A surrender charge is a penalty fee that usually ranges from 0% to 10% of a policy's cash value when you cancel certain life insurance policies or annuities early. It's the kind of fee you need to understand before you buy, because it can change how much money you can access if life takes an unexpected turn.

A lot of young families run into this question at the exact moment they're already stressed. A job change hits. A car repair shows up. Childcare costs jump. You start looking at every account and every policy, wondering what's available if you need cash now.

That's where confusion starts. Many people hear the word “life insurance” and assume all policies work the same way. They don't. Some policies build cash value and may come with surrender charges. Others, especially term life insurance, usually don't. That difference matters if flexibility is high on your priority list.

This guide breaks down what a surrender charge is, why insurers use it, how a surrender schedule works, how to calculate the actual impact, and how to avoid unpleasant surprises. The goal is simple. Help you read the fine print with confidence and choose coverage that fits your life, not the other way around.

Table of Contents

- Introduction

- What Is a Surrender Charge and Why Does It Exist

- Decoding the Surrender Charge Schedule and Period

- A Real-World Surrender Charge Calculation

- Strategies to Avoid or Minimize Surrender Charges

- The Simplicity of Term Life Insurance A Comparison

- Frequently Asked Questions About Surrender Charges

Introduction

If you're asking what is a surrender charge, you're probably not asking out of curiosity. You're likely trying to make a practical decision. Maybe you're shopping for life insurance. Maybe you already own a policy and want to know what happens if you cancel it.

The key point is that a surrender charge can act like a roadblock between the cash value shown on your statement and the amount you'd receive. That surprises people because the number they see on paper doesn't always equal the cash they can take home.

For a young family, that gap matters. You may be trying to balance mortgage payments, emergency savings, and protection for your spouse or children. A product that looks flexible at first glance can feel much less flexible if early access comes with penalties.

Practical rule: If a policy builds cash value, ask what happens if you need to exit early. If it doesn't build cash value, that question often disappears.

That's why this topic matters before purchase, not just after. The smartest time to learn about surrender charges is when you're comparing options, not when you're already filling out cancellation forms.

What Is a Surrender Charge and Why Does It Exist

A surrender charge is a fee charged when you cash out a cash-value life insurance policy or annuity before the contract's penalty period ends. According to US Legal Forms' explanation of surrender charges, it typically ranges from 0% to 10% of the cash value and exists mainly to help the insurer recover upfront commissions and administrative costs.

That's the formal answer. The plain-English answer is simpler. It works a lot like an early termination fee on a long-term contract. The insurer spent money to issue and service the policy, and the surrender charge helps the company recover part of that cost if you leave early.

Which products usually have this fee

Surrender charges usually show up in products that have a cash value component. That often includes:

- Whole life insurance, because it builds cash value over time

- Universal life insurance, for the same reason

- Variable life insurance, which also has cash value

- Annuities, especially deferred contracts designed for long-term use

Term life insurance usually doesn't fit into that group because it generally doesn't build cash value.

Why insurers structure it this way

Insurance companies price these products around a long holding period. They expect the contract to stay in force long enough for the economics to work. When someone cancels early, the company loses time to recover what it spent setting up the policy.

That's why the fee isn't random. It's tied to the idea that these products are built for longer-term protection or accumulation, not quick in-and-out access.

A short video can make that idea easier to visualize.

The easiest way to think about a surrender charge is this. The policy may have value, but that doesn't always mean all of that value is available today.

That distinction clears up a lot of confusion. People often focus on the promise of cash value and miss the access rules attached to it.

Decoding the Surrender Charge Schedule and Period

The two terms that matter most are surrender period and surrender schedule.

The surrender period is the span of years during which the fee can apply. The surrender schedule is the year-by-year list of what percentage the insurer charges if you exit during that period. Those percentages usually decline over time.

What the timeline usually looks like

A common pattern is a sliding scale. The fee starts higher in the early years, then drops each year until it reaches zero. The idea is straightforward. The longer you keep the contract, the less penalty applies if you leave.

According to the Insurance Information Institute's overview of surrender fees, annuity surrender schedules often follow this pattern:

| Policy Year | Surrender Charge |

|---|---|

| Year 1 | 7% |

| Year 2 | 6% |

| Year 3 | 5% |

| Year 4 | 4% |

| Year 5 | 3% |

| Year 6 | 2% |

| Year 7 | 1% |

| Year 8 onward | 0% |

That table gives you a practical benchmark, not a universal rule for every contract. Your own policy controls what applies.

Why the schedule matters so much

The schedule tells you whether waiting could materially change your result. If you're close to the end of the surrender period, even a short delay may reduce or eliminate the fee. If you're early in the contract, leaving may cost more than you expect.

This is why you should look beyond the phrase “cash value.” A statement can show a healthy cash value number while the surrender schedule limits what you can receive today.

One area that often confuses buyers

Some people assume surrender charges are flat. They usually aren't. A declining schedule means timing matters. Year 2 and Year 7 can lead to very different outcomes, even if the policy is otherwise the same.

Key question to ask: “What is my surrender charge today, and when does it go to zero?”

That single question can save a lot of frustration.

Another wrinkle is that product types aren't always handled the same way. The Investor.gov glossary entry on surrender charges notes a standard benchmark schedule of 7% in year one, 6% in year two, 5% in year three, 4% in year four, 3% in year five, 2% in year six, 1% in year seven, and 0% thereafter, and it also explains that a free look period typically lasts 10 to 30 days. That free look period can give you a short window to cancel without penalty right after purchase.

For families comparing products, the big takeaway is this. Don't just ask whether there's a surrender charge. Ask how long it lasts, how it declines, and what year you're in right now.

A Real-World Surrender Charge Calculation

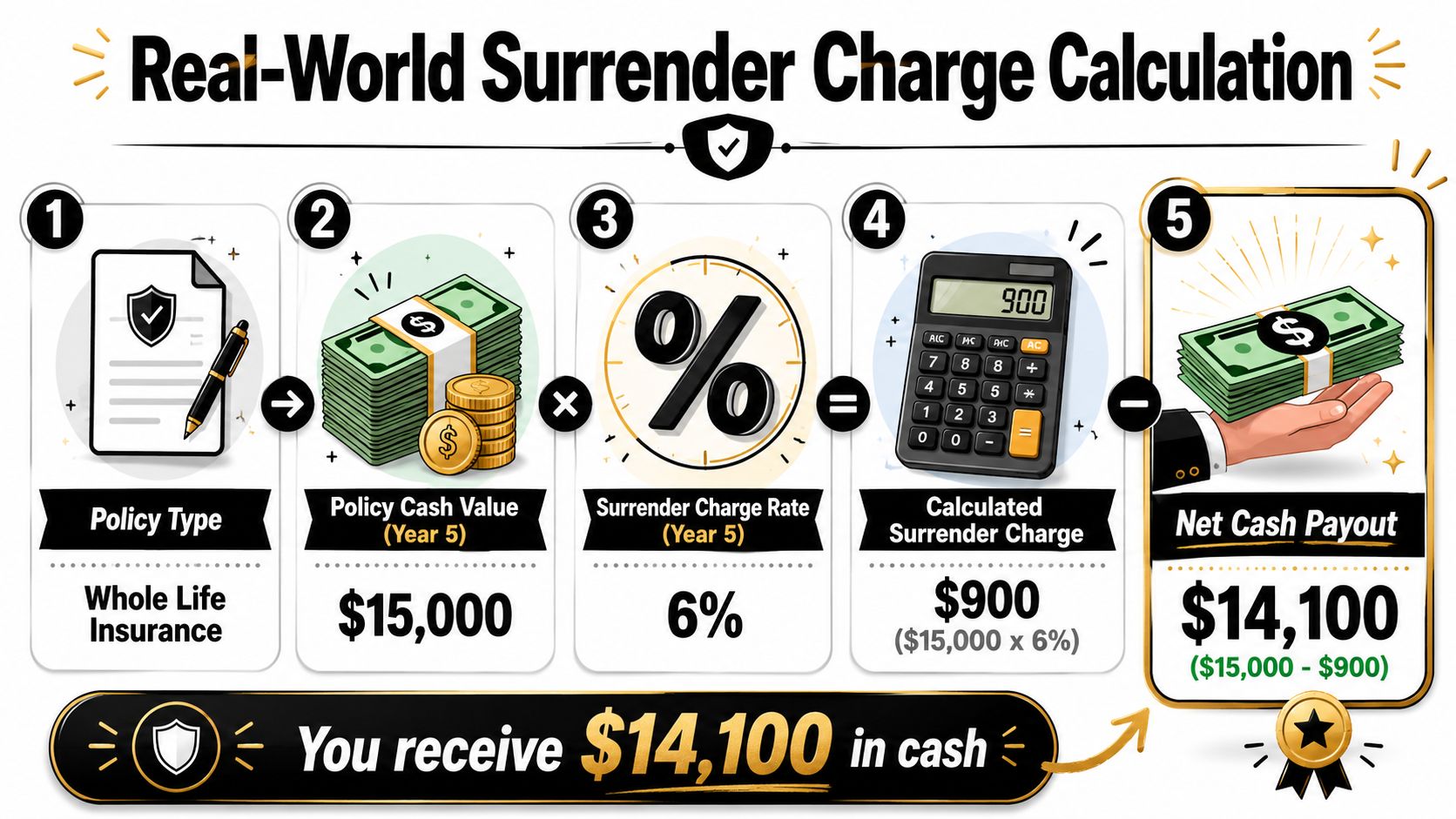

Percentages can feel abstract until you run the math. So let's use a simple example.

Suppose you own a whole life policy with a cash value of $15,000. You're thinking about canceling it while the contract still has a 6% surrender charge. Your first question is obvious. How much would you get?

Step-by-step math

Here's the calculation:

- Start with the cash value: $15,000

- Apply the surrender charge rate: 6%

- Calculate the charge: $15,000 × 6% = $900

- Subtract the charge from cash value: $15,000 – $900 = $14,100

So the net payout is $14,100, before accounting for any policy loans or loan interest.

The formula that matters

The full formula is straightforward. According to Western & Southern's explanation of cash surrender value, Cash Surrender Value = Cash Value – Surrender Charges – Outstanding Loans & Interest.

That last part matters more than many people expect. If you borrowed against the policy earlier, your actual payout could be lower than the simple example above.

If you want to get a better feel for how cash value works before surrender charges come into play, a cash value life insurance calculator can help you see how these moving pieces fit together.

The number on the statement is only the starting point. The usable number is the cash surrender value after charges and any loans are deducted.

That's why surrender charges feel so frustrating when people first encounter them. They aren't always visible in the headline number. You have to calculate what's left after the policy's rules are applied.

Strategies to Avoid or Minimize Surrender Charges

A common family-money problem goes like this. You bought a policy or annuity for the long term, then life changed faster than the contract did. A job loss, new baby, home repair, or better coverage option can make you want access to your money now. That is when surrender charges hurt most.

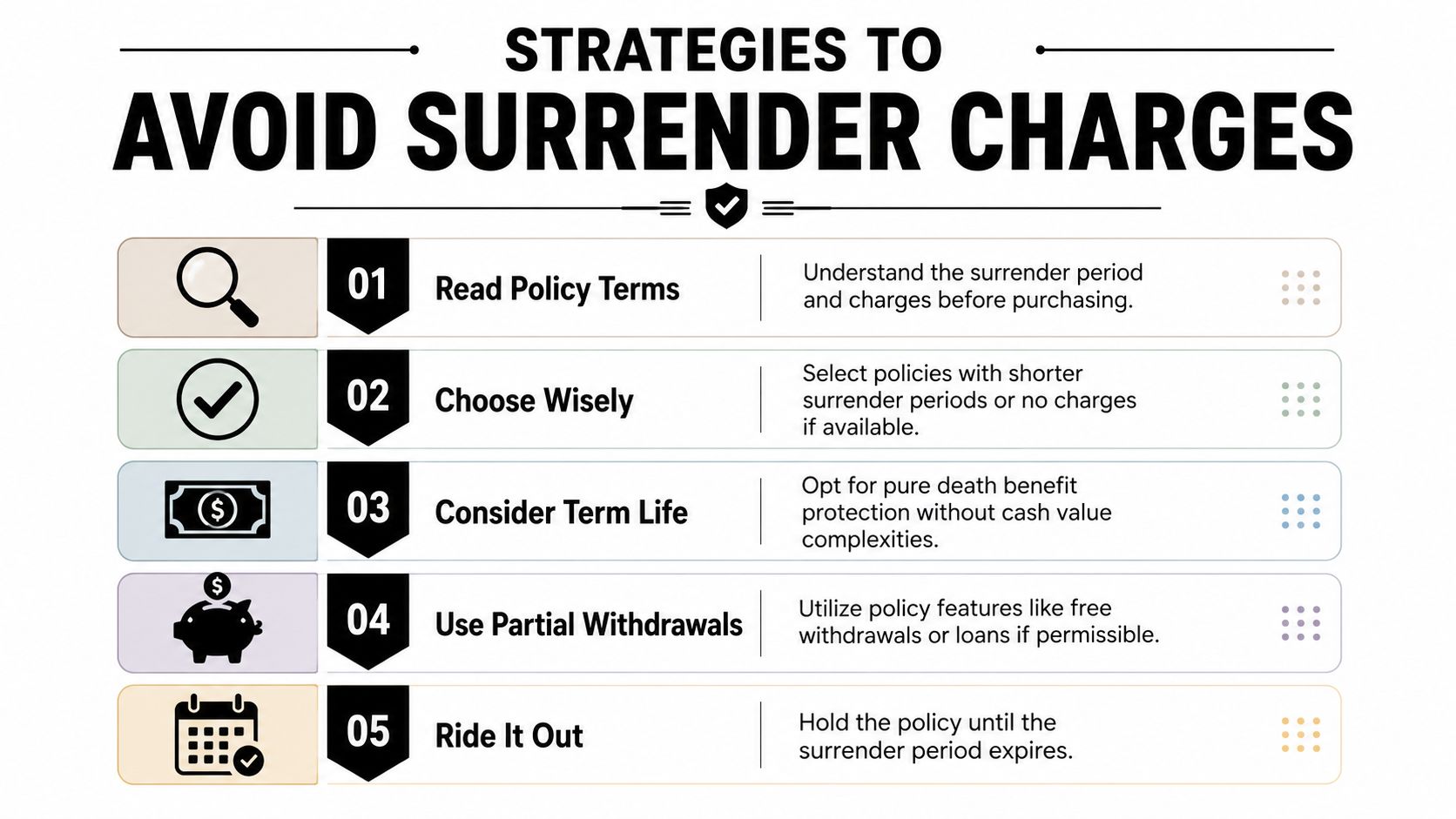

The good news is that a surrender charge does not always force an all-or-nothing decision. Many contracts give you smaller off-ramps. The key is to slow down and compare the cost of leaving now against the cost of staying longer.

Start with the lowest-risk options

Before you surrender anything, check these items in order:

- See how much time is left in the surrender period: If the charge falls each year, waiting even a few months could reduce what you lose.

- Use the free-look window if the policy is brand new: As noted earlier, Investor.gov explains that this cancellation period is often 10 to 30 days.

- Ask whether limited withdrawals are allowed: The FINRA investor alert on deferred annuities explains that some annuities let you withdraw a set amount each year without paying the full surrender charge.

- Review loans or partial withdrawals carefully: With some permanent life insurance policies, taking part of the value may cost less than canceling the policy.

- Call the insurer and ask for the actual surrender value in writing: That number is more useful than guessing from your statement.

This works a lot like an early exit fee on a long phone contract. Full cancellation may cost the most. A smaller change may cost less.

Pay close attention to "partial access"

Families often get tripped up. A contract may sound flexible, but the flexibility can be narrow. A free-withdrawal feature might apply only once a year, only up to a certain percentage, or only if the account has been open long enough.

The U.S. Securities and Exchange Commission's investor bulletin on annuities notes that variable annuities often allow limited penalty-free withdrawals, but the contract terms control how much you can take and when. In plain English, "you can access some money" is very different from "you can take out whatever you want."

That distinction matters most in emergencies.

Match the strategy to the product

If you own permanent life insurance or an annuity, surrender charges are part of the tradeoff for having cash value or tax-deferred growth features. You need to read the exit rules as carefully as the benefits.

If your main goal is to protect your family income, flexibility usually looks very different. Term life insurance generally avoids this problem because there is no cash value account to surrender. That means fewer moving parts and fewer surprise exit penalties if your needs change later.

For households that no longer want to keep a permanent policy, canceling is not the only path. This guide on how you can sell a life insurance policy explains another option that may be worth reviewing before you give the policy back to the insurer.

The best way to reduce a surrender charge is to avoid triggering one before you understand your contract, your timing, and your alternatives.

Calm, careful review saves money here. Fast decisions usually do not.

The Simplicity of Term Life Insurance A Comparison

Here's the part many buyers find reassuring. Term life insurance usually doesn't have surrender charges. The reason is simple. Term policies generally don't build cash value, so there isn't a cash-value account to surrender.

That makes term life much easier to understand if your main goal is protection for your family, not a product with an investment-style component.

Where people mix this up

Many consumers hear stories about surrender fees and assume they apply to all life insurance. That's not true. According to Thrivent's explanation of annuity surrender periods, around 90% of term life policies have no surrender fees because they lack a cash value component, while 95% of annuities do include them.

That difference is a major reason term life feels cleaner for many households. You're paying for a death benefit over a set period, not navigating cash value, surrender schedules, and withdrawal provisions.

Side-by-side practical difference

| Product Type | Cash Value | Surrender Charge Risk | Main Use |

|---|---|---|---|

| Term life insurance | No | Usually no | Income protection for a set term |

| Permanent life insurance | Yes | Can apply | Lifelong coverage with cash value |

| Annuity | Yes or account value component | Often applies | Long-term income or accumulation |

This doesn't mean permanent life or annuities are “bad.” It means they solve different problems. If you want simplicity, affordability, and freedom from hidden exit penalties, term life often lines up better with that goal.

For readers comparing protection-first options, this term life insurance guide is a useful next step.

For many young families, the smartest form of flexibility is choosing a policy that doesn't create an exit penalty in the first place.

That's often the cleanest answer to the surrender charge question. Pick a product designed for straightforward protection if that's what you need.

Frequently Asked Questions About Surrender Charges

Are surrender charges tax-deductible

Tax treatment depends on your situation, and this is one area where it's wise to speak with a qualified tax professional. The safe takeaway is not to assume a surrender charge creates a straightforward tax deduction just because it reduced your payout.

What happens to a surrender charge if the insured person dies

A surrender charge generally matters when someone cancels a qualifying policy early to access cash value. If the insured person dies while the coverage is in force, the conversation usually shifts to the policy's death benefit rather than a surrender payout. In practical terms, surrender charges typically become irrelevant because the policy wasn't surrendered.

Is surrendering the only way to get value from a policy you no longer want

Not always. In some situations, people explore alternatives such as partial withdrawals, loans, or a life settlement. A life settlement is more complex than canceling a policy, and it isn't the right fit for everyone, but it can come up when someone no longer wants or needs coverage and wants to examine options before giving the policy back to the insurer.

The bigger lesson behind all three questions is simple. Don't treat “cancel the policy” as your only move until you've checked the contract and considered the consequences carefully.

If you want life insurance that's straightforward, digital, and built for real-life flexibility, Coveredly is worth a look. Coveredly offers online life insurance designed for busy families and professionals, with up to $3mm of term life insurance and no exams for most, so you can focus on protecting the people you love without getting buried in unnecessary complexity.