You're probably here because State Farm feels familiar. Maybe you already have auto or home coverage with them. Maybe you trust the name, but you also expect the ease of opening a bank account, investing, and applying for insurance from your phone in minutes. That tension is what makes a modern state farm life insurance review worth reading carefully.

Life insurance gets confusing fast because the product itself is simple, but the buying process often isn't. You're not just choosing a company. You're choosing a style of service, a pricing philosophy, and a policy structure that has to fit your life now and still make sense years from now.

Table of Contents

- Is State Farm the Right Choice in a Digital World?

- State Farm Life Insurance Policies Explained

- Decoding State Farm's Pricing and Underwriting

- The Agent Experience and Financial Strength

- Is State Farm a Good Fit for Your Life Stage?

- State Farm vs Modern Alternatives Like Coveredly

- Frequently Asked Questions About State Farm Life Insurance

Is State Farm the Right Choice in a Digital World?

State Farm is the insurance version of a legacy brand people already know. For many buyers, that matters. If you're raising kids, buying a house, or building a career, a familiar company can feel safer than a newer online-only option.

But familiarity isn't the same as fit. A lot of people start shopping for life insurance expecting the process to work like other online purchases. They want fast quotes, a clean application, and clear answers without scheduling a meeting. State Farm often takes a more traditional path, which can feel reassuring to one person and frustrating to another.

A young couple is a good example. One partner may love the idea of a local agent who can explain riders and talk through a long-term plan. The other may wonder why buying life insurance still feels like setting up a dentist appointment.

Practical rule: If you want guidance and ongoing human support, State Farm's model may feel comfortable. If you want speed and self-service, the process may feel dated.

That's the central question in this state farm life insurance review. Not whether State Farm is legitimate. It clearly is. The better question is whether its mix of strong brand trust, agent support, and often higher pricing lines up with how you want to buy coverage today.

For some households, the answer is yes. For others, the brand premium and slower experience may not be worth it.

State Farm Life Insurance Policies Explained

State Farm's lineup is fairly traditional. You get the three policy types many shoppers expect, but the experience of choosing among them matters more than the labels. For a digital-first buyer, the essential question is not just what State Farm sells. It is whether these policies match how you want to buy, manage, and adjust coverage over time.

A simple way to sort the options is by job:

| State Farm Policy Overview | Coverage Duration | Key Feature | Best For |

|---|---|---|---|

| Term Life | Temporary | Coverage for a chosen period | Families covering mortgage, income replacement, child-raising years |

| Whole Life | Permanent | Lifelong coverage with cash value | Buyers who want stability and a long-term asset component |

| Universal Life | Permanent | Flexible premiums and adjustable structure | Professionals or households with changing financial needs |

Term life for temporary needs

Term life works like a safety net for your highest-responsibility years. If your paycheck helps cover rent or a mortgage, daycare, student loans, or everyday family expenses, this is usually the first policy type to examine.

That matters for young families because the goal is often simple. Replace income if one parent dies too soon. Cover major debts. Give the surviving partner time to recover without making rushed financial decisions.

State Farm's term policies may appeal to buyers who want an agent to walk them through choices such as riders, conversion options, and coverage amounts. State Farm also advertises term coverage limits that can reach high amounts for people with larger protection needs, which can matter for physicians, executives, and business owners.

Several rider options can make term coverage more customized:

- Children's Term Rider: Adds coverage for children under one rider.

- Select Term Rider: Extends level premiums for a longer period in certain designs.

- Waiver of Premium for Disability: Keeps the policy in force if a qualifying disability prevents you from working.

- Flexible Care Benefit Rider: Allows access to part of the death benefit for long-term care needs, though availability varies by state.

That menu is useful if your household needs more than a basic death benefit. It can also make the shopping process slower than the fast, quote-and-buy model many online insurers offer.

If terms like medical exam, health class, and approval timeline feel fuzzy, this plain-English guide to how life insurance underwriting works can help before you compare policy types.

Whole life for permanent coverage

Whole life is built to last for your entire life as long as premiums are paid. It also builds cash value over time, which is one reason this policy can sound appealing at first glance.

Here is where buyers often get stuck. Whole life is not just insurance. It is insurance plus a savings-like component inside the policy. That combination can be useful for someone who wants predictable premiums, lifelong coverage, and a policy they plan to keep for decades.

It can be less appealing for a buyer who mainly wants the most death benefit for the lowest monthly cost.

According to Annuity Expert Advice's State Farm review, State Farm's permanent life policies are backed by strong financial ratings, but its whole life dividends have historically trailed peers by 10 to 15 percent because of conservative crediting rates of 4 to 5 percent versus 5.5 to 6.5 percent at some competitors. That can lead to slower cash value growth over long periods.

A practical way to read that: if you want permanent coverage first and cash value second, State Farm whole life may still fit. If you are comparing whole life policies partly on long-term policy performance, it deserves closer scrutiny.

State Farm also sells smaller whole life policies aimed at final expense needs. In MoneyGeek's 2026 State Farm review, examples for guaranteed issue whole life include about $29 per month for $10,000 of coverage for a 45-year-old female nonsmoker and about $41 per month for $15,000.

Universal life for flexibility

Universal life is permanent coverage with more moving parts. You usually get more flexibility around premiums and policy structure than with whole life, which can help if your income or financial goals change over time.

That sounds modern on paper. In practice, it requires attention.

A business owner with uneven income might like the flexibility. A high-earning professional who expects expenses to shift over the next decade might like it too. But someone who wants a policy they can buy, automate, and rarely revisit may find universal life less comfortable than it first appears.

This is one place where State Farm's agent-based model can help. Universal life often makes more sense when someone explains how premium choices affect the policy later. A digital-first shopper should still ask a simple question before buying: do I want flexibility badly enough to keep reviewing this policy over time? If the answer is no, term life or whole life may be easier to live with.

Decoding State Farm's Pricing and Underwriting

Price usually becomes real the moment you compare two quotes side by side. One policy comes with a familiar brand and a local agent. Another may offer the same coverage amount with a faster online application and a lower monthly bill. For a young family or busy professional, that trade-off matters more than the logo.

State Farm often fits the buyer who wants guidance and is comfortable paying more for it. If your main goal is keeping costs low and getting covered quickly, it may feel less appealing than a digital-first option.

What pricing looks like in real life

State Farm is not usually framed as the low-cost pick for term life. As noted earlier, outside reviews often place it above cheaper competitors for common term policy scenarios.

That does not mean the price is unreasonable. It means you should be clear about what you are paying for.

Part of the premium can reflect the experience around the policy, not just the policy itself. With State Farm, that may include one-on-one help from an agent, a familiar national brand, and a more traditional buying process. Some shoppers value that. Others would rather keep the difference in their monthly budget.

A simple way to judge it is to ask what role you want the insurer to play.

- If you want personal guidance: A higher premium may feel fair.

- If you are comfortable buying online: Extra cost may feel hard to justify.

- If cash flow is tight: Even a modest price gap can affect how much coverage you can afford.

That last point is easy to miss. Paying more for the company name can sometimes mean buying less protection than your family needs.

How underwriting usually works

Underwriting is the insurer's screening process. It works like a lender reviewing a mortgage application. The company looks at your risk, then decides whether to approve you and what rate class to offer.

For State Farm, that review may include:

- Health history: Diagnoses, prescriptions, past treatment, and current conditions

- Tobacco use: Smoking and other nicotine use often raise rates

- Family medical history: Some applications ask about major hereditary conditions

- Coverage amount: Larger policies usually get more scrutiny

- Age and overall risk profile: Older applicants or people with more health complexity may face more follow-up

If you want a plain-English overview before you apply, this guide to how life insurance underwriting works explains what insurers typically review.

The experience matters as much as the checklist. A healthy applicant with a straightforward coverage request may wonder why the process cannot move as quickly as some online insurers do. A buyer with a more complicated medical history may feel better having an agent help gather details and set expectations.

That is the core State Farm trade-off through a digital-first lens. The traditional process can feel supportive, or it can feel slow.

Riders also affect cost. Adding options such as child coverage or a waiver of premium can make a policy fit family life better, but each add-on raises the total you pay. The smartest approach is to separate the nice-to-have features from the protection your household would rely on if income disappeared tomorrow.

The Agent Experience and Financial Strength

State Farm's biggest differentiator isn't just product variety. It's the agent-centered experience. That can be a real advantage if you want a person to call, sit with, and revisit over time.

Why the local agent still matters

Many online buyers underestimate how emotional life insurance decisions can feel. If you're deciding how much coverage your spouse needs, whether to add a children's rider, or whether permanent insurance belongs in your plan at all, talking through those questions with one person can reduce a lot of uncertainty.

A good State Farm agent can help translate insurance language into life decisions. That matters for buyers who don't want to self-direct everything.

Still, the trade-off is obvious. An agent-driven process often moves more slowly than a digital-first one. You may need calls, follow-ups, and more back-and-forth than you'd get with an online platform built around speed.

For readers comparing insurer reliability more broadly, it can help to see how ratings are framed across the market, including in guides like this review of Globe Life insurance ratings.

Why financial strength matters more than branding

Brand recognition is nice. Financial strength is what backs the promise.

According to Insure.com's 2026 State Farm life insurance ranking, State Farm ranked No. 9 among providers with an overall 4.4 out of 5 rating, driven largely by policy offerings and an A++ (Superior) financial strength rating from AM Best. For long-term policyholders, that matters because life insurance is a promise that may need to be honored decades from now.

If you're newly married and buying your first policy, this is easy to overlook. You're not just buying a contract for this year. You're choosing a company you want standing behind your family years into the future.

A short overview can help put that in context:

A financially strong insurer can justify a slower buying experience for some people. It won't justify that trade-off for everyone.

That's the split with State Farm. The company's strength and service reputation support the case for trust. The buying experience still leans traditional, and that won't fit every modern shopper.

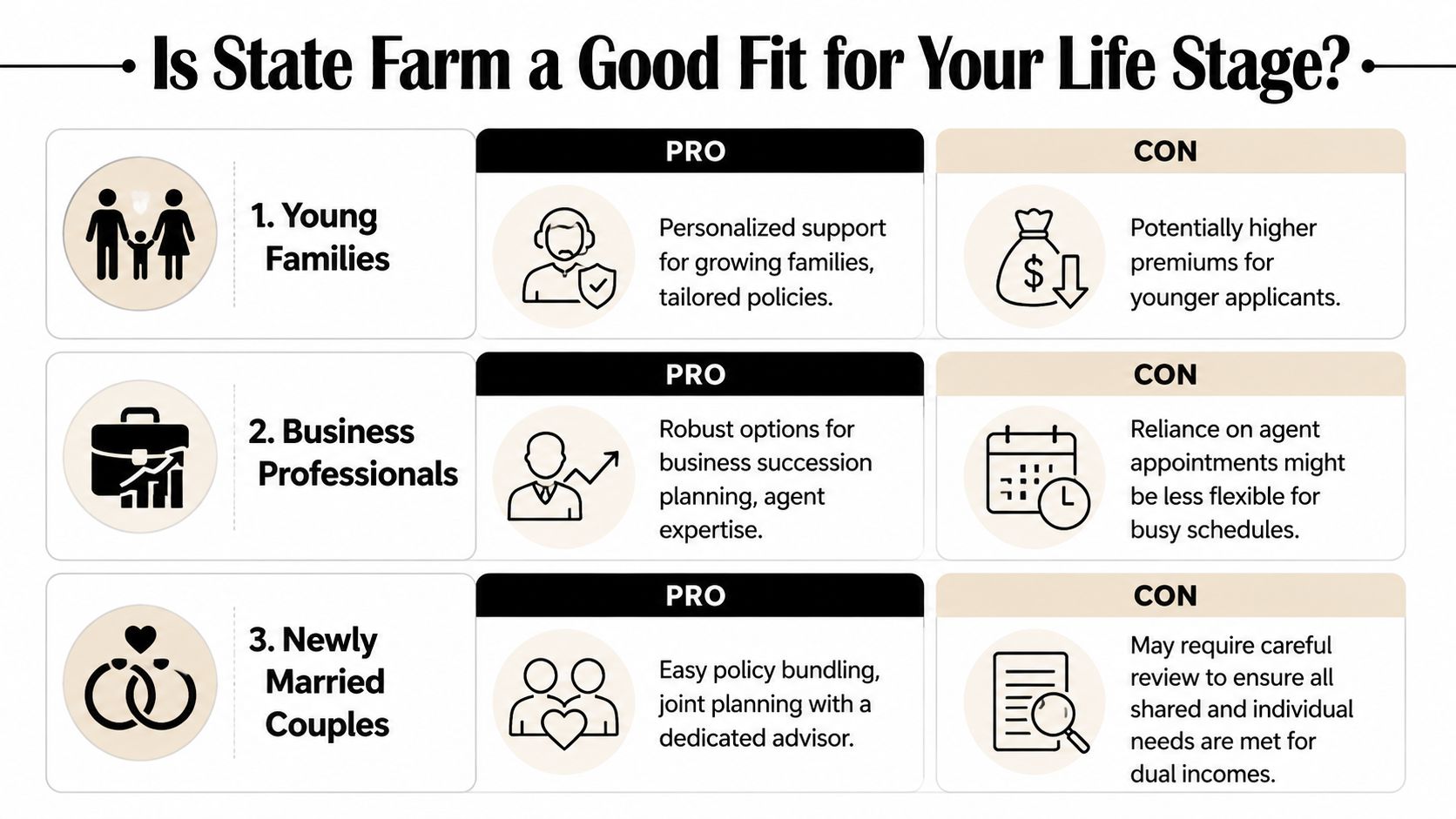

Is State Farm a Good Fit for Your Life Stage?

The best life insurance company for a retiree, a founder, and a couple expecting their first child probably won't be the same. State Farm makes more sense for some life stages than others.

Young families

If you have kids or are planning for them, State Farm has a lot going for it. The company's rider options can help parents build a policy around real household risks instead of just picking a death benefit and moving on. Having one agent who also understands your auto and home coverage may also make family planning feel simpler.

The downside is cost. If you're early in your earning years, a higher premium can crowd out other priorities like emergency savings, childcare, or retirement contributions.

State Farm often fits young families best when these points are true:

- You want human help: You'd rather ask questions than research every detail yourself.

- You like bundled relationships: One insurer across multiple products feels easier to manage.

- You care about customization: Riders and policy structure matter to your plan.

It may fit less well if your top goal is getting the most term coverage for the lowest price with the least hassle.

Business professionals

Professionals with higher incomes or more complex needs may appreciate State Farm more than younger budget shoppers do. If you're thinking about large coverage needs, debt protection, or business continuity planning, the traditional advisor model can be useful.

State Farm's appeal here is less about speed and more about structured planning. A buyer who wants to discuss permanent insurance, survivorship options, or layering riders may value that conversation.

Common reasons a business professional may like State Farm:

- You need a larger planning conversation: Insurance is part of a broader estate or business strategy.

- You prefer relationship-based service: You want a contact person rather than a support queue.

- You don't mind a slower process: Convenience is not your first priority.

The main drawback is flexibility of time. Busy professionals often want evening, mobile, and self-serve options. An appointment-based process can feel like one more thing to manage.

Newly married couples

Newlyweds often need straightforward coverage, not a highly engineered policy. They're trying to protect shared rent or mortgage payments, future children, and each other's income. In that phase, State Farm's stable reputation can feel reassuring.

There's also a planning benefit to sitting down together with one advisor. Some couples find that easier than trying to compare online quotes and policy structures on their own.

Marriage changes insurance needs fast. Beneficiary choices, debt sharing, and income dependence need to be reviewed together, not one policy at a time.

Still, many newly married buyers are digital natives. They expect simple applications, online account access, and quick decisions. If that's how you prefer to shop, State Farm's strengths may feel less compelling than they once did.

State Farm vs Modern Alternatives Like Coveredly

This is the cleanest way to frame the decision. State Farm represents traditional service. Modern digital insurers represent speed and simplicity.

Traditional service versus digital speed

State Farm works well for buyers who want conversation, context, and a local point of contact. If you already have an agent relationship and you like that model, staying in one ecosystem can feel efficient enough.

Digital-first alternatives appeal to a different kind of shopper. They're built for people who want to compare options online, move quickly, and avoid unnecessary friction. If that's your priority, products like no-exam term life insurance usually feel much closer to how people already buy other financial products.

The contrast usually comes down to a few real-world preferences:

- Choose State Farm if: You want in-person or agent-led guidance, you value legacy-brand comfort, and you don't mind a more traditional process.

- Choose a digital-first option if: You want speed, efficient applications, and a buying experience that feels native to your phone and laptop.

- Be especially careful if: You're paying extra mainly for familiarity, not because you want the added service.

That last point matters. Plenty of buyers assume they need a full-service insurance relationship when they really just need a solid term policy at a competitive price. Others assume speed is all that matters, then realize they wanted more guidance once policy choices became less obvious.

A good state farm life insurance review shouldn't pretend one model wins for everyone. It should help you choose the trade-off you'll be happy with after the application starts.

Frequently Asked Questions About State Farm Life Insurance

Does State Farm offer term and permanent life insurance?

Yes. State Farm offers term life, whole life, and universal life options. That makes it relevant for both simple income-replacement needs and more permanent planning goals.

Is State Farm good for online buyers?

It can be, but it's not built around a digital-first experience in the same way newer online insurers are. If you like working through an agent, that's a feature. If you want mostly self-service speed, it may feel slower than expected.

Can you convert a term policy later?

State Farm offers term options with features that may support longer-term planning, but conversion details depend on the specific policy and rider structure. This is one of those areas where reading the policy contract carefully matters more than relying on a broad summary.

Is a medical exam always required?

Not always in every insurance scenario, but buyers should expect more review as coverage amounts and complexity increase. The exact path depends on the policy, the amount requested, and your personal profile.

Who is State Farm best for?

State Farm is often strongest for people who value local guidance, want policy customization, and are comfortable paying more for service and brand trust. It's often weaker for shoppers who want the fastest and most digital buying process available.

If you want life insurance to feel simpler, faster, and more flexible, take a look at Coveredly. It's built for people who want modern coverage without the old-school friction, especially if you'd rather shop online than schedule your life around an insurance appointment.