If you're buying life insurance because people depend on you, or because your business would take a hit if a key person died, you've already grasped the heart of insurable interest. The term sounds legal and stiff. The idea is practical.

Think of a newly married couple with a mortgage, or two co-founders building a company. In both cases, one person’s death would create a real loss for the other. Life insurance is built for that kind of risk. It isn't supposed to be a bet on someone else's life.

That’s why people ask, what is insurable interest in life insurance? The short answer is simple. It’s the rule that says you need a real reason, usually financial or close family-related, to take out a policy on another person.

Table of Contents

- What Is Insurable Interest in Plain English

- Why Insurable Interest Is a Safeguard Not a Hurdle

- When and How Insurable Interest Applies

- Real-World Examples Who Has Insurable Interest

- How to Document Insurable Interest

- Legal Implications and Common Mistakes

- Secure Your Future with Confidence

What Is Insurable Interest in Plain English

Insurable interest means you would suffer a real loss if the insured person died.

View it as a permission slip. If you want to buy a life insurance policy on someone else, the law and the insurer want proof that your connection is legitimate. You can't just choose any person and insure them because their death would pay money.

This makes intuitive sense fast.

If your spouse dies, you may lose income, childcare support, or help paying the mortgage. If your business partner dies, the business may lose leadership, revenue, or the ability to carry out contracts. Those are real stakes. That is insurable interest.

If a casual acquaintance dies and their death wouldn't affect your finances or create a recognized close-family loss, there usually isn't insurable interest. The policy would start to look less like protection and more like speculation.

Think of it this way

Life insurance works best when it protects something valuable that's already there:

- A household income

- A family responsibility

- A business relationship

- A loan or debt obligation

That’s why the rule matters. It keeps the purpose of life insurance tied to protection.

Simple rule: If the person’s death would leave you with a genuine loss, you may have insurable interest. If their death would mainly create a payout without a real loss, that’s a red flag.

People often get tripped up by the wording, not the concept. The phrase sounds technical. The everyday meaning is straightforward. It answers one question: Do you have a valid reason to insure this person’s life?

Why Insurable Interest Is a Safeguard Not a Hurdle

Some people hear this rule and think it’s just one more insurance roadblock. It isn’t. It’s one of the main reasons life insurance can stay focused on protecting families and businesses.

It separates protection from gambling

The rule started as a legal safeguard in 1774 to stop people from buying insurance on lives when they had no legitimate financial stake, which helped prevent wagering and moral hazard, according to Allianz on the origins and purpose of insurable interest.

That history still matters. Life insurance should respond to loss, not create a reason to hope for one.

A driver's license is a useful analogy. It is viewed not as a punishment, but as a basic qualification that helps keep the road safer for everyone. Insurable interest does something similar. It confirms that the person buying coverage has a legitimate reason to be involved.

It protects the people insurance is meant to serve

This rule protects more than insurance companies.

It helps protect:

- Families who need coverage tied to real income replacement needs

- Businesses that need key person or partner protection for actual financial exposure

- Insured individuals who shouldn't have strangers taking policies out on them

- The broader market that depends on trust and fair underwriting

One reason this lands in real life is how people use coverage. 44% of Americans cite income replacement as the primary purpose of their life insurance, based on the same Allianz source linked above. That aligns neatly with the spirit of insurable interest. The policy is there to replace something meaningful that would be lost.

It keeps the process grounded in common sense

You don't need to be a lawyer to understand the logic.

Ask these questions:

- Would this person’s death harm me financially or within a recognized close relationship?

- Am I trying to protect against loss, or profit from a loss I wouldn't actually suffer?

- Would this relationship make sense to an underwriter reviewing the application?

Insurance works best when the payout fills a hole. It shouldn't create an incentive where no real hole exists.

Once you see the rule that way, it feels less like bureaucracy and more like guardrails.

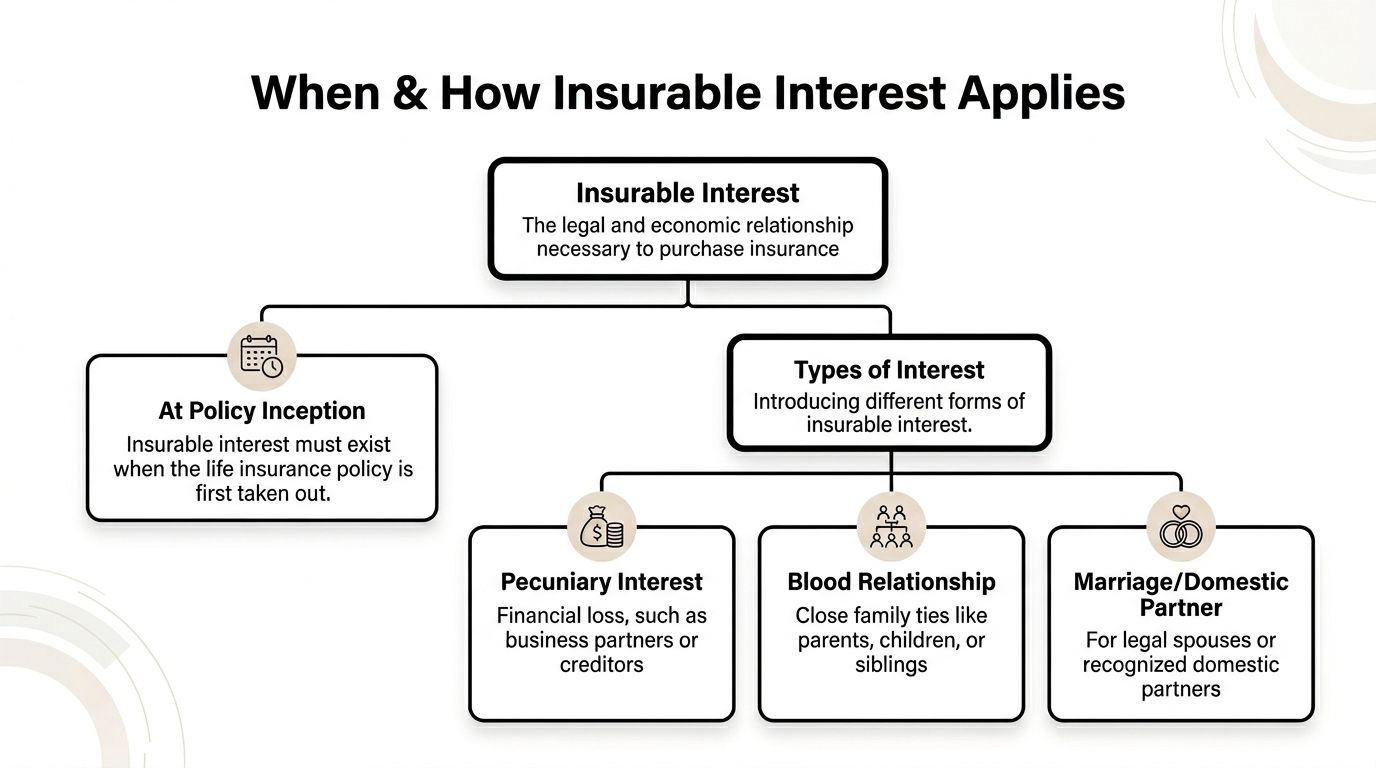

When and How Insurable Interest Applies

The timing matters just as much as the relationship. Many readers find this confusing.

It matters when the policy is issued

The key rule is this. Insurable interest is only required at the time the policy is purchased, not at the time of claim, as explained by Western & Southern on when insurable interest is required.

That point clears up a lot.

A spouse can have insurable interest when the policy starts. Later, the couple may divorce. If the policy stays in force and the beneficiary isn't changed, that later relationship change doesn't automatically erase the policy's validity. The issue is whether the insurable interest existed at the beginning.

The same source notes that this timing rule underpins 95%+ of policies that are owner-insured. In other words, individuals commonly buy life insurance on themselves, which avoids much of the complexity.

Practical rule: Ask whether the relationship was valid and meaningful when the policy was taken out. That’s the moment underwriters care about most.

Two broad ways people qualify

In plain language, insurable interest usually shows up in one of two forms.

Love and affection

Close family relationships often qualify because the law recognizes that these ties usually involve real dependency, obligation, or loss.

Common examples include:

- Spouses

- Parents and children

- Other close blood or legal relatives in many situations

This category isn't just about emotion. It's about the law recognizing that certain close relationships carry natural financial and personal consequences.

Economic interest

Some relationships qualify because money, contracts, or business continuity are on the line.

Examples often include:

- Business partners

- Employers insuring key employees

- Creditors with a valid loan exposure

In those cases, the interest needs to make sense in proportion to the likely loss. The policy should protect against a financial problem, not create a windfall.

Consent still matters

Even if the relationship fits, insurers usually want the insured person’s knowledge and cooperation during underwriting. That helps prove the arrangement is legitimate.

Think of the process as a one-time legitimacy check. Once the policy is properly issued, later life changes don't usually require the same proof again.

Real-World Examples Who Has Insurable Interest

The easiest way to understand this rule is to see it in ordinary life.

Life insurance isn't rare or fringe. 51% of adults hold coverage, 40% believe they don't have enough, and the market includes more than 267 million active policies, according to The Zebra's life insurance statistics research. That same source notes that insurable interest directly matters for 59% of parents with minor children who own life insurance and for businesses managing key person risk.

Spouses and domestic partners

A newly married couple buys a home together. One spouse earns most of the income. The other handles a big share of childcare and household management.

If either person dies, the survivor faces a real loss. It may be lost wages. It may be the cost of replacing caregiving. It may be both.

This is one of the clearest examples of insurable interest because the connection is obvious and ongoing. A legal spouse generally has a recognized stake in the other spouse’s continued life.

Common real-life reasons include:

- Shared housing costs

- Dependents who rely on both adults

- Joint debts

- Loss of future earning power in the household

Parents and children

A parent with young kids often buys life insurance because the family depends on that parent’s income or care.

A stay-at-home parent can also create a very real insurable interest. Even without a paycheck, that parent may provide childcare, transportation, scheduling, and household labor that would be expensive and disruptive to replace.

On the other side, parents can also have insurable interest in a child in certain legally recognized ways, especially around the costs and obligations connected to the relationship. The exact rules can vary by state and insurer, but the key point stays the same. There must be a legitimate stake, not simple curiosity or affection alone.

Business relationships

Two partners launch a firm together. One brings in clients. The other runs operations and signs contracts.

If either dies, the surviving partner may lose revenue, face debt pressure, or struggle to keep the business running. That can support insurable interest.

Key person and partner coverage often become relevant. A business may insure someone whose death would cause a meaningful financial setback.

If you want a practical look at related planning for owners, this guide to life insurance for small business owners is a useful companion read.

A few business situations often qualify:

- Co-founders with shared ownership

- A company insuring a key executive

- Owners funding a buy-sell arrangement

- A business covering a person tied closely to revenue or operations

Here’s a quick explainer that helps visualize how insurers talk about the concept in consumer terms:

Creditors and lenders

A lender doesn't usually have a broad right to profit from a borrower’s death. But a creditor can have insurable interest tied to a real debt.

Think of a person who lends a substantial amount to a business owner. If that borrower dies before repayment, the lender may suffer a measurable financial loss. That can support a limited insurable interest tied to the debt itself.

The key idea is proportionality. The coverage should connect to the actual exposure.

A creditor’s interest is tied to repayment risk, not to the borrower’s life in a general sense.

Who usually does not qualify

The rule becomes clearer when you flip it around.

These examples usually raise problems:

- A stranger with no financial tie

- A distant acquaintance

- A celebrity you don't know

- A coworker whose death wouldn't affect your finances

If the relationship doesn't point to real loss, the application will likely face trouble. That’s the system doing its job.

How to Document Insurable Interest

Once people understand the concept, the next question is practical. How do you prove it?

For close family relationships, the answer is often simple. The relationship itself may be enough for the insurer to see why the interest exists. In more complex arrangements, especially business or debt-related ones, paperwork matters more.

When interest is usually obvious

For a spouse or a parent applying in a straightforward family setting, insurers often don't need an elaborate paper trail beyond the normal application details and consent process.

That doesn't mean they skip review. It means the relationship usually speaks for itself.

When paperwork matters more

Business and creditor cases usually need stronger support. The insurer may want records that show the financial connection is real and that the coverage amount makes sense.

Use this checklist mindset:

- Identify the relationship clearly

- Show the possible loss

- Match the policy purpose to that loss

- Keep supporting documents ready

| Relationship to the Insured | Basis of Interest | Common Documentation |

|---|---|---|

| Spouse | Legal and financial connection | Marriage details on the application, identity information, insured’s consent |

| Parent of a minor child | Family relationship and recognized responsibility | Application details, identity information, insured information when applicable |

| Adult child insuring a parent | Family tie plus possible financial dependency or obligation | Application details, consent, and any insurer-requested explanation of dependency |

| Business partner | Shared financial stake in the business | Buy-sell agreement, ownership records, financial statements, insured’s consent |

| Employer insuring a key employee | Potential business loss if the employee dies | Employment records, business financials, internal authorization, consent |

| Creditor | Risk of unpaid debt | Loan agreement, repayment records, consent, proof of outstanding obligation |

One related tool in business and lending scenarios is collateral assignment of life insurance, which can help show how policy rights may be connected to a loan without changing the basic purpose of coverage.

Bring documents that prove the relationship first, and the dollar impact second. Underwriters usually need both in non-family cases.

A good application tells a clear story. Who is being insured, why this owner has a stake, and what loss the policy is meant to protect against.

Legal Implications and Common Mistakes

This rule has real consequences. If insurable interest was missing when the policy was issued, the policy can be in serious trouble.

What can go wrong

State laws codify the requirement. For example, Arizona Revised Statutes §20-1104 on insurable interest lays out recognized categories, and if insurable interest is absent when the policy is issued, courts can declare the contract void to prevent moral hazard.

That means the problem isn't just an underwriting delay. It can affect whether the contract is valid at all.

For businesses, that same legal framework matters when setting the amount of coverage. A key-person policy should align with a proven pecuniary loss, often benchmarked at 3 to 5 times the employee's annual salary, as reflected in the Arizona-based summary above.

Mistakes people make

Most errors aren't complicated. They usually come from misunderstanding what life insurance is for.

Common examples include:

- Trying to insure someone famous or unrelated because you think their death would create a payout opportunity

- Assuming affection alone is enough in a relationship that doesn't carry recognized legal or financial weight

- Using an inflated coverage amount that doesn't match the actual business or debt exposure

- Forgetting to review policy details so ownership, beneficiary, and purpose are unclear

If you're reviewing a contract and want to understand where these details show up, this guide on how to read a life insurance policy can help.

A valid policy starts with a valid reason for coverage. If that reason is weak or artificial at the beginning, the policy may not hold up later.

The safest approach is simple. Make sure the relationship is real, the loss is understandable, and the application says so plainly.

Secure Your Future with Confidence

Insurable interest sounds like legal jargon, but the day-to-day meaning is reassuring. Life insurance should protect people from real loss. This rule helps make sure it does.

For most young families, newly married couples, and business professionals, the idea isn't hard to apply. If someone depends on your income, your work, your care, or your role in a business, the reason for coverage is usually easy to understand. The key is making sure the policy is built around that genuine need.

If you've been wondering what is insurable interest in life insurance, the answer comes down to one sentence. You need a real stake in the insured person’s continued life when the policy begins.

That isn't a bureaucratic trap. It's a safeguard.

It protects the integrity of life insurance. It protects families from confusion. It helps businesses insure the risks that matter. And it gives you a clearer way to judge whether a policy setup makes sense before you apply.

If you're ready to put that understanding into action, Coveredly offers a digital way to shop for term life insurance that fits modern family and business needs, including options for up to $3M of coverage with no exams for most applicants.