show up as a salary.

Example two: a dual-income couple without children

This couple rents, both work full time, and they carry student debt. They don't need to fund childcare or college savings, but one death would still change the entire budget.

Their DIME approach might focus more on:

| DIME category | Priority for this couple |

|---|---|

| Debt | High |

| Income replacement | Moderate to high |

| Mortgage | Not relevant if renting |

| Education | Low or none for now |

Because both partners earn, they may choose separate coverage amounts tied to what each person contributes to shared expenses. The goal isn't making the survivor wealthy. It's making sure one loss doesn't become a financial collapse.

Coverage needs aren't static, either. Marriage, a home purchase, a child, or one partner stepping back from work can all change the right number.

Navigating the Application and Underwriting Process

You and your partner sit down to apply, and suddenly the questions feel more personal than expected. Health history. Income. Beneficiaries. Ownership. It can feel like filling out paperwork for your future selves.

That feeling is normal. The insurer is trying to answer a simple question: how much risk is involved in covering each person, and what policy setup makes sense on paper. Once you know what they're looking for, the process feels much less mysterious.

What the application usually involves

If you choose two individual term policies, each partner fills out a separate application. That may sound like extra work, but it often creates a cleaner setup later. Each person has their own contract, their own coverage amount, and more control if life changes.

Applications usually ask for:

- Basic personal details: age, address, job, and household information

- Health history: current conditions, medications, past diagnoses, and tobacco use

- Lifestyle factors: hobbies or work risks that may affect pricing

- Coverage choices: term length, coverage amount, and beneficiary decisions

Some applicants complete a medical exam. Others qualify for accelerated or no-exam underwriting. The path depends on the insurer, the amount of coverage, and the applicant's profile.

Accuracy matters more than perfection. If something seems small, disclose it. A life insurance application works a bit like building a house on a foundation. If the facts are solid at the start, the policy is more likely to hold up the way you expect later. For a clearer look at what happens behind the scenes, read this guide to life insurance underwriting and how insurers assess risk.

Questions to ask before you apply

Many couples focus on the monthly premium first. That makes sense, but price is only one part of the decision. The better question is whether the policy will still work well if your lives stop moving in perfect sync.

Ask these before you sign:

- Can each person adjust or keep coverage on their own later?

- Can one partner convert to permanent insurance without affecting the other?

- Can you choose different term lengths if your responsibilities are different?

- Who owns the policy, and who has the right to make changes?

These questions matter most when life gets uneven. One partner may develop a health condition. One may want coverage longer. One may leave work to care for a child. A joint policy can look neat at the beginning, but separate policies often give a couple more room to adapt without turning one decision into a shared negotiation every time something changes.

Divorce is the clearest example. A joint policy can leave two people connected by one contract long after their financial goals have split apart. Two individual policies usually avoid that problem. The same logic applies if one person wants to keep coverage, increase it, or convert it later while the other does not.

A good policy is not just affordable today. It should still make sense if your relationship, health, or income looks different five or ten years from now.

Real-Life Scenarios for Modern Couples

Advice sticks better when you can see yourself in it. Here are two common ways couples apply these decisions in real life.

A newly married couple with a first home

Maya and Chris just bought their first house. Both work, but Chris earns more and would be the one covering most of the mortgage if Maya died. Maya, on the other hand, handles a lot of the household planning and would need replacement income support if Chris died.

They initially liked the idea of one joint policy because it sounded tidy. One application. One bill. One decision.

After comparing the options, they chose two individual term policies. They wanted different coverage amounts based on income and obligations. They also wanted the freedom to revisit their own policies later if one of them changed jobs, developed a health condition, or needed a longer term.

Their main question wasn't “What's the easiest setup today?” It was “What will still work if life gets messy?”

Parents protecting income and future education

Lena and Jordan have two young children. Jordan earns more, but both incomes matter. If either parent died, the survivor would face not just income loss but also childcare disruption, future education planning, and pressure on everyday routines.

They used a DIME-style calculation to estimate coverage. Jordan's policy focused heavily on income replacement and housing stability. Lena's policy also mattered because replacing her contribution to childcare and family logistics would cost money, even beyond salary comparisons.

Families often discover that both adults need coverage, even when one income is lower.

They also chose separate policies because they didn't want one death to exhaust the household's entire protection plan. With individual coverage, each life is insured on its own terms, and each policy can stand on its own if circumstances change later.

Frequently Asked Questions About Couples Life Insurance

Can unmarried couples get life insurance together?

Yes, but joint coverage can be harder. Unmarried couples can generally buy life insurance, but they may need to prove insurable interest, meaning there would be a financial impact if one partner died. That can create a higher barrier for joint policies, which is one reason separate policies are often the more reliable route, as explained in Progressive's article on life insurance for couples.

What happens if we get divorced?

This is one of the strongest arguments for separate policies. Each person keeps control of their own policy, beneficiary decisions can be updated, and there's less need to negotiate a shared contract after the relationship ends. A joint policy can be more complicated because both people are tied to the same agreement.

What if one of us is uninsurable?

That doesn't automatically mean the other person should go without coverage. The insurable partner can still apply for an individual policy. In some households, that's the most important policy to get in place first, especially if one income supports most of the family's monthly obligations.

Should both spouses have the same coverage amount?

Not always. Coverage should reflect financial impact, not fairness in the abstract. Some couples need equal amounts. Others don't.

If you're ready to compare options without the usual friction, Coveredly offers online term life insurance designed to be digital, affordable, and flexible, with up to $3mm of term coverage and no exams for most. It's a practical place to explore coverage that fits the life you're building together.