You might be in that stage of life where your money is already assigned before payday hits. Rent or a mortgage. Student loans. A car payment. Maybe you're helping your parents with a bill, or your younger sibling leans on you more than anyone realizes. You may be single. You may be newly married. You may not have kids yet and still wonder whether life insurance is even relevant.

That's exactly why term life insurance for young adults deserves a closer look. It isn't only for parents with strollers and big suburban mortgages. It can also protect the people tied to your income, your debts, and the financial promises you've already made.

A lot of young adults put this off. Ownership is lower among younger people, with 42% of Gen Z ages 18 to 26 and 49% of Millennials ages 27 to 42 owning life insurance, compared with 52% of all Americans overall. That leaves a large protection gap, with over 100 million Americans uninsured or underinsured according to Choice Mutual's life insurance statistics research. The good news is that term coverage is often much more accessible than people assume.

Table of Contents

- What Is Term Life Insurance Exactly

- Why You Need Coverage Sooner Than You Think

- How to Choose Your Coverage and Term Length

- How to Get the Lowest Price on Your Policy

- The Simple Path to Getting Covered in 2026

- Common Mistakes and How to Avoid Them

- Answering Your Top Questions

What Is Term Life Insurance Exactly

Term life insurance operates similarly to renting financial protection. You choose a set period, pay for coverage during that window, and if you die during that term, the policy pays money to the people you named. If the term ends and you're still living, the coverage ends unless you renew or convert it.

That's different from permanent coverage, which is built to last longer and usually costs more. For many young adults, term life is the practical starting point because it focuses on protection, not on building cash value.

The simplest way to think about it

A term policy covers a specific stretch of time. Common term lengths are 10, 20, or 30 years, and the premium stays fixed for that entire period, with no cash value accumulation, according to Western & Southern's overview of life insurance for young adults.

For a healthy young adult, that can be surprisingly affordable. Term life insurance is typically under $20 per month, or about $240 annually, making it the most affordable option compared with permanent life insurance, according to MarketWatch's guide to life insurance for young adults.

If you want a plain-English overview of policy basics, this guide on what a term life insurance policy is is a useful companion.

Practical rule: Buy term life for the years when other people or other debts would feel your loss the most.

Four terms that matter

Insurance language gets easier once you strip it down to a few words:

- Premium means the amount you pay to keep the policy active, usually monthly.

- Death benefit means the lump sum your beneficiary receives if you die while the policy is in force.

- Beneficiary means the person or people you choose to receive that payout.

- Term means the coverage period you selected.

Here's the key distinction that confuses a lot of people. Term life is mostly about affordable protection. Permanent life can last much longer and may build cash value, but that added feature usually comes with a much higher cost. If your goal is to protect income, debts, or your household during your working years, term life insurance for young adults is often the cleanest fit.

Why You Need Coverage Sooner Than You Think

The old image of life insurance is a breadwinner with a spouse, two kids, and a mortgage. That situation still matters. But it's far from the full story.

Today, young adults often carry financial responsibilities that don't fit that old script. A co-signed private student loan can affect a parent. Support you give an aging parent can disappear overnight. A younger sibling may rely on your help with tuition, rent, or daily costs. Even if no one depends on your paycheck every month, someone may still be exposed to the fallout of your debts or final expenses.

It's not only about a spouse and kids

A big reason people delay buying coverage is simple. They think they're too early.

According to Midland National's Gen Z life insurance guide, 43% of Gen Z individuals delay purchasing life insurance because they believe they are "not at risk" yet, while 62% of young adults have co-signed debts, dependent siblings, or future income obligations that justify coverage as early as ages 22 to 25.

That matters because "need" is broader than parenthood. You may want coverage if any of these sound familiar:

- Co-signed debt: A parent helped you qualify for a loan and could be left carrying the balance.

- Family support: You regularly help with groceries, utilities, medication, or rent.

- Shared housing costs: A partner or roommate depends on your share of major bills.

- End-of-life costs: You don't want your family covering funeral and related expenses while grieving.

If your absence would leave someone with a bill, a debt, or a financial mess to untangle, life insurance belongs in the conversation.

A quick look at life insurance rates by age also helps explain why younger buyers often have an advantage when they shop early.

Why waiting feels harmless until it isn't

People don't delay because they've carefully analyzed the trade-offs. They delay because life insurance feels easy to postpone. It's invisible when everything is going fine.

But term life insurance for young adults works best when you buy it before health changes, before a debt gets larger, and before more people depend on you. Buying earlier gives you more control. Waiting gives underwriting more time to notice something you wish it couldn't.

How to Choose Your Coverage and Term Length

A lot of young adults get stuck here. They can picture the need in a general way, but turning that need into a dollar amount feels fuzzy.

A simpler way to handle it is to treat life insurance like a financial backup plan. Start with the bills and responsibilities that would not disappear if you did.

A simple way to estimate coverage

One common starting point is the Human Life Value approach. Guardian Life's explanation of how term life works says adults ages 18 to 40 are often pointed toward coverage equal to about 30 times annual income. That can be useful as a big-picture benchmark, especially for young workers whose earning years are still ahead of them.

For many people in their 20s and 30s, a build-it-yourself estimate feels more practical. Instead of starting with a formula, start with the actual obligations someone else might inherit.

A helpful checklist is the DIME method:

- Debt: Private student loans, co-signed loans, car loans, credit cards, personal loans

- Income replacement: Money a partner, parent, or other family member would need if your income stopped

- Mortgage or housing costs: Mortgage payments, rent support, or your share of shared bills

- Education: School costs for children, younger siblings, or other support you intended to provide

This approach works well for young adults because it goes beyond the old idea that life insurance is only for married parents. If your death would push a co-signer into debt, leave your parents short on monthly help, or force a partner to cover housing alone, those are real coverage needs.

Here is a practical example. A single 27-year-old with a co-signed private student loan and a parent who relies on a few hundred dollars of monthly help might choose enough coverage to clear the loan, cover final expenses, and replace that support for a few years. A married 32-year-old with a new mortgage may need a much larger amount because the goal is not just debt payoff. It is also keeping the household stable while the surviving partner regroups.

If you want a clearer framework, this guide on how much term life insurance to buy can help you test your estimate.

How to match the term to your life

Term length is easier once you stop treating it like a guess. Match the policy to the number of years you expect a major obligation to last.

A term policy works a lot like reserving coverage for a specific season of life. You are choosing how long you want that safety net in place.

Use your longest responsibility as the anchor:

- A shorter term can make sense if you mainly want to cover a loan balance, a co-signed debt, or a few years of support for a parent.

- A longer term may fit better if you recently bought a home or expect a partner to depend on your income for many years.

- If children are likely in the near future, you may want a term that carries protection through their dependent years, even if they are not part of your life yet.

The goal is not to predict every turn your life will take. The goal is to give the people connected to your finances enough time to recover, repay debts, or replace your income without making rushed decisions during a hard moment.

A quick way to pressure-test your choice

Before you apply, ask two plain questions:

- Would this amount fully cover the obligations I am most worried about?

- Would this term last through the years those obligations are likely to exist?

If the answer to either question is no, adjust before you buy. A policy should fit your real life, not a generic rule of thumb.

How to Get the Lowest Price on Your Policy

A lot of young adults assume life insurance pricing is mysterious. It is usually much more predictable than it looks.

Insurers price term life a bit like a lender prices a loan. They look at a few factors that signal risk, then use those details to set your rate. For young adults, the biggest price drivers are usually your age, your current health, whether you use nicotine, the coverage amount you choose, and how long the policy lasts. Some insurers also weigh driving history, certain medical issues, and higher-risk hobbies.

The practical takeaway is simple. The younger and healthier you are when you apply, the easier it usually is to lock in a lower rate.

What affects your premium

If you are 24 and deciding whether to apply now or wait a few years, this section is really about timing and fit. Buying earlier often costs less because insurers are evaluating the version of you that exists today, not the one you might be after a health change, a new diagnosis, or a few more birthdays.

Policy design matters too. A larger death benefit costs more than a smaller one, and a longer term usually costs more than a shorter term because the insurer is promising coverage for more years. That does not mean you should automatically choose the cheapest option. It means you want to be precise.

Precision saves money.

For example, a policy sized to cover a co-signed private student loan, a share of rent for a partner, or a few years of support for an aging parent may cost less than a policy built around a life you do not have yet. Young adults who are single and child-free sometimes overbuy because they assume life insurance is only about future spouses and kids. In reality, the right policy is the one that matches the financial obligations already tied to your name.

Ways to keep costs down

A lower premium usually comes from a handful of straightforward choices:

- Apply sooner if coverage already makes sense for you. Waiting rarely improves pricing.

- Answer every application question accurately. Accuracy helps prevent underwriting problems and claim issues later.

- Choose a coverage amount based on real obligations. Cover the debts, income gaps, or family support you want the policy to handle.

- Pick a term length that fits the timeline of those obligations. Extra years can raise the premium without adding much value.

- Compare quotes from more than one insurer. Companies assess risk a little differently, so the lowest price is not always in the first quote you see.

- Avoid adding features you do not need. Simple term coverage is often the most budget-friendly option.

Here is a helpful way to frame it over coffee. You are not shopping for the lowest sticker price. You are shopping for a monthly payment you can keep comfortably, tied to protection that would help the people connected to your finances.

That balance matters more than getting the absolute cheapest number on the screen.

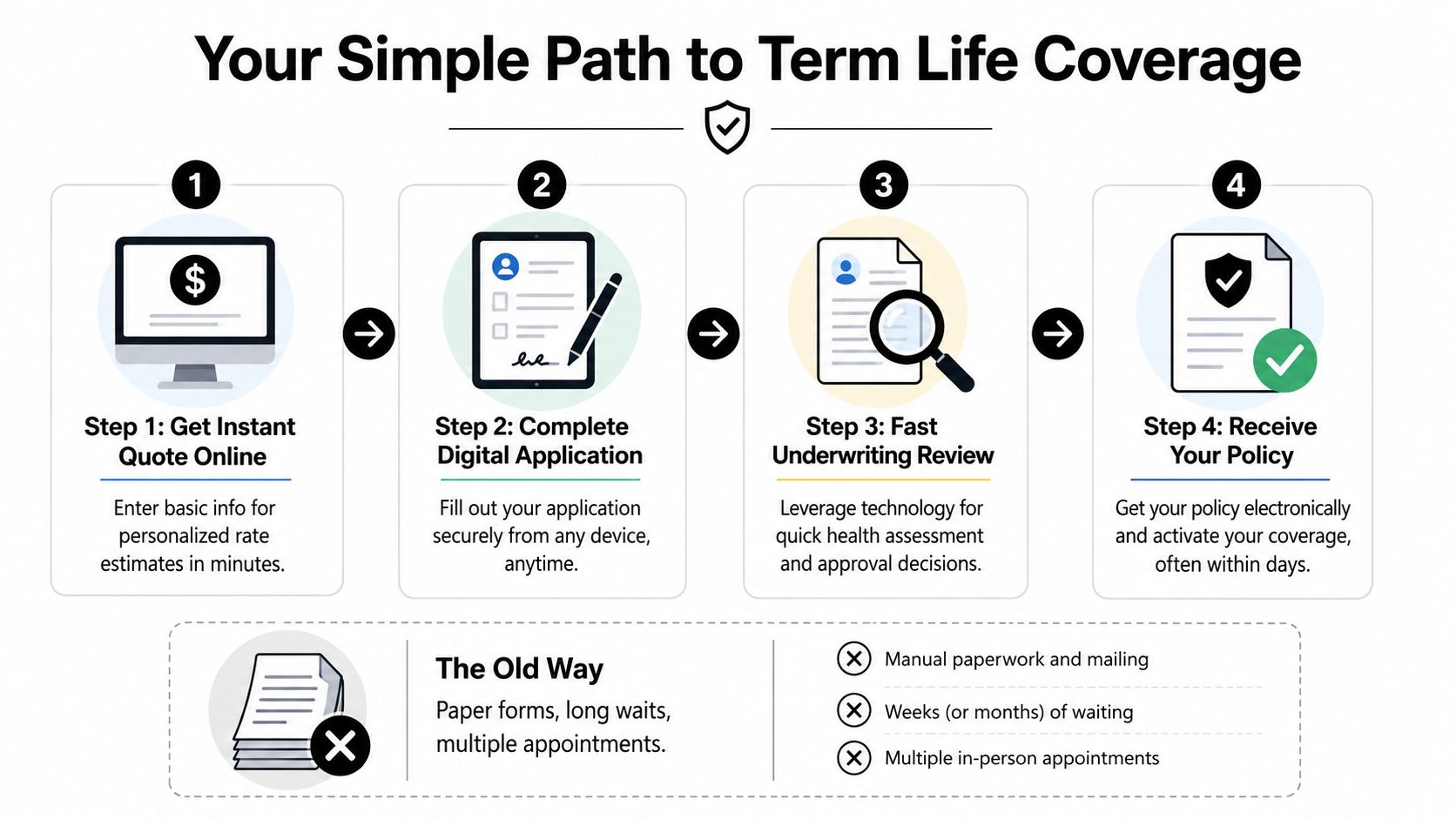

The Simple Path to Getting Covered in 2026

Buying life insurance used to sound like paperwork, phone calls, and a medical exam squeezed into your workweek. The process is often much more digital now.

That matters because friction is one of the biggest reasons people procrastinate. When the process feels easier, people finish it.

What the process looks like now

A modern application usually follows a simple flow:

- Get a quote online. You enter basic personal information and see estimated pricing.

- Complete the application. You answer questions about health, lifestyle, and the coverage you want.

- Go through underwriting. Some applicants can qualify through accelerated underwriting, which uses available records and application data to make a decision more quickly.

- Review and sign. If approved, you review the offer and e-sign the policy documents.

Here's a short walkthrough of the process in video form:

Some policies also offer no-exam paths, depending on the insurer and your profile. The point isn't that every applicant skips every step. It's that the process can be much less disruptive than many people expect.

What to have ready before you apply

You'll make the process smoother if you gather a few basics first:

- Your coverage goal: The amount and term you want.

- Beneficiary details: Full legal names and your relationship to them.

- Work and income information: Enough to explain the financial purpose of the policy.

- Health history: Medications, diagnoses, and recent doctor visits if applicable.

If you're organized going in, term life insurance for young adults can feel less like a major project and more like another smart financial task you check off this month.

Common Mistakes and How to Avoid Them

Most life insurance mistakes don't show up immediately. They show up later, when a family files a claim, when a term ends too soon, or when someone realizes the policy no longer fits their life.

That's why the setup matters almost as much as the decision to buy.

Mistakes that create problems later

A few errors come up again and again:

- Waiting too long: You may face higher pricing or fewer favorable options later.

- Buying too little: A small policy can leave debts and income gaps mostly untouched.

- Choosing a term that's too short: Coverage can expire while your biggest obligations are still active.

- Forgetting beneficiary updates: Marriage, divorce, and family changes can make an old beneficiary choice a serious problem.

One of the most overlooked mistakes involves conversion. According to TruStage's no-medical-exam life insurance resource, 58% of policyholders fail to convert their term policies because they're confused about eligibility windows and medical re-testing, even though newer no-exam conversion features are becoming more available.

A smarter way to set up your policy

A stronger setup usually looks like this:

- Match the term to your longest obligation

- Choose beneficiaries carefully

- Review the policy after major life events

- Check whether your policy includes a conversion option and when that window closes

Don't treat your policy like a document you buy once and never revisit. Treat it like part of your financial plan.

If your health changes later, understanding conversion options early can matter a lot. That's one detail worth checking while you're healthy, not after the fact.

Answering Your Top Questions

Can I own multiple life insurance policies

Yes. Some people layer coverage to match different needs. For example, one policy may cover a major debt while another covers income replacement for a partner or family member. What matters is that the total amount makes sense for your situation and budget.

What happens if I stop paying my premiums

For term life, missed premiums can lead to a lapse in coverage. If the policy lapses, the protection can end. That's why affordability matters so much when you choose your amount and term. A policy only helps if you can keep it active.

Does life insurance through work give me enough coverage

Sometimes it helps, but it may not be enough on its own. Workplace coverage can be limited, and it may not follow you if you change jobs. Many young adults use employer coverage as a base and buy their own policy for more control and portability.

If I'm single and don't have children, do I still need it

You might. If you have co-signed debt, support family members, share major expenses with someone, or want to avoid leaving final costs behind, term life insurance for young adults can still make sense.

If you're ready to see what coverage could look like in real life, Coveredly makes it easy to explore online life insurance built for modern schedules and modern budgets. You can review options, compare term coverage that fits your goals, and move at your own pace without turning the process into a second job.